Posts tagged ‘Apple Inc’

The Bunny Rabbit Market

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (April 1, 2015). Subscribe on the right side of the page for the complete text.

With spring now upon us, we can see the impact the Easter Bunny has had on financial markets…a lot of bouncing around. More specifically, stocks spent about 50% of the first quarter in negative territory, and 50% in positive territory. With interest rates gyrating around the 2% level for the benchmark 10-Year Treasury Note for most of 2015, the picture looked much the same. When all was said and done, after the first three months of the year, stocks as measured by the S&P 500 finished +0.4% and bonds closed up a similarly modest amount of +1.2%, as measured by the Total Bond Market ETF (BND).

Why all the volatility? The reasons are numerous, but guesswork of when the Federal Reserve will reverse course on its monetary policy and begin raising interest rates has been (and remains) a dark cloud over investment strategies for many short-term traders and speculators. In order to provide some historical perspective, the last time the Federal Reserve increased interest rates (Federal Funds rate) was almost nine years ago in June 2006. It’s important to remember, as this bull market enters its 7th consecutive year of its advance, there has been no shortage of useless, negative news headlines to keep investors guessing (see also a Series of Unfortunate Events). Over this period, ranging concerns have covered everything from “Flash Crashes” to “Arab Springs,” and “Ukraine” to “Ebola”.

Last month, the headline pessimism persisted. In the Middle East we witnessed a contentious re-election of Israeli Prime Minister Benjamin Netanyahu; Saudi Arabia led airstrikes against Iranian-backed, Shi’ite Muslim rebels (Houthis) in Yemen; controversial Iranian nuclear deal talks; and President Barack Obama directed airstrikes against ISIS fighters in the Iraqi city of Tikrit, while he simultaneously announced the slowing pace of troop withdrawals from Afghanistan.

Meanwhile in the global financial markets, investors and corporations continue to assess capital allocation decisions in light of generationally low interest rates, and a U.S. dollar that has appreciated in value by approximately +25% over the last year. In this low global growth and ultra-low interest rate environment (-0.12% on long-term Swiss bonds and 1.93% for U.S. bonds), what are corporations choosing to do with their trillions of dollars in cash? A picture is worth a thousand words, and in the case of companies in the S&P 500 club, share buybacks and dividends have been worth more than $900,000,000,000.00 over the last 12 months (see chart below).

Source: Financial Times

Case in point, Apple Inc (AAPL) has been the poster child for how companies are opportunistically boosting stock prices and profitability metrics (EPS – Earnings Per Share) by borrowing cheaply and returning cash to shareholders via stock buybacks and dividend payments. More specifically, even though Apple has been flooded with cash (about $178 billion currently in the bank), Apple decided to accept $1.35 billion in additional money from bond investors by issuing bonds in Switzerland. The cost to Apple was almost free – the majority of the money will be paid back at a mere rate of 0.28% until November 2024. What is Apple doing with all this extra cash? You guessed it…buying back $45 billion in stock and paying $11 billion in dividends, annually. No wonder the stock has sprung +62% over the last year. Apple may be a unique company, but corporate America is following their shareholder friendly buyback/dividend practices as evidenced by the chart below. By the way, don’t be surprised to hear about an increased dividend and share buyback plan from Apple this month.

Source: Investors Business Daily

Despite all the turmoil and negative headlines last month, the technology-heavy NASDAQ Composite index managed to temporarily cross the psychologically, all-important 5,000 threshold for the first time since the infamous tech-bubble burst in the year 2000, more than 15 years ago. The Dow Jones Industrial also cracked a numerically round threshold (18,000) last month, before settling down at 17,779 at month’s end.

While the S&P 500 and NASDAQ indexes have posted their impressive 9th consecutive quarter of gains, I don’t place a lot of faith in dubious, calendar-driven historical trends. With that said, as I eat jelly beans and hunt for Easter eggs this weekend, I will take some solace in knowing April has historically been the most positive month of the year as it relates to direction of stock prices (see chart below). Over the last 20 years, stocks have almost averaged a gain of +3% over this 30-day period. Perhaps investors are just in a better mood after paying their taxes?

