Posts tagged ‘acquisitions’

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

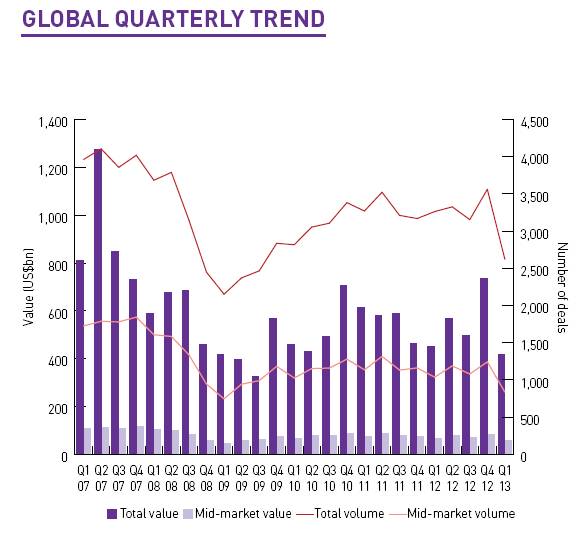

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

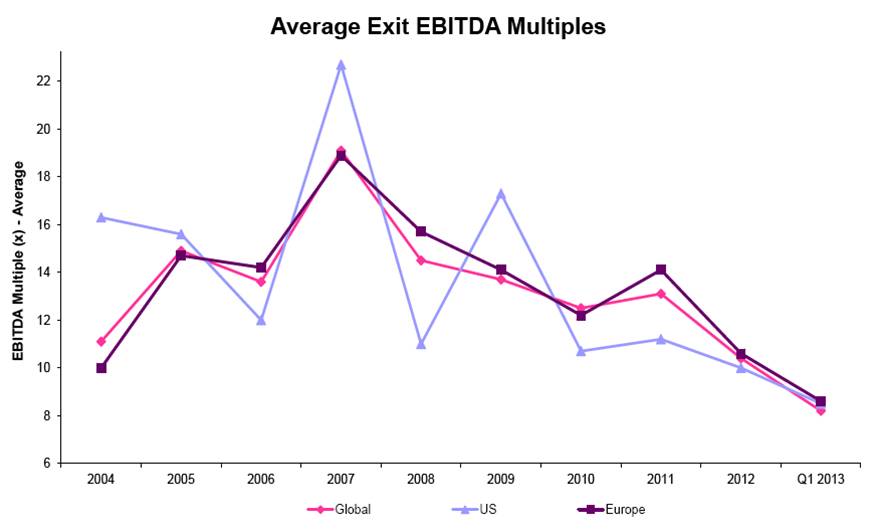

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Killing Patients to Investment Prosperity

All investors are optimistic, every time they open up a position, but just like surgeons, sometimes the outcome doesn’t turn out as well as initially anticipated. When it comes to investing, I think this old Hindu proverb puts things into perspective:

“No physician is really good before he has killed one or two patients.”

So too, an investor does not become really good until he kills off some investment positions. But like surgeons, investors also have to understand the most important aspect of tragic events is learning from them. In many cases, unexpected outcomes are out of our control and cannot be prevented. This conclusion, in and of itself, can provide valuable insights. But on many occasions, there are procedures, processes, and facts that were missed or botched, and learning from those mistakes can prove invaluable when it comes to refining the process in the future – in order to further minimize the probability of a tragic outcome.

My Personal Killers

Professionally, I have killed some stocks in my career too, or they have killed me, depending on how you look at the situation. How did these heartrending incidents occur? There are several categories that my slaughtered stocks fell under:

- Roll-Up, Throw-Up: Several of my investment mistakes have been tied to roll-up or acquisition-reliant growth stories, where the allure of rapid growth shielded the underlying weak fundamentals of the core businesses. Buying growth is easier to create versus organically producing growth. Those companies addicted to growth by acquisition eventually experience the consequences firsthand when the game ends (i.e., the quality of deals usually deteriorates and/or the prices paid for the acquisitions become excessive).

- Technology Kool-Aid: Another example is the Kool-Aid I drank, during the technology bubble days, related to a “story” stock – Webvan, a grocery delivery concept. How could mixing Domino’s pizza delivery (DZP) with Wal-Mart’s (WMT) low-priced goods not work? I’m just lazy enough to demand a service like that. Well, after spending hundreds of millions of dollars and never reaching the scale necessary to cover the razor thin profit margins, Webvan folded up shop and went bankrupt. But don’t give up hope yet, Amazon (AMZN) is refocusing its attention on the grocery space (mostly non-perishables now) and could become the dominant food delivery retailer.

