Posts tagged ‘Apple’

Investors Slowly Waking to Technology Tailwinds

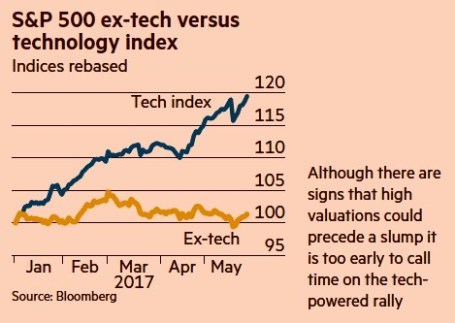

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Fink & Capitalism: Need 4 Kitchens in Your House?

Do you need four kitchens in your house? Apparently financial industry titan Larry Fink does. If Mr. Fink were a designer for millionaire homeowners, he would advise them to use their millions to build more kitchens in their house (reinvest) rather than distribute those monies to family members (dividends) or use that money to pay back an equity loan from mom and dad for the down payment (share buybacks). Essentially that is exactly what is happening in the stock market. Companies that are generating record profits and margins (millionaires) are increasingly choosing to pay out larger percentages of profits to stockholders (family members) in the form of rising dividends and share buybacks. Contrary to Mr. Fink’s belief, corporate America is actually doing plenty with room additions, landscaping, and roof replacements – I will describe more later.

As a consequence of corporate America’s increasingly shareholder friendly practices of returning cash, Fink believes this trend will stifle innovation and long-term growth in American companies. Here’s a snapshot of the supposed dividend/buyback problem Mr. Fink describes:

Source: Financial Times

Fink Mails Letter from Soapbox

For those of you who do not know who Larry Fink is, he is the successful Chairman and CEO of BlackRock Inc. (BLK), an investment manager which oversees about $4.65 trillion in investment assets. Mr. Fink ignited this recent financial controversy when he jumped on his soapbox by mailing letters to 500 CEOs lecturing them on the importance of long-term investing. What is Mr. Fink’s beef? Fink’s issues revolve around his belief that CEOs and corporations are too short-term oriented.

In his letter, Mr. Fink had this to say:

“This pressure [to meet short-term financial goals] originates from a number of sources—the proliferation of activist shareholders seeking immediate returns, the ever-increasing velocity of capital, a media landscape defined by the 24/7 news cycle and a shrinking attention span, and public policy that fails to encourage truly long-term investment.”

He goes on to bolster his argument with the following:

“More and more corporate leaders have responded with actions that can deliver immediate returns to shareholders, such as buybacks or dividend increases, while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.”

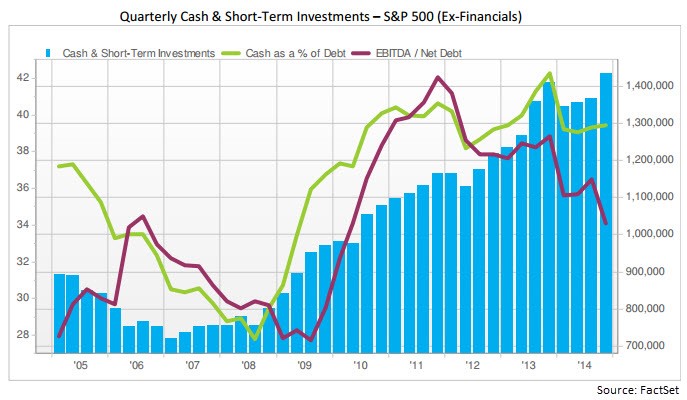

What Mr. Fink does not say in his letter is that large, multinational S&P 500 corporations driving this six-year bull run are sitting on a record hoard of cash, exceeding $1.4 trillion (see chart below). In this light, it should come as no surprise that CEOs are forking over more cash to investors in the forms of dividends and share repurchases.

What’s more, despite Fink’s assertion that share buybacks and dividends are killing innovation, he also fails to mention in his letter that 2014 capital expenditures of $730 billion are also at a record level. That’s right, CAPEX has not been cut to the bone as he implies, but rather risen to all-time highs.

It’s true that generationally low (and declining) interest rates have accelerated the pace of dividends/repurchases, however dividend payout ratios (the percentage of profits distributed to shareholders) of about 32% remain firmly below the long-term payout ratio of approximately 54% (see chart below) – see also Dividend Floodgates Widen. I find it difficult to fault many companies doing something with the gargantuan piles of inflation-losing cash anchoring their balance sheets. Don’t cash-rich companies have a fiduciary duty to borrow reasonable amounts of near-0% debt today (see Bunny Rabbit Market) in exchange for share buybacks currently providing returns of about 5.5% (inverse of 18x P/E ratio) and likely yielding 7%+ returns five years from now?