Source: Bespoke

Even though April has historically been an outperforming month, banker and economist Robert Rubin stated it best, “Nothing is certain – except uncertainty.” We’ve had a bouncing “Bunny Market” so far in 2015, and chances are this pattern will persist. Rather than fret whether the Fed will raise interest rates 0.25% or agonize over a potential Greek exit (“Grexit”) from the EU, you would be better served by constructing an investment and savings plan to meet your long-term financial goals. That’s an eggstra-special idea that even the Easter Bunny would want to place in the basket.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including BND and AAPL (stock), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Here Comes the Great Rotation…Finally?

For decades interest rates have continually gravitated to zero like flies attracted to stink. For a split second in 2013, as long-term U.S. Treasury rates about doubled from 1.5% to 3.0% before reversing, it appeared the declining rate cycle could finally be broken. At the time, pundits of all types were calling for the “great rotation” out of bonds into stocks. Half of this forecast came to fruition as stocks grinded to record highs in 2014, but even I the big stock bull admittedly did not expect interest rates on 10-year Switzerland bonds to turn negative (see also Draghi QE Beer Goggles), especially after U.S. quantitative easing (QE) came to an end.

With rates already at a generational low, how could anyone be expected to accept a measly 0.3% annual return for a whole decade? Well, that’s exactly what’s happening in massive developed markets like Germany and Japan. While investors and retirees are painted into a corner by being forced to accept near-0% interest payments, savvy corporate borrowers are taking advantage of this once in a lifetime opportunity. Take for example the recently unprecedented $1.35 billion Switzerland bond issuance by Apple Inc. (AAPL), which included a tranche of bonds maturing in 2024 that yielded a paltry 0.25%.

With bonds offering lower and lower yield possibilities for investors of all stripes, at Sidoxia we are still finding plenty of opportunities in stocks, especially in high dividend-paying equity investments. In the U.S., the average S&P 500 stock is yielding approximately the same as the 10-Year Treasury Note (2.0%), but in other parts of the world, equity markets such as the following are offering significantly higher yields:

- iShares MSCI Australia (Yield 5.0% – EWA)

- Europe FTSE Europe (Yield: 4.6% – VGK)

- Market Vectors Russia (Yield 4.6% – RSX)

- iShares MSCI Brazil (Yield 4.0% – EWZ)

- iShares MSCI Sweden (Yield 3.8% – EWD)

- iShares MSCI Malaysia (Yield 3.8% – EWM)

- iShares MSCI Singapore (Yield 3.4% – EWS)

- iShares China (Yield 2.5% – FXI)

A New “Great Rotation” in 2015?

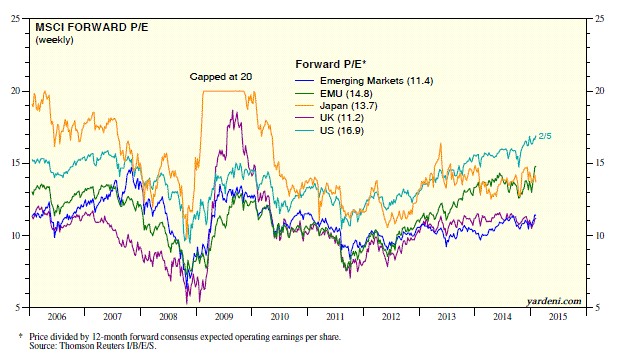

If you look at the 2014 ICI (Investment Company Institute) fund flow data, it becomes clear the great rotation out of bonds into U.S. stocks has not occurred. More specifically, despite the S&P 500 index reaching new record highs, -$60 billion flowed out of U.S. stock funds last year, and about +$44 billion flowed into all bond funds. Could the “great rotation” out of bonds into stocks finally happen in 2015? Certainly, this scenario is a possibility, but given the barren bond yield environment, perhaps the new “great rotation” in 2015 will be out of domestic equities into higher yielding international equity markets. In addition to the higher international market yields listed above, many of these foreign markets are priced more attractively (i.e., lower Price-Earnings (P/E) ratios) as you can see from the chart below created by strategist Dr. Ed Yardeni.

Source: Ed Yardeni – Dr. Ed’s Blog

Obviously, any asset shifting scenario is not mutually exclusive, and there could be a combination of investor reallocations made in 2015. It’s possible that previously unloved emerging markets and international developed markets could receive new investor capital from several areas.

