Posts tagged ‘AMZN’

Mission Accomplished?

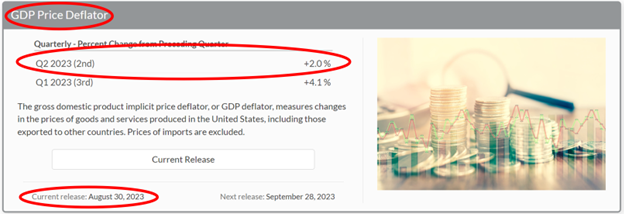

The Federal Reserve has a “dual mandate” designed to “foster economic conditions that achieve both stable prices and maximum sustainable employment.” The “dual mandate” is obviously a moving target, but it appears for now, based on the Fed’s explicit goals, Fed Chairman, Jerome Powell, has accomplished the central bank’s mission. More specifically, inflation, according to the just-reported BEA’s (Bureau of Economic Analysis) GDP Price Deflator statistics, has plummeted dramatically to the Fed’s goal of 2.0% from the sky-high inflation number of 9.1% a year ago (see chart below). Meanwhile, the economy continues to grow (+2.0% GDP growth in the 2nd quarter), and the long-awaited recession boogeyman has yet to appear.

Source: Bureau of Economic Analysis

Rate Pig Moving Through Economic Python

How has inflation plunged so quickly? For starters, in addition to the Fed’s restrictive policy of reducing the balance sheet, since the beginning of last year, the Fed has also effectively slammed the brakes on the economy by taking their target interest rate from 0% to 5.5%. The pace and scale of the interest rate increases have been reduced this year, however it is possible there might be more rate hikes ahead (currently, pundits are betting for no more rate increases this year, although a boost in November is possible if economic data accelerates). Like a pig working its way through the economic python, the large interest rate increases naturally take a while to work their way through the consumer, commercial, and government credit markets.

To put things in better perspective, a study done earlier this year showed the average 30-year monthly mortgage payment for a $500,000 home was higher by more than $800 (up +44%) versus a year ago! But wait, it’s not just consumers feeling the pinch of higher rates. Businesses and governments in all shapes and sizes have felt the pain as well from higher borrowing costs. Post-COVID supply chain constraints and disruptions have eased too, which have helped choke down the high inflation numbers. In the background, let’s not also forget about the disinflationary benefits of ever-expanding technology adoption coupled with the related productivity advantages (see also AI Revolution).

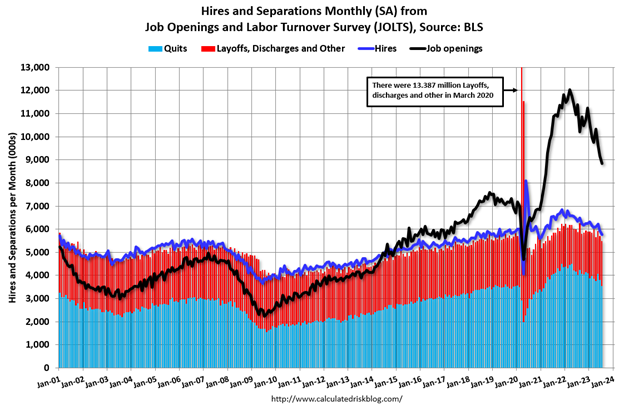

As a result of these dynamics, we are now starting to see cracks appear in our country’s employment foundation as this month’s JOLTs (Job Openings and Labor Turnover – see black line in chart below) and ADP monthly job additions data, which both came in disappointingly low compared to forecasts. Chairman Powell must be ecstatic inflation has plummeted, while the unemployment rate remains near multi-decade lows, and Gross Domestic Product (GDP) growth continues expanding (i.e., no recession in sight).