Source: Financial Times

The “Short-Term” Poster Child – Apple

There is no arguing that excessive debt eventually can catch up to a company. Our multi-year expanding economy is eventually due for another recession in the coming years, and there will be hell to pay for irresponsible, overleveraged companies. With that said, let’s take a look at the poster child of “short-termism” according to Mr. Fink …Apple Inc. (AAPL).

Of the roughly $500 billion in buybacks spent by S&P 500 companies in 2014, Apple accounted for approximately $45 billion of that figure. On top of that, CEO Tim Cook and his board generously decided to return another $11 billion to shareholders in the form of dividends. Has this “short-term” return of capital stifled innovation from the company that has launched iPhone version 6, iPad, Apple Watch, Apple Pay, and is investing into exciting areas like Apple Television, Apple Car, and who knows what else?

To put these Apple numbers into perspective, consider that last year Apple spent over $6 billion on research and development (R&D); $10 billion on capital expenditures; and hired over 12,000 new full-time employees. This doesn’t exactly sound like the death of innovation to me. Even after doling out roughly -$28 billion in expenditures and -$56 billion in dividends/share repurchases, Apple was amazingly able to keep their net cash position flat at an eye-popping +$141 billion!

Mr. Fink abhors “activist shareholders seeking immediate returns” but rather than deriding them perhaps he should send the greedy, capitalist Carl Icahn a personal thank you letter. Since Icahn’s vocal plea for a large Apple share buyback, the shares have skyrocketed about +85%, catapulting BlackRock’s ownership value in Apple to over $19 billion.

With respect to these increasing outlays, Mr. Fink also notes:

“Returning excessive amounts of capital to investors—who will enjoy comparatively meager benefits from it in this environment—sends a discouraging message.”

This would be true if investors took the dividends and stuffed them under their mattress, but an important message Mr. Fink neglects to address as it relates to dividends and share buybacks is demographics. There are 76 million Baby Boomers born between 1946 – 1964 and a Boomer is turning age 65 every 8 seconds. With many bonds trading at near 0% yields (even negative yields) it is no wonder many income starving retirees are demanding many of these cash-rich corporations to share more of the growing spoils via rising dividends.

Capitalism Works

After looking at a few centuries of our country’s history, one of the main lessons we can learn is that capitalism works – especially over the long-run. With about 200 countries across the globe, there is a reason the U.S. is #1…we’re good at capitalism. As our economy has matured over the decades, it is true our priorities and challenges have changed. It is also true that other countries may be narrowing the gap with the U.S., due to certain advantages (e.g., demographics, lower entitlements, easier regulations, etc), but the U.S. will continue to evolve.

In many respects, capitalism is very much like Darwinism – corporations either adapt with the competition…or they die. I repeatedly hear from pessimists that the U.S. is in a secular state of decline, but if that’s the case, how come the U.S. continues to dominate and innovate in major industries like biotechnology, mobile technology, networking, internet, aviation, energy, media, and transportation? Quite simply, we are the best and most experienced practitioners of capitalism.

Certainly, capitalism will continue to cultivate cyclical periods of excess investment/leverage and insufficient regulation. But guess what? Investors, including the public, eventually lose their shirts and behaviors/regulations adjust. At least for a little while, until the next period of excess takes hold. If Apple, and other balance sheet healthy companies allocate capital irresponsibly, capital will flow towards more aggressive and innovative companies. BlackBerry Limited (BBRY) knows a little bit about the consequences of cutthroat competition and suboptimal capital allocation.

While I emphatically share Mr. Fink’s focus on long-term investing values (including his self-serving tax reform ideas), I vigorously disagree with his attacks on shareholder friendly actions and his characterization of rising dividends/buybacks as short-term in nature. In fact, increasing dividends and share buybacks can very much coexist as a long-term investment and capital allocation strategy.

The question of proper capital allocation should have more to do with the age of a company. It only makes sense that younger companies on average should reinvest more of their profits into growth and innovation. On the other hand, more mature S&P 500-like companies will be in a better position to distribute higher percentages of profits to shareholders – especially as cash levels continue to rise to record levels and leverage remains in check.

BlackRock’s Larry Fink may continue to urge CEOs to reinvest their growing cash hoards into superfluous corporate kitchens, but Sidoxia and other prudent capitalist investors will continue to exhort CEOs to opportunistically take advantage of near-free borrowing rates and responsibly share the accretive gains with shareholders. That’s a message Mr. Fink should include in a letter to CEOs – he can use BlackRock’s lofty, above-average dividend to cover the cost of postage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including AAPL and iShares ETFs, but at the time of publishing, SCM had no direct position in BLK, BBRY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

NVEC: A Cash Plump Activist Target…For Icahn?