With defensive sectors like utilities (up +25%) and healthcare (up +24%) leading the U.S. sector higher last year, it’s evident to me that “skepticism” remains the operative word in investors’ minds and there is no clear evidence of widespread euphoria hitting the U.S. stock market. Valuations as measured by trailing P/E ratios have objectively moved above historical averages, however this has occurred within the context of all-time record low interest rates and inflation. If you take into account the near-0% interest rate environment into your calculus, current stock prices (P/E ratios) are well within historical norms (see also The Rule of 20 Can Make You Plenty), which still leaves room for expansion.

If some of the half-glass full economic waters spill into the half-glass empty emerging markets/international markets, conceivably the eagerly anticipated “great rotation” out of bonds into U.S. stocks may also flow into even more attractively valued foreign equity opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL and certain exchange traded funds (ETFs) including VGK, EWZ, FXI, but at the time of publishing SCM had no direct position in EWA, RSX, EWD, EWM, EWS, and any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chewing on Some Apple Pie

Apple pie is an unrivaled American dessert that optimally mixes the elements of dough, sugar, cinnamon, and apples. With Thanksgiving just around the corner, I can already taste that Costco (COST) apple pie that is about to snap my belt buckle open as I proceed to eat pie for breakfast, lunch, and dinner. A different dessert of the stock variety, Apple Inc. (AAPL), recently received a sour reception after reporting its 3rd quarter financial results.

Despite reporting +27% year-over-year revenue growth and +23% earnings growth, investors have continued to spew the stock out as the share price has fallen from $700 per share down to $600 per share in about a month. With all this indigestion, is now the time to reach for the Tums or should we serve ourselves up another helping of some tasty Apple pie? Not everybody loves this particular fruity dessert, so let’s cut into the Apple pie stock and see if there is any dough to be made here.

Point #1 (Cash Giant): Apple Inc. is a profit machine with a fortress balance sheet. More specifically, Apple has around $121 billion dollars in cash in its checking account and generated over $42 billion in free cash flow in fiscal 2012. And by free cash flow, I mean the excess cash Apple gets to stuff in its pockets after ALL expenses have been paid AND after spending more than $8 billion in capital expenditures (including spending for their new 2.8 million sq. foot spaceship campus expected to open in 2015 and house 13,000 employees).

Point #2: (Brand): A brand has value that will not show up on a balance sheet, and according to Forbes, Apple’s brand is rated #1 on a global basis, outstripping iconic brands like IBM, McDonald’s (MCD) and Microsoft (MSFT). BrandZ, a division of advertising giant WPP, values Apple’s 2012 brand value at approximately $183 billion.

Point #3 (Product Pipeline): Apple is no one-trick pony. Apple’s iPhone sales account for about half of the company’s sales, but a whole new slate of products positions them well for the critical calendar fourth quarter period. Apple’s iPhone 5, iPad 3 (aka, “New iPad”), and iPad Mini should translate into robust holiday sales for Apple. What’s more, a +39% increase in Apple’s fiscal 2012 R&D (research and development) should mean a continued healthy pipeline of new products, including the ever-rumored new integrated version of Apple TV that could be coming in 2013.

Point #4 (Mobile & Tablets): Apple is at the center of the mobile revolution. There are approximately 5 billion cell phones globally, and about 2 billion new phones are sold each year. Of that 2 billion, Apple sold a paltry 125 million units (tongue firmly in cheek) with the market growing faster in Apple iPhone’s key smart phone market. As the approximately 500 million smart phone market grows to about 5 billion units over the next decade, Apple is uniquely positioned to capitalize on this trend. Beyond cell phones, the table market is bursting as traditional personal computer growth declines. Although Apple has made computers for 36 years, the company impressively generated +40% more revenue from fiscal 2012 iPad tablet sales, relative to Apple desktop and laptop sales.

Point #5 (Valuation): With all these positives, what type of premium would you pay for Apple’s stock? Does a +100% premium sound reasonable? OK, maybe a tad high, so how about a +50% premium? Alright, alright, I know you want a good bargain, so surely a +20% premium is warranted? Well in fact, if you account for Apple’s $121 billion cash hoard, Apple’s stock is currently trading at about a -22% DISCOUNT to the average S&P 500 stock on a P/E basis (Price-Earnings). You heard that correctly, a significant discount. If Apple is trading at a P/E discount, surely mature staple stocks like Procter & Gamble (PG) and Colgate Palmolive (CL), which both reported negative Q3 revenue declines coupled with meager bottom-line growth of 5%, deserve even steeper discounts…right? WRONG. These stocks trade at a 70-80% PREMIUM to Apple and a 35-40% PREMIUM to the overall market. Toilet paper and toothpaste I guess are a lot more popular than consumer electronics these days. Clear as mud to me.