Source: Calculated Risk and U.S. Bureau of Labor Statistics

Hot Summer, Hot Stocks

Economic activity clearly can and will change, but the stock market has been like the weather this summer…hot. However, after experiencing up-months in six out of the first seven months of 2023, the S&P 500 index decided to take a small breather this month. For August, the S&P slipped -1.8%, but the month was a tale of two cities. By the middle of the month, the index had fallen by roughly -6% on fears of potentially more aggressive interest rate hikes by the Federal Reserve due to better than anticipated economic data. In other words, inflation fears were on the rise and the 10-Year Treasury Note yield temporarily climbed to a 52-week high. By the end of the month, economic data cooled, interest rates dropped a little, and stock prices rebounded smartly by +4.0% to finish the month on a strong note.

For the year, the S&P’s remain strongly positive, up +17.4%. As I have written in the past, the seven largest companies in the S&P 500 index (a.k.a., The Magnificent 7: Apple Inc.; Microsoft Corp.; Alphabet Inc.; Amazon.com, Inc.; NVIDIA Corp.; Tesla, Inc.; and Meta Platforms, Inc.) have contributed to a significant portion of the year’s gains – the average Magnificent 7 stock has skyrocketed an eye-popping +99.0% with NVIDIA being the largest winner, more than tripling in value during the first eight months of the year.

The Federal Reserve can admit they were late to the game in taming out-of-control inflation, but Fed Chair Powell has been swift in moving to preserve his legacy as an inflation fighter. Now that inflation is coming under control and the economy is beginning to cool, Powell needs to make sure he doesn’t murder the economy into recession with overzealous future interest rate increases. Time will tell if the mission has already been accomplished, but so far, the Fed has been delicately balancing an economic soft landing and stock market investors like it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, MSFT, GOOGL, AMZN, NVDA, TSLA, META, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dancing Elephants in a Challenging Economy

To many, the significant rebound in global equity markets, since the March 2009 price lows, has merely been a dead-cat bounce or simply a temporary “sugar high” from the extraordinary fiscal and monetary measures taken by governments all over the world. John Authers, columnist at the Financial Times, captures that cycnical view in his daily column. He believes we are on the cusp of financial dynamics that will “drive a bear market for another two decades.” Ouch – pretty harsh outlook.

Perception Can Differ from Reality

Throughout much of 2009, the better than anticipated corporate results were rationalized as improvements only coming from discretionary cost-cutting. Well, as of last week, 73% of the S&P 500 companies that reported quarterly results exceeded earnings expectations, with 70% surpassing revenue estimates as well. With the 9.7% unemployment improving (at least temporarily), the recovery cannot solely be attributed to cost-cuts.

In the midst of the economic recovery (+5.7% growth in Q4 GDP), other animals beyond deceased felines have joined the party, including dancing elephants. More than seven million jobs have been lost since the late-2007 recession began, yet a broad set of companies have thrived through this horrible environment. The bubble economy has certainly had a disproportionately negative impact on particular areas of the economy (e.g., housing, credit, and automobiles). However, in the midst of the global credit tsunami that engulfed us over the last two years, the largest global economic engine (U.S.A.) was still churning out about $14 trillion in the sales of goods and services. Many companies that were not reliant on the financial and credit markets used their superior competitive positioning to generate significant piles of cash. Instead of piling on additional debt (or diluting owners through share offerings), certain corporations tightened their belts, invested prudently, and stepped on the throats of other irresponsible and reckless competitors, which were forced to recoil back into their caves and bunkers.

Dancing Elephants

Times are tough, right? If that is indeed the case, let’s take a look at a few elephants that are trouncing the competition, even under extremely challenging economic circumstances:

Apple Inc. (AAPL) – Revenue growth +32% ($182 billion market capitalization): In the recent quarter, Apple pounded the competition by selling a boatload of electronic goods, including iPhones, iPods, and Mac computers. Next up, the iPad!

Amazon.com Inc. (AMZN) – Revenue growth +42% – ($53 billion market capitalization): In the fourth quarter ending December, Amazon pulverized peers in a cutthroat holiday by selling lots of Kindles (e-reader), growing +49% internationally, and adding a new Zappos.com shoe and accessory acquisition. Organic revenue growth (ex-Zappos) was still incredibly strong at about +23%.