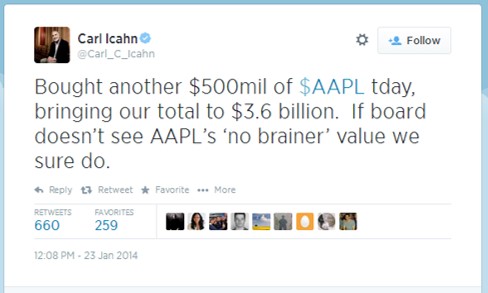

Some might call Carl Icahn a greedy capitalist, but at the core, the 78 year old activist has built his billions in fortunes by unlocking shareholder value in undervalued companies. His targets have come in many shapes and sizes, but one type of target is cash bloated companies without defined capital allocation strategies. A recent high profile example of a cash ballooned target of Icahn was none other than the $591+ billion behemoth Apple Inc. (AAPL).

His initial tweet on August 13, 2013 announced his “large position” in the “extremely undervalued shares” of Apple ($67 split adjusted). We have been long-term shareholders of Apple ourselves and actually beat Carl to the punch three years earlier when the shares were trading at $35 – see Jobs: The Gluttonous Cash Hog. Icahn doesn’t just nonchalantly make outrageous claims…he puts his money where his mouth is. After Icahn’s initial proclamation, he went onto build a substantial $3.6 billion Apple position by January 2014.

Icahn initially demanded Apple’s CEO Tim Cook to execute a $150 billion share repurchase program before downgrading his proposal to a $50 billion buyback. After receiving continued resistance, Icahn eventually relented in February 2014. But Icahn’s blood, sweat, and tears did not go to waste. His total return in Apple from his initial announcement approximates +50%, in less than one year. And although Icahn wanted more action taken by the company’s management team, Apple has repurchased about $50 billion in stock and paid out $14 billion in dividends to investors over the last five quarters. Despite the significant amount of capital returned to shareholders over the last year, Apple still holds a gargantuan net cash position of $133.5 billion, up approximately $3 billion from the 2013 fiscal third quarter.

Icahn’s Next Cash Plump Target?

Mr. Icahn is continually on the prowl for new targets, and if he played in the small cap stock arena, NVE Corp. (NVEC) certainly holds the characteristics of a cash bloated company without a defined capital allocation strategy. Although I rarely write about my hedge fund stock holdings, followers of my Investing Caffeine blog may recognize the name NVE Corp. More specifically, in 2010 I picked NVEC as my top stock pick of the year (see NVEC: Profiting from Electronic Eyes, Nerves & Brains). The good news is that NVEC outperformed the market by approximately +25% that year (+36% vs 11% for the S&P 500). Over the ensuing years, the performance has been more modest – the +42% return from early 2010 has underperformed the overall stock market.

Rather than rehash my whole prior investment thesis, I would point you to the original article for a summary of NVE’s fundamentals. Suffice it to say, however, that NVE’s prospects are just as positive (if not more so) today as they were five years ago.

Here are some NVE data points that Mr. Icahn may find interesting:

- 60% operating margins (achieved by < 1% of all non-financial companies FINVIZ)

- 0% debt

- 15% EPS growth over the last seven years ($1.00 to $2.29)

- Cutting edge, patent protected, market leading spintronic technology

- +7% Free Cash Flow yield ($13m FCF / $194 adjusted market value) $294m market cap minus $100m cash.

- $100 million in cash on the balance sheet, equal to 34% of the company’s market value ($294m). For comparison purposes to NVE, Apple’s $133 billion in cash currently equates to about 23% of its market cap.

Miserly Management

As I noted in my previous NVE article, my beef with the management team has not been their execution. Despite volatile product sales in recent years, it’s difficult to argue with NVE CEO Dan Baker’s steering of outstanding bottom-line success while at the helm. Over Baker’s tenure, NVE has spearheaded meteoric earnings growth from EPS of $.05 in 2009 to $2.29 in fiscal 2013. Nevertheless, management not only has a fiduciary duty to prudently manage the company’s operations, but it also has a duty to prudently manage the company’s capital allocation strategy, and that is where NVE is falling short. By holding $100 million in cash, NVE is being recklessly conservative.

Is there a reason management is being so stingy with their cash hoard? Even with cash tripling over the last five years ($32m to $100m) and operating margins surpassing an incomprehensibly high threshold (60%), NVE still has managed to open their wallets to pursue these costly actions:

- Double Capacity: NVE doubled their manufacturing capacity in fiscal 2013 with minimal investment ($2.8 million);

- Defend Patents: NVE fought and settled an expensive patent dispute against Motorola spinoff (Everspin) as it related to the company’s promising MRAM technology;

- R&D Expansion: The company shored up its research and development efforts, as evidenced by the +39% increase in fiscal 2014 R&D expenditures, to $3.6 million.

The massive surge in cash after these significant expenditures highlights the indefensible logic behind holding such a large cash mound. How can we put NVE’s pile of cash into perspective? Well for starters, $100 million is enough cash to pay for 110 years of CAPEX (capital expenditures), if you simply took the company’s five year spending average. Currently, the company is adding to the money mountain at a clip of $13,000,000 annually, so the amount of cash will only become more ridiculous over time, if the management team continues to sit on their hands.