Risks: I understand that Apple is not a risk-free Treasury security. Research in Motion’s (RIMM) rapid collapse over the last two years serves as a fresh reminder that in technology land, competition and obsolescence risks play a much larger role compared to other industries. Apple must still deliver on its product visions, and as the king of the hill Apple will have a big bulls-eye on its back from both competitors and regulators. Hence, we will continue to read overblown headlines about map application glitches and photographic purple haze.

In the end, a significant amount of pessimism is already built into Apple’s stock price (yes, I did say “pessimism” – even with the stock’s share price up +49% this year). If Apple can uphold the quality of its products and maintain modest growth, then I’m confident shareholders will happily eat another slice of Apple pie.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct positions in COST, IBM, MCD, CL, PG, MSFT, WPP, RIMM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Cramer Pulls Apple from Romney Tree

Republican Presidential primary candidate Mitt Romney has taken a lot of heat for his lack of conviction on various issues, whether they be on immigration, universal healthcare, or abortion. Jim Cramer, former hedge fund manager and host of TV show Mad Money, has also been known to do a bit of his own John Kerry-esque waffling. One of Cramer’s most recent high profile flip-flops is highflying Apple Inc. (AAPL). If Mitt Romney had his own stock show in his free time like Jim Cramer, there’s a high probability that Romney and Cramer could both agree that they were “for Apple, before they were against it, and now for it again.”

Some might think that picking on Jim Cramer is like clubbing a defenseless seal; wrestling a first grader; or stealing candy from a baby. Suffice it to say, I am not the first person to point out the dangers, inconsistencies, and irresponsible behavior associated with Jim Cramer’s recommendations. Here are some of the highest profile critiques of Jim Cramer in recent years past:

I. Daily Show Destruction

Vodpod videos no longer available.

Daily Show Skewering PART II Daily Show Skewering PART III

II. The Barron’s Bashing

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

III. New York Times Expose

Last year, this article highlighted the good, bad, and ugly, but the sentiment noted by famed Yale University endowment fund manager David Swensen echoes the sentiment of many investment professionals:

“Cramer induces his viewers to do things that are bad for them. He’s smart enough to know what he’s doing. ‘Mad Money’ delivers a very dangerous message — that individual investors can beat the market with momentum-driven, high-octane trading strategies. There are individuals who do beat the market, but their number is vanishingly small. Cramer is a master manipulator. He has absolutely no accountability. This is serious business; people’s retirements are at stake.”

Spoiled Apple Turns Sweet Again

Apple stock has historically been a favorite of Jim Cramer. Because why? Well, like many short-term traders, it’s a stock that has been going up! A few short months ago, however, Apple’s stock stopped going up, and was actually going down. Jim Cramer’s long love affair with Apple was on the rocks – this is what he had to say about Apple on November 9th (AAPL price – $395.28):

“Times Have Changed for Apple. I’m hearing about weak tablet sales, about iPhone 4S sales not up to snuff, along with worries about holiday sales for iPods.” In the past Jim would brush these worries aside, but in the past, the visionary Steve Jobs was still breathing. “These days though, every nuance, every little bit of worry about Apple, as we heard today from a brokerage firm talking about lighter tablet sales seaps into my ears, and I actually listen, and I agonize over it – I don’t want to…But I can’t dismiss these minute Apple data points as irrelevant any more. These days it would just be too glib…Apple is no longer a given. We are not going to re-recommend endlessly right here. We are waiting. I think actually better prices are coming. No reason to pull the trigger [buy]. No reason until then [lower prices].”

Oh my, what a difference 90 days makes! Has Steve Jobs been resurrected from the dead? Last I checked, the answer is no. Anxiety of whether new CEO Tim Cook was about to drive Apple off a cliff to obsolescence, like Research in Motion Ltd. (RIMM), has apparently been put on hold. Previous deep-rooted concerns about iPad and iPhone 4S sales from Jim Cramer’s in-depth analysis turned out to be completely off base. As a matter of fact, two months after Cramer went on his anti-Apple rant, the company reported blowout quarterly results of record proportions. Not only did earnings results explode +116% from a year ago (+37% higher than Wall Street forecasts), but iPad unit sales grew by +111% (15.4 million iPads) and iPhone unit sales grew +128% (37.0 million iPhones). To make matters worse, during Cramer’s temporary Apple break-up, he told his followers to buy Google Inc. (GOOG) instead of Apple. Oops…since that short time ago, Apple has only outperformed Google by a massive +28% or so.