Corning Inc. (GLW) – Revenue growth +41% – ($28 billion market capitalization): Results were buoyed by demand for its liquid crystal display (LCD) glass as consumers continued purchasing LCD televisions, laptop computers, and other electronic devices. In addition, GLW experienced a resurgence in demand for its emissions control products as the auto industry rebuilt supply. Telecom orders in China were solid also.

Google Inc. (GOOG) – Revenue growth +17% – ($169 billion market capitalization): In addition to the growth in the global search advertising market and YouTube video platform, Google also accelerated the deployment of their mobile platform, including their Android cell phone operating system, and concentrated on the expansion of the display advertising market.

Gilead Sciences Inc. (GILD) – Revenue growth +42% – ($42 billion market capitalization): Growth was catapulted by GILD’s dominant HIV/AIDS product franchise, including Atripla, Truvada, and Viread. Pulmonary arterial hypertension drug Letairis and chronic angina treatment Ranexa also contributed to stellar results.

Intuitive Surgical Inc. (ISRG) – Revenue growth +40% – ($13 billion market capitalization): This cutting-edge surgical equipment manufacturer enjoyed robust expansion from continued robotic procedure adoption and higher da Vinci Surgical System sales.

Intel Corp. (INTC) – Revenue growth +28% – ($113 billion market capitalization): The company’s semiconductor sales growth was fairly broad based across its major segments (Data Center, Intel architecture, Atom Microprocessor/Chipset) as demand recovered and depleted inventories were replenished globally.

Netflix Inc. (NFLX) – Revenue growth +24% – ($3.5 billion market capitalization): Netflix added more than one million new customers in the quarter as they continued to eat Blockbuster’s-BBI (and other competitors’) lunch. In addition, the company’s streaming “Watch Instantly” service continues to gain traction.

Although I do currently own a few of these companies, do NOT interpret this partial list of companies as “buy” recommendations – in fact, some of these stocks may be excellent “short” ideas. Regardless of how sexy growth may be, investors should never ignore valuation (read more about valuation). As stated at the beginning of the article, I mainly want to emphasize that trillions of commerce dollars are being transacted, even in demanding economic times. It just goes to show, one can turn lemons into lemonade. Or said differently, even elephants can be trained to dance.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, AMZN, and GOOG, but at time of publishing had no direct positions in GLW, GILD, ISRG, INTC, BBI, and NFLX. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Amazon: Growing Up to be Wal-Mart

Wal-Mart (WMT) got its start almost 50 years ago with its first store in Rogers, Arkansas (1962). Since then, the company has expanded to create a global franchise generating more than $400 billion in revenues with a market capitalization valued at about $190 billion. Amazon.com Inc. (AMZN) is a relative toddler (founded in 1995 by CEO Jeff Bezos) generating about $20 billion in revenue with a market cap about 1/5th that of Wal-Mart. Mr. Bezos graduated summa cum laude, Phi Beta Kappa in electrical engineering and computer science from Princeton University in 1986, and we know he has no problem in thinking big. The evidence can be found in his space travel company, Blue Origin, which is expected to initiate human travel in the upcoming years. Beyond space, Mr. Bezos is presented with a multitude of growth opportunities that have the potential of elevating Amazon from a young toddler into a mature adult like its cousin Wal-Mart.

So how does Mr. Bezos get the company through puberty to adulthood? Well actually, all I believe it will take is just more of the same. The company has created an incredible franchise with huge barriers to entry, if you consider the billions spent on the technology, infrastructure, and its distribution dominance as compared to its e-commerce brethren. Bolting on new categories (whether its jewelry, sporting goods, groceries, private label or digital downloads) can be extremely profitable since unlike Wal-Mart, Amazon doesn’t need to build or reconfigure thousands of stores to expand into new categories. For example, Wal-Mart has opened over 600 Sam’s stores nationally in order to target the wholesale club market. Once a new category is added, the blue-print is rolled out nationally and then eventually internationally. And just like Wal-Mart, as economies of scale are achieved, the cost savings are rolled back into lower prices, which then brings more customers, and even more scale advantages. This virtuous cycle then creates deeper and deeper moats separating itself from competitors.