To their credit, NVE dipped half of a pinky toe in the capital allocation pool in 2009 with a share repurchase program announcement. Since the share repurchase was approved, the cash on the balance sheet has more than tripled from the then $32 million level. To make matters worse, the authorization was for a meaningless amount of $2.5 million. Over a five year period since the initial announcement, the company has bought an irrelevant 0.5% of shares outstanding (or a mere 25,393 shares).

A Prudent Proposal

The math does not require a Ph.D. in rocket science. With interest rates near a generational low, management is destroying value as inflation eats away at the growing $100 million cash hoard. I believe any CFO, including NVE’s Curt Reynders, can be convinced that earning +7% on NVE shares (or +15% if earnings compound at historical rates for the next five years) is better than earning +2% in the bank. Or in other words, buying back stock by NVE would be massively accretive to EPS growth. Conceptually, if NVE used all $100 million of its cash to buy back stock at current prices, NVE’s current EPS of $2.59 would skyrocket to $3.63 (+40%).

A more reasonable proposal would be for NVE management to buy back 10% of NVE’s stock and simultaneously implement a 2% dividend. At current prices, these actions would still leave a healthy balance of about $75 million in cash on the balance sheet by the end of the fiscal year, which would arguably still leave cash at levels larger than necessary.

Despite the capital allocation miscues, NVE has incredibly bright prospects ahead, and the recently reported quarterly results showing +37% revenue growth and +57% EPS growth is proof positive. As a fellow long-term shareholder, I share management’s vision of a bright future, in which NVE continues to proliferate its unique and patented spintronic technology. With market leadership in nanotechnology sensors, couplers, and MRAM memory, NVE is uniquely positioned to take advantage of game changing growth in markets such as nanotechnology biosensors, electric drive vehicles (EDVs), consumer electronic compassing, and next generation MRAM technology. If NVE can continue to efficiently execute its business plan and couple this with a consistent capital allocation discipline, there’s no reason NVE shares can’t reach $100 per share over the next three to five years.

While NVE continues to execute on their growth vision, they can do themselves and their shareholders a huge favor by implementing a shareholder enhancing capital return plan. Carl Icahn is all smiles now after his successful investments in Apple and Herbalife (HLF), but impatient investors and other like-minded activists may be lurking and frowning, if NVE continues to irresponsibly ignore its swelling $100 million cash hoard.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in Apple Inc. (AAPL), NVE Corp. (NVEC), and certain exchange traded funds, but at the time of publishing SCM had no direct position in TWTR, MOT, Everspin, HLF, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

August Shakes, Rattles, and Swirls

Shake, Rattle, & Swirl: Category 3 hurricane Irene pounded the eastern seaboard with winds reaching 110 miles per hour, knocking out power in an estimated 8 million homes and businesses. Some analysts estimate the damage to be somewhere between $7 billion and $10 billion. If that wasn’t enough, earlier in the same week, a 5.8-magnitude earthquake rippled from its Virginia epicenter up to Maine rattling both buildings and people’s nerves.

Shake, Rattle, & Swirl: Category 3 hurricane Irene pounded the eastern seaboard with winds reaching 110 miles per hour, knocking out power in an estimated 8 million homes and businesses. Some analysts estimate the damage to be somewhere between $7 billion and $10 billion. If that wasn’t enough, earlier in the same week, a 5.8-magnitude earthquake rippled from its Virginia epicenter up to Maine rattling both buildings and people’s nerves.

Volatility Spikes in August: Volatility, as measured by the Volatility Index (VIX – a.k.a. “Fear Gauge”), reared its ugly head again in August, reaching a level exceeding 44 (Source: Hays Advisory). This reading has only been experienced nine times in the last 25 years. Historically, on average, these have been excellent buying points for long-term investors.

Volatility Spikes in August: Volatility, as measured by the Volatility Index (VIX – a.k.a. “Fear Gauge”), reared its ugly head again in August, reaching a level exceeding 44 (Source: Hays Advisory). This reading has only been experienced nine times in the last 25 years. Historically, on average, these have been excellent buying points for long-term investors.

![]() Steve Jobs Lets Go of Reins: After being Chief Executive Officer of Apple Inc. (AAPL – formerly Apple Computers) for more than 20 years, Steve Jobs passed the CEO reins over to Tim Cook, who has been with the company for 13 years (including interim CEO). Jobs will remain on board as Chairman of Apple and still provide assistance in a more limited capacity.

Steve Jobs Lets Go of Reins: After being Chief Executive Officer of Apple Inc. (AAPL – formerly Apple Computers) for more than 20 years, Steve Jobs passed the CEO reins over to Tim Cook, who has been with the company for 13 years (including interim CEO). Jobs will remain on board as Chairman of Apple and still provide assistance in a more limited capacity.