Well, no reason to fret now because any worries about a dead Steve jobs, collapsing iPad/iPhone sales, and a RIMM-like train wreck have been quickly forgotten by Cramer over the last few months. Apple gloom has turned to champagne cheers. Here’s what Jim has to say now:

“This stock (Apple) has gripped the imagination like no other I’ve seen in my career. A stock going to $500 in a straight line.”

When Wall Street analysts recently weren’t bullish enough for Cramer (despite 50 “Buy” ratings, 3 “Hold” ratings, 2 “Sell” ratings), he had this to say:

“I want to grab them by the throat and say, ‘Will you give me a break?’ Apple sells at 10 times earnings; the average stock sells at 15 times earnings; Apple is a lot better than the average stock. Don’t you understand this stock is galloping to where it has to go, simply to catch up with the rest of the market? Don’t you see that happening? Don’t you understand that apple has to go higher?!

If these whipsaw stock recommendation reversals are not fast enough for you, no need to worry. Apparently flip-flopping on the overall market only takes 24 hours. Last week, Cramer could hardly control his excitement during his show’s opening, given another up-day in the market. To bolster his bullish case, Cramer proceeded to chastise Wall Street analysts for being so negative. With one rotation of the Earth, the following day, Cramer turned negative and nervous once again as the Dow Jones Industrials index fell 0.69%. Who knows what Cramer’s ever-changing mood will be next, but I can give you a hint – if you look at the daily direction of the Dow, your mood guessing batting average will be higher than Ty Cobb’s career average.

Selective Consumption at the Investment Supermarket

Despite all the criticisms, one should not shed a tear for this multi-mega-millionaire, Harvard grad, and Goldman Sachs Group Inc. alum (GS). Mad Money is highly entertaining for short-term traders, and in upward trending momentum markets, Cramer followers might do OK. Unfortunately, the lucrative, straight-upward market that Cramer made his fortunes in during the 1990s hasn’t been in existence over the last 12 years. For the untrained, investing masses who are looking to preserve and grow their retirement nest eggs, the schizophrenic recommendations that Jim Cramer provides can prove extremely damaging. We have seen this destructive dynamic especially at key inflection points in the market, whether it was at the 2000 peak of the market when his 10-stock “Winners of the New World” portfolio that collapsed by over -90%, or in late 2008/early 2009, near the market bottom, when Cramer told all investors to sell stocks unless you can wait five years.

Jim Cramer is not an evil person and he his very entertaining and sharp individual. I fully admit that I occasionally watch Mad Money for a chuckle and to also gain perspective of the speculative sentiment in the market. Although I would like to see better programming on the network, CNBC is not to be fully blamed. CNBC is like a supermarket that sells both healthy and unhealthy goods. While long-time Investing Caffeine readers know, I have been known to take numerous cavalier economists and strategists to task, many of my investing philosophies and strategies have been built off of long-time, successful investors that CNBC has interviewed or profiled. CNCB guests whom I have written about include, Warren Buffett, Ron Baron, Bill Gross, Ken Heebner, Wilbur Ross, Joel Greenblatt, Laszlo Birinyi, Jimmy Rogers, and others.

While Jim Cramer can be consumed in small doses by professionals and short-term traders, average investors should tread lightly. Investors will be better served by reading the labels of television commentators’ advice, and instead listen to those advisors or managers that have a time horizon consistent with your long-term financial goals.

Jim Cramer has been picked apart by many, but his screaming “Booyahs!,” singing “hallelujah” choirs, and flying bulls, make for compelling television. Although Jim Cramer and I are on the same page as Apple currently (I’ve owned for a long time), I have yet to come to a definitive decision on the 2012 presidential elections. If Cramer changes his view on Apple again in the coming days and weeks, I hope he invites his friend Mitt Romney on as a guest. That way I can kill two birds with one stone, and if one flip-flopper is entertaining to watch, having two should certainly be twice as amusing.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG but at the time of publishing SCM had no direct position in RIMM, GS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}