GROWTH OPPORTUNITIES

Besides just the natural expansion of users purchasing more online and Amazon adding to existing categories, here are some other fertile areas for future growth:

- Amazon Prime (Free shipping membership is driving incremental revenue and usage).

- Kindle (This digital reader is already estimated to account for 35% of Amazon’s book sales and some analysts see $2 billion in Kindle revenues by 2012).

- Zappos.com (This acquisition provides instant dominance in shoes and adjacent product lines).

- International Expansion (Joyco.com acquisition in China is an example of how Amazon is expanding into emerging markets).

- New Categories (There are virtually limitless potential categories, but the migration to digital will be key).

- Cloud Computing, Storage & Other Services (EC2 cloud computing, S3 storage, and other outsourced technology services offer promising opportunities).

TREND IS AMAZON’S FRIEND

Source: U.S. Department of Commerce

E-Commerce sales account for only about 3.6% of total retail sales ($32.4 billion in Q2’09), but as you can see from the chart, the upward sloping trend is the friend of Amazon. With the proliferation of broadband and the natural aging of our next generation of computer-savvy internet users, not only is the number of online shoppers increasing, but the amount of time spent online is escalating as well. If you consider catalog sales (e.g. Land’s End, L.L. Bean, Eddie Bauer, etc.) have represented about 7-8% of total retail sales, there is a lot of head-room left for online sales to catch-up or replace these sales. Mr. Bezos believes online industry sales can ultimately reach 15% of total retail sales (double catalog sales). Top-rate online franchises like Amazon will be natural beneficiaries of these trends and funnel shoppers through their internet aisles, as a function of these demographic and behavioral tailwinds.

CAPITAL ADVANTAGE

Even when you account for the significantly higher revenue growth rates and growth initiatives (e.g., Kindle, E3, digital, etc) for Amazon relative to Wal-Mart, the capital intensity (as measured by CAPEX/Sales) is still about 70% higher for Wal-Mart as compared to Amazon. For one thing, Amazon does not need to support the some 8,100 stores in 15 countries that Wal-Mart is saddled with, and in turn Amazon can redeploy that capital into areas such as new products, services, and lower delivery costs. Surviving the dot-com bubble bursting, along with paying down billions of debt has afforded Amazon even more capital flexibility.

VALUATION

Valuation can be tricky, especially when you’re talking about a high growth company like Amazon. The exercise becomes a little easier once you realize Amazon is generating about $1.5 billion in free cash flow per year, with $4.3 billion in cash/investments on the balance sheet with virtually no debt in the middle of one of the worst recessions in a generation. At roughly $90 per share, AMZN is trading at over 53x’s Wall Street analysts’ projected earnings of $1.68 for 2009. Jeff Bezos and the rest of the management make it very clear the company is managing their business to one key goal – maximize free cash flow per share (music to my ears – see my article on cash flow). On that basis, AMZN trades at about 25x’s trailing free cash flow and closer to 22x’s if you strip out the $4 billion+ in cash on the balance sheet. If AMZN can grow 15% for the next 5 years (not a given), the valuations just mentioned above could be chopped in half, if price levels and share count remained constant.

With the large run-up in 2009, I have locked in some gains this year, but tactically I will be doing what “Deep Throat” advised in the movie All the President’s Men, and that is to follow the money (cash). If Bezos and Amazon can continue on its current growth trajectory in the coming years, this toddler will mature into a company more closely resembling its cousin Wal-Mart.

Wade S. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and client accounts do have direct long positions in AMZN and WMT at the time article was originally posted. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}