Buffett Puts Dry Powder to Work: Billionaire Warren Buffett is putting his money where his mouth is. Although he is one of a few wealthy individuals griping about too LOW income taxes (NYT OpEd), at least he is using some of his extra bucks to support the country’s financial system. More specifically, Buffet’s Berkshire Hathaway Inc. (BRKA) is investing $5 billion in troubled banking giant Bank of America Corp.’s (BAC) preferred stock (paying a 6% dividend), with warrants to buy additional stock in the future at a mutually prearranged price.

Buffett Puts Dry Powder to Work: Billionaire Warren Buffett is putting his money where his mouth is. Although he is one of a few wealthy individuals griping about too LOW income taxes (NYT OpEd), at least he is using some of his extra bucks to support the country’s financial system. More specifically, Buffet’s Berkshire Hathaway Inc. (BRKA) is investing $5 billion in troubled banking giant Bank of America Corp.’s (BAC) preferred stock (paying a 6% dividend), with warrants to buy additional stock in the future at a mutually prearranged price.

Google Buys Motorola Mobility: Google Inc. (GOOG) agreed to pay $12.5 billion to buy cellphone maker Motorola Mobility Holdings (MMI) in a move designed to protect the internet giant, and its partners, against patent litigation as it pertains to the Google Android mobile phone operating system. that could shake up the balance of power among among tech rivals. Time will tell whether Motorola’s assets will providing valuable resources for Google’s partners (i.e., HTC, LG Electronics and Samsung Electronics) or whether the acquisition will create competitive conflicts.

Google Buys Motorola Mobility: Google Inc. (GOOG) agreed to pay $12.5 billion to buy cellphone maker Motorola Mobility Holdings (MMI) in a move designed to protect the internet giant, and its partners, against patent litigation as it pertains to the Google Android mobile phone operating system. that could shake up the balance of power among among tech rivals. Time will tell whether Motorola’s assets will providing valuable resources for Google’s partners (i.e., HTC, LG Electronics and Samsung Electronics) or whether the acquisition will create competitive conflicts.

ECB Buys some Bonds:The European Central Bank (ECB), Europe’s equivalent of the U.S. Federal Reserve Bank, began buying up billions of dollars in Spanish and Italian bonds last month. The goal of the bond buying program is to stem any potential contagion effect arising from debt crises occurring in countries like Greece, Portugal, and Ireland.

ECB Buys some Bonds:The European Central Bank (ECB), Europe’s equivalent of the U.S. Federal Reserve Bank, began buying up billions of dollars in Spanish and Italian bonds last month. The goal of the bond buying program is to stem any potential contagion effect arising from debt crises occurring in countries like Greece, Portugal, and Ireland.

Quote of the Month

On Volatility:

“Worry gives a small thing a big shadow.”

– Swedish Proverb

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: For those taking this article seriously, please look up “parody” in the dictionary. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in BRKA, MMI, HTC,

LG Electronics and Samsung Electronics, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

The Internet: The Fourth Necessity

The basic necessities for human life are food, water, shelter and most importantly…the internet. Imagine a world where you cannot: access your email; text your spouse or significant other in the same house; Twitter the contents of your lunch; or Facebook a YouTube video of a dancing meringue dog (see video). Scary thought.

Many people take the internet for granted, just like the air we breathe, but how important a role does the internet play in people’s lives? Mary Meeker, internet analyst from Morgan Stanley, takes a look at this question in a recently released presentation she completed. Earlier in the decade, Meeker was raked over the coals during the deflation of the internet bubble, but in many respects she has been redeemed in the subsequent years as hundreds of millions of people continue to plug into the internet.

According to the broad base of expert strategists, we apparently are living in an overvalued, “New Normal ” market with subdued growth for as far as the eye can see (check out New Abnormal). In the mean time Meeker shows how the top 15 global internet franchises have nearly quadrupled revenue from $33 billion in 2004 to $126 billion today. Perhaps abnormally outsized opportunities in the corporate internet universe will be the “New Normal” over the coming years?

Internet Ubiquity

Source: Morgan Stanley

How ubiquitous is the internet becoming? Last year 1.8 billion people accessed this invisible global flattening medium we like to call the internet, and users spent 18.8 trillion minutes online, up +21% over the previous year. Many people are very familiar with the home-bred internet franchises of Facebook (620 million users), Google (940 million users), and Apple (120 million internet device users), but many investors under-appreciate the global scale of international internet franchises like Tencent (637 million users…more than Facebook by the way), Baidu ($40 billion market value), or Alibaba.com ($10 billion market value).