- Penny Stocks = Dollars Lost: Almost every seasoned investor carries at least one “penny stock” horror story. Unfortunately for me, my biotech miracle stock, Saliva Diagnostics (SALV), did not take off to the moon and provide an early retirement opportunity as planned. On the surface it sounded brilliant. Spit in a cup and Saliva Diagnostic’s proprietary test would determine whether patients were infected with the HIV virus. With millions of HIV/AIDS patients spread around the world, the profit potential behind ‘Saliva’ seemed virtually limitless. The technology unfortunately did not quite pan out, and spit turned into tears.

The Misfortune Silver Lining

These stock tragedies are no fun, but I am not alone. Fortunately for me, and other professionals, there is a nine-lives feline element to investing. One does not need to be right all the time to outperform the indices. “If you’re terrific in this business you’re right 6 times out of 10 – I’ve had stocks go from $11 to 7 cents (American Intl Airways),” admitted investment guru Peter Lynch. Growth stock investing expert, Phil Fisher, added: “Fortunately the long-range profits earned from really good common stocks should more than balance the losses from a normal percentage of such mistakes.”

Warren Buffett takes a more light-hearted approach when he describes investment mistakes: “If you were a golfer and you had a hole in one on every hole, the game wouldn’t be any fun. At least that’s my explanation of why I keep hitting them in the rough.”

Some investors purposely forget traumatic investment experiences, but explicitly sweeping the event under the rug will do more harm than good. So the next time you suffer a horrendous stock price decline, do your best to log the event and learn from the situation. That way, when the patient (stock) has been killed (destroyed), you will become a better, more prosperous doctor (investor).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, and AMZN but at the time of publishing SCM had no direct position in DZP, Webvan, Saliva Diagnostics, American intl Airways, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Buffett on Gold Fondling and Elephant Hunting

Warren Buffett is kind enough to occasionally grace investors with his perspectives on a wide range of subjects. In his recently released annual letter to shareholders he covered everything from housing and leverage to liquidity and his optimistic outlook on America (read full letter here). Taking advice from the planet’s third wealthiest person (see rankings) is not a bad idea – just like getting basketball pointers from Hall of Famer Michael Jordan or football tips from Pro Bowler Tom Brady isn’t a bad idea either.

Besides being charitable with billions of his dollars, the “Oracle of Omaha” was charitable with his time, spending three hours on the CNBC set (a period equal to $12 million in Charlie Sheen dollars) answering questions, all at the expense of his usual money-making practice of reading through company annual reports and 10Qs.

Buffett’s interviews are always good for a few quotable treasures and he didn’t disappoint this time either with some “gold fondling” and “elephant hunting” quotes.

Buffett on Gold & Commodities

Buffett doesn’t hold back on his disdain for “fixed-dollar investments” and isn’t shy about his feelings for commodities when he says:

“The problem with commodities is that you are betting on what someone else would pay for them in six months. The commodity itself isn’t going to do anything for you….it is an entirely different game to buy a lump of something and hope that somebody else pays you more for that lump two years from now than it is to buy something that you expect to produce income for you over time.”

Here he equates gold demand to fear demand:

“Gold is a way of going long on fear, and it has been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money, but the gold itself doesn’t produce anything.”

Buffett goes on to say this about the giant gold cube:

“I will say this about gold. If you took all the gold in the world, it would roughly make a cube 67 feet on a side…Now for that same cube of gold, it would be worth at today’s market prices about $7 trillion dollars – that’s probably about a third of the value of all the stocks in the United States…For $7 trillion dollars…you could have all the farmland in the United States, you could have about seven Exxon Mobils (XOM), and you could have a trillion dollars of walking-around money…And if you offered me the choice of looking at some 67 foot cube of gold and looking at it all day, and you know me touching it and fondling it occasionally…Call me crazy, but I’ll take the farmland and the Exxon Mobils.”

Although not offered up in this particular interview, here is another classic quote by Buffett on gold:

“[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

For the most part I agree with Buffett on his gold commentary, but when he says commodities “don’t do anything for you,” I draw the line there. Many commodities, outside of gold, can do a lot for you. Steel is building skyscrapers, copper is wiring cities, uranium is fueling nuclear facilities, and corn is feeding the masses. Buffett believes in buying farms, but without the commodities harvested on that farm, the land would not be producing the income he so emphatically cherishes. Gold on the other hand, while providing some limited utility, has very few applications…other than looking shiny and pretty.

Buffett on Elephant Hunting

Another subject that Buffett addresses in his annual shareholder letter, and again in this interview, is his appetite to complete large “elephant” acquisitions. Since Berkshire