Posts tagged ‘Amazon’

Investors Slowly Waking to Technology Tailwinds

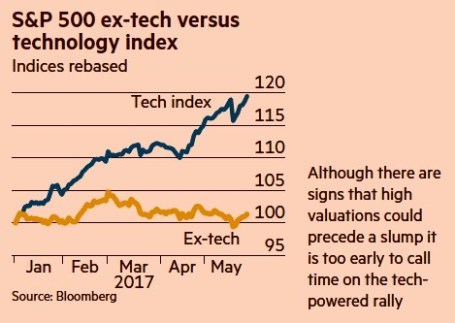

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

“1001 Truths about Investing” Released!

Hot off the printing presses, the much anticipated follow-up book, 1001 Truths about Investing, from Sidoxia Capital Management President and hedge fund manager Wade Slome has arrived.

With Valentine’s Day around the corner, what better way to tell your loved one or special friend that you truly care for them than by purchasing a copy of 1001 Truths. Okay, maybe the purchase wouldn’t be the most romantic gift, but investment portfolios need love too, and adding this to your book collection may be exactly what the investment doctor ordered.

Click Here for the 1001 Truths Press Release

Click Here to Purchase Book on Amazon.com

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AMZN, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Amazon: Growing Up to be Wal-Mart

Wal-Mart (WMT) got its start almost 50 years ago with its first store in Rogers, Arkansas (1962). Since then, the company has expanded to create a global franchise generating more than $400 billion in revenues with a market capitalization valued at about $190 billion. Amazon.com Inc. (AMZN) is a relative toddler (founded in 1995 by CEO Jeff Bezos) generating about $20 billion in revenue with a market cap about 1/5th that of Wal-Mart. Mr. Bezos graduated summa cum laude, Phi Beta Kappa in electrical engineering and computer science from Princeton University in 1986, and we know he has no problem in thinking big. The evidence can be found in his space travel company, Blue Origin, which is expected to initiate human travel in the upcoming years. Beyond space, Mr. Bezos is presented with a multitude of growth opportunities that have the potential of elevating Amazon from a young toddler into a mature adult like its cousin Wal-Mart.

So how does Mr. Bezos get the company through puberty to adulthood? Well actually, all I believe it will take is just more of the same. The company has created an incredible franchise with huge barriers to entry, if you consider the billions spent on the technology, infrastructure, and its distribution dominance as compared to its e-commerce brethren. Bolting on new categories (whether its jewelry, sporting goods, groceries, private label or digital downloads) can be extremely profitable since unlike Wal-Mart, Amazon doesn’t need to build or reconfigure thousands of stores to expand into new categories. For example, Wal-Mart has opened over 600 Sam’s stores nationally in order to target the wholesale club market. Once a new category is added, the blue-print is rolled out nationally and then eventually internationally. And just like Wal-Mart, as economies of scale are achieved, the cost savings are rolled back into lower prices, which then brings more customers, and even more scale advantages. This virtuous cycle then creates deeper and deeper moats separating itself from competitors.

GROWTH OPPORTUNITIES

Besides just the natural expansion of users purchasing more online and Amazon adding to existing categories, here are some other fertile areas for future growth:

- Amazon Prime (Free shipping membership is driving incremental revenue and usage).

- Kindle (This digital reader is already estimated to account for 35% of Amazon’s book sales and some analysts see $2 billion in Kindle revenues by 2012).

- Zappos.com (This acquisition provides instant dominance in shoes and adjacent product lines).

- International Expansion (Joyco.com acquisition in China is an example of how Amazon is expanding into emerging markets).

- New Categories (There are virtually limitless potential categories, but the migration to digital will be key).

- Cloud Computing, Storage & Other Services (EC2 cloud computing, S3 storage, and other outsourced technology services offer promising opportunities).

TREND IS AMAZON’S FRIEND

Source: U.S. Department of Commerce

E-Commerce sales account for only about 3.6% of total retail sales ($32.4 billion in Q2’09), but as you can see from the chart, the upward sloping trend is the friend of Amazon. With the proliferation of broadband and the natural aging of our next generation of computer-savvy internet users, not only is the number of online shoppers increasing, but the amount of time spent online is escalating as well. If you consider catalog sales (e.g. Land’s End, L.L. Bean, Eddie Bauer, etc.) have represented about 7-8% of total retail sales, there is a lot of head-room left for online sales to catch-up or replace these sales. Mr. Bezos believes online industry sales can ultimately reach 15% of total retail sales (double catalog sales). Top-rate online franchises like Amazon will be natural beneficiaries of these trends and funnel shoppers through their internet aisles, as a function of these demographic and behavioral tailwinds.

CAPITAL ADVANTAGE

Even when you account for the significantly higher revenue growth rates and growth initiatives (e.g., Kindle, E3, digital, etc) for Amazon relative to Wal-Mart, the capital intensity (as measured by CAPEX/Sales) is still about 70% higher for Wal-Mart as compared to Amazon. For one thing, Amazon does not need to support the some 8,100 stores in 15 countries that Wal-Mart is saddled with, and in turn Amazon can redeploy that capital into areas such as new products, services, and lower delivery costs. Surviving the dot-com bubble bursting, along with paying down billions of debt has afforded Amazon even more capital flexibility.

VALUATION

Valuation can be tricky, especially when you’re talking about a high growth company like Amazon. The exercise becomes a little easier once you realize Amazon is generating about $1.5 billion in free cash flow per year, with $4.3 billion in cash/investments on the balance sheet with virtually no debt in the middle of one of the worst recessions in a generation. At roughly $90 per share, AMZN is trading at over 53x’s Wall Street analysts’ projected earnings of $1.68 for 2009. Jeff Bezos and the rest of the management make it very clear the company is managing their business to one key goal – maximize free cash flow per share (music to my ears – see my article on cash flow). On that basis, AMZN trades at about 25x’s trailing free cash flow and closer to 22x’s if you strip out the $4 billion+ in cash on the balance sheet. If AMZN can grow 15% for the next 5 years (not a given), the valuations just mentioned above could be chopped in half, if price levels and share count remained constant.

With the large run-up in 2009, I have locked in some gains this year, but tactically I will be doing what “Deep Throat” advised in the movie All the President’s Men, and that is to follow the money (cash). If Bezos and Amazon can continue on its current growth trajectory in the coming years, this toddler will mature into a company more closely resembling its cousin Wal-Mart.

Wade S. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and client accounts do have direct long positions in AMZN and WMT at the time article was originally posted. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}