Source: Morgan Stanley

Mobile ubiquity is on the rise too. Connecting through a desktop or laptop is not enough these days, so internet addicts are increasingly attaching a mobile phone umbilical cord for such useful bathroom applications such as this (click here). Lugging a laptop around all over the place can be an inconvenience. So primal is the mobile instinct among internet users, Morgan Stanley expects mobile phone shipments to surpass PC and laptop shipments over the next 24 months.

What’s Next?

The party is just getting started. If you just consider eCommerce (purchases online), which only accounts for 4% of total commerce conducted in the U.S., then there is a lot of headroom for internet purchases to expand. The incredible potential rings true especially if you contemplate old traditional catalog, which peaked at more than 10% of overall commerce according to some industry executives. The rich feature functionality afforded to users through the internet, coupled with the increased convenience of mobility, augur well for future ecommerce sales growth.

The internet has been around for 15 years, but in the whole scheme of things this transformative medium is just a baby – especially if you consider the amount of time it took other revolutions like electricity, the rail network, and automobile proliferation to spread. That is why it is not too late to join the internet party. Food, water, and shelter are human necessities of life, just like exposure to the internet revolution is a necessity for your investment portfolio.

Read the Morgan Stanley Internet Presentation by Mary Meeker

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL and GOOG, but at the time of publishing SCM had no direct position in MS, BIDU, Tencent, Alibaba.com, Facebook, Twitter, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Corporate Shockers: You did *#$@% to Steve Jobs?

Source: 1funny.com

Steve Jobs recruited John Sculley to run Apple Computers (AAPL) in 1983 because the board wanted someone more experienced than a snot-nosed 28 year old founder barking orders at Apple employees. Sculley was a seasoned 15 year veteran executive from Pepsi Co. (PEP) whom was persuaded by Jobs to take over the company and join him in changing the world.

Things were all nifty until Sculley went all Brutus on Jobs and decided to fire him with board assistance in 1985 when it was believed that Jobs was poaching executives from Apple to join Jobs’s successor company, Next Computers.

The verdict may not completely be out on Sculley’s effectiveness on running Apple, but he deserves a PhD in the “Obvious Arts.” When asked if the coordinated decision (between Sculley and the Board) to fire Steve Jobs more than 25 years ago was correct, this is what Sculley had to say:

“In hindsight, I think they [board] made the wrong choice. They should have chosen Steve…we should have figured out a way to work with it [Job’s talent].”

Click Here for John Sculley Bloomberg Interview

Over his term at Apple, Sculley increased sales from $800 million to $8 billion. Good performance, but apparently not good enough, because Sculley was axed in 1993 and a window was opened for Jobs to return as Apple’s puppet-master four years later. The rest is history and AAPL stock went from about $10 per share when Sculley left all the way up to $316.65 today. Not too shabby.

In another shocker, after hiring Sculley and then getting fired by Sculley, Jobs said Sculley won’t talk to him. I can’t understand why a company founder would hold a grudge toward a hand-picked former employee who spearheaded a lynching against his boss? Well, I guess karma has a way of evening things out in the long run – redemption was found with Jobs’s climbing the Silicon Valley mountain to create the $300 billion consumer technology behemoth. I’m sure you don’t have to cry a river for John Sculley, but if he can’t control his own tears, he can always use his hundred dollar bills as tissue surrogates.

What makes Jobs’s decline and subsequent triumph even more unbelievable are the hugs and kisses Steve Jobs owes Microsoft founder and billionaire Bill Gates. If not for a $150 million lifeline offered by Gates to Steve Jobs in August 1997, while Apple was on its financial deathbed, we may not have ever experienced the iPod, iPhone, iPad, or future overhyped consumer gadget (OK, I admit it, I have succumbed to the hype myself). I’m guessing if Bill were given another chance, he would have passed on that Apple investment and we would be stuck paying for $4,000 computers and $1,000 Microsoft Office upgrades.

As a result of these corporate shockers, several lessons can be learned. Number one: If you are hired by a company founder, be careful about firing that boss if put in that position – you could potentially be jeopardizing the creation of hundreds of billions of dollars in future value. Number two: If you are unable to successfully negotiate lesson number one, then just find someone to lend you $150 million. History has taught us lessons based on past events ranging from Prohibition to Watergate, and from Nazi Germany to Tiger Woods’s indiscretions. John Sculley also learned lessons from Apple’s corporate shockers, and so can you.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in PEP, MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Jobs: The Gluttonous Cash Hog

Really? Do you think Steve Jobs actually needs to hoard $42 billion in cash reserves on the company’s balance sheet, when they are already adding to the gargantuan mountain of money at a $12 billion clip per year. Let’s not forget, this gaudy amount of money is being added after all operating expenses and capital expenditures have been paid for.

Perhaps Steve is just a little worried about the economy, and wants a little extra loose change around for a rainy day? I’d buy that argument, but Mr. Jobs and the rest of the executives just witnessed the worst financial crisis in a generation, and the company still managed to generate about $9 billion in free cash flow in both fiscal 2008 and 2009.

If Apple was not creating cash flow like those cascading chocolate fountains I see at wedding receptions, then perhaps a cash safety blanket is needed for acquisitions? Here’s what Steve had to say about Apple’s cash levels in February:

Steve Jobs (Source: Photobucket)

“We know if we need to acquire something – a piece of the puzzle to make something big and bold – we can write a check for it and not borrow a lot of money and put our whole company at risk…The cash in the bank gives us tremendous security and flexibility.”

Let’s explore that idea a little further. First of all, what type of experience does Apple have in doing large acquisitions? Not a lot, and just to humor myself I ran a screen on a universe of more than 10,000 stocks and I came up with 111 companies with a value (market capitalization) greater than $40 billion. Unless Apple plans on buying companies like Coca Cola (KO), Chevron Corp. (CVX), Pfizer (PFE), or United Parcel Service (UPS), I think Apple can part ways with some of their billions. Certainly, there are a handful of theoretical targets in the areas of technology and content, but for certain, (a) any large deal would face intense regulatory scrutiny, and (b) if truly there were grand synergies from doing a massive deal, then most definitely they would be able to issue stock (if Jobs hates debt) to help fund the deal. It is pure nonsense and laughable to believe any “big and bold” acquisition would put the company “at risk.” The only thing at risk for doing a large deal would be Apple’s stock price.

The truth of the matter is returning cash to shareholders would be a fantastic self-disciplining tool, like putting mayonnaise on a brownie to prevent excess calorie consumption. Steve should give current or former CEOs of AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, and Nextel a call to see how those large deals worked out for them. Apple could use an acquisition security blanket, but they do not need a circus tent of cash.

Times of Change

Although times have changed, some executives have not. Many tech companies, including Apple, have nostalgic memories of the go-go tech bubble days of the 1990s when growth at any price was the main mantra and no attention was paid to prudent capital allocation. With a stagnant stock market over the last twelve years, and interest rates sitting sluggishly at record lows (effectively 0% on the Federal Funds rate), investors are demanding prudent decision-making when it comes to capital allocation. Mr. Jobs, it is time to expand your narrow views and show the stewardship of sensibly managing the cash of your loyal investors.

Believe it or not, there are still a few of us actual “investors” that still exist. I’m talking about investors who do not just speculatively rent a stock for a day, week, or month, but rather those who invest for the long-term because they believe in the vision and execution capabilities of management and believe the company’s capital will be invested in their best interest.

I do not mean to single Mr. Jobs out, because he is not the only gluttonous, cash-hog offender among CEOs. In many respects, Apple has the good fortune of becoming a cash-hoarding poster child. The company does indeed deserve credit for becoming a $225 billion technology-consumer-media-retail juggernaut that has spread its tentacles brilliantly across numerous massive markets, whether its PCs, cell phones, music, television, movies, games, advertising etc.…you get the picture. But just because you are an exceptionally gifted visionary doesn’t give you the right to destroy value of hopelessly idle cash, which is begging for a better home than a 0.25% T-Bill.

Solutions – Taming the Cash Hog:

1) Divvy Up Dividends: With $42 billion in cash on the balance sheet and additional annual free cash generation on pace for $12 billion per year, there is no reason Steve Jobs and the board couldn’t declare a dividend that would yield 3% today. If that feels like too much, then how about shave off a pittance of $5 billion or so to pay out a sustainable dividend, which would yield a market-matching 2% dividend yield to investors. This scenario would accommodate Apple with at least a few decades of a cash cushion to cover ALL the company’s operating expenses and capital expenditures. This meagerly, ultra-conservative dividend policy can actually persist (or grow) longer than expected, if Apple can sustainably grow profits – a good possibility.

2) Share Buyback: This solution is much less desirable from my perspective compared to the dividend route, since many of the large share repurchasers tend to also issue lots of new shares to employees and executives, thereby neutering the benefits of the share repurchases.

3) Bank of Apple – (B of A): Why doesn’t Jobs just create a new entity, plop $40 billion of cash from Apple Inc. into the venture, and then open it up as Bank of Apple. At least that way, as an investor in the bank, I could make more profitable lending spreads at B of A relative to the 0.25% yield earned on the mega-billions deteriorating on Apple’s corporate balance sheet.

The downside of instituting these cash reducing solutions:

- The company doesn’t have as much cash as it would like to do large stupid acquisitions.

- The company loses a bunch of day-traders and short-term stock renters that don’t even know what a dividend is.

The upside to efficiently allocating capital through a 2% dividend is Steve (and the other investors) will receive a nice fat quarterly check. In the case of Jobs, he’ll collect a handsome $27 million or so to his measly $1 annual salary. In the process, the company will also gain long term shareholders that buy into the strategic vision of the company.

Stubbornness has served Steve Jobs tremendously well in his career, and a successful CEO like Steve Jobs is not required to listen to my advice. However, I am hopeful that Mr. Jobs will see the hazards of choking on a rapidly growing $42 billion cash hoard and discover the benefits of slimming down a gluttonous cash hog.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct positions in KO, CVX, PFE, UPS, AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, Nextel, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Digging for iPad Gold with Simplicity

We live in a hyper global competitive world, yet some companies manage to find gold while others unsuccessfully dig for their dreams. What is a major determinant of great companies? Apple Inc. (AAPL), and other companies, may include “simplicity” as a key ingredient. Take the iPad for example. Already the company has successfully exceeded iPad sales target thanks to the shrewd marketing of the simple touch-screen technology. Some call it a glorified iPhone because the iPad uses a very similar interface on a larger scale. Nonetheless, the device is getting rave reviews from the likes of US Today, The Wall Street Journal, The New York Times, Newsweek, and as Stephen Colbert smartly pointed out in his video (below), the iPad even makes salsa to boot. Many estimates point to more than a half million units sold in the first few weeks, making the 2010 estimates of 3-4 million units sold likely too low.

Competition Not a Game Killer

How much more competitive can the personal computer and cell phone markets be? According to the United Nations, we will reach 5 billion subscribers in 2010. With pricing pressure galore, and new Asian competitors popping up all over the place, how can companies grow, let alone make profits? Ever since the revolutionary iPhone was introduced in 2007, rivals have attempted to copy-cat the device. In the meantime, Apple continues to gain market share while they sit on close to $40 billion in cash, not to mention the flood of new cash rolling in the doors ($10+ billion in free cash flow generated in calendar 2009).

Innovation and the Remote Control

One key driver of profitability is innovation, but an elegant solution driven by an out-of-touch engineer with consumer demands will only lead to share losses and headaches. I mean how many times have you pulled your hair out trying to navigate through a 100-button TV remote control or screamed in frustration from attempting to learn a non-Wii videogame?

But Apple is not the only company to find simplicity in its quest for profit domination. In order to be a massive juggernaut like Apple Inc., a company’s product or service must gain mass appeal. A key determinant for mass appeal is simplicity. Beyond Apple, think of other dominant franchises that also operate in massively competitive markets like Wal-Mart Stores (WMT) in retail; Starbucks Corp. (SBUX) in coffee; Google Inc. (GOOG) in internet advertising; Coca Cola Co. (KO) in soda; Netflix Inc. (NFLX) in video rentals, among a host of other category killers. Many of these corporate giants offer products we cannot function or live without. I still find it utterly amazing that my children will never know what life was really like without an internet search on Google or a Caffe Misto Caramel Frappuccino from Starbucks.

All Good Things Come to an End

It’s not clear how much longer these titans of corporate America can thrive. By innovating new products that improve lives in some way, these Dancing Elephants will continue to prosper. But nothing in the stock market is static, so investors should pay attention to several potential derailing factors:

- Valuations: Valuations are extremely important in determining long-run appreciation potential, and chasing winners solely based on momentum (see related article) can lead to problems.

- Market Share Losses: What will be the next computer, cell phone, or e-reader killer? I don’t know right now, but eventually the day will come where these leaders will lose market share to a new kid on the block.

- Rising Costs: Competition is not the only factor in leading to slowing sales and declining profit margins. Inflation either related to labor or other input costs can crimp profits and decay investor appetites.

- Too Big to Succeed: There has been a lot of talk about “too big to fail,” but I strongly believe companies reach a point where they become “too big to succeed.” Either the law of large numbers catches up with these companies making simple math more challenging (think of the supertanker Wal-Mart growing its $400+ billion revenue base), or regulatory scrutiny kicks in (think of Microsoft Corp. [MSFT] and Intel Corp [INTC]).

Size: Peeling More of the Onion

Success can continue for these giants, however at some point “size” becomes a headwind rather than a tailwind. Just as simply as a train can speed down a railway at over 100+miles per hour, under the right conditions the train can derail as well. As Warren Buffett states, when referring to a company’s growth prospects relative to size, “Gravity always wins.”

However, investors should remind themselves that gains can last longer than expected too. Finding “ginormous” winners in many ways is like finding a needle in a haystack. But even if you find the needle in the haystack relatively late in a company’s growth cycle (see Equity Life Cycle story), in many instances there can be a lot of appreciation potential still available. Take Wal-Mart (WMT) for example. If you bought Wal-Mart shares after it rose 10-fold during its first 10 years, you still could have achieved a 60x return over the next 30 years.

Time will tell if Apple will strike additional gold with its iPad introduction, nonetheless Steve Jobs has found an element present in many long-term successful companies…simplicity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, WMT, GOOG, but at the time of publishing SCM had no direct positions in MSFT, SBUX, KO, INTC, NFLX, Nintendo or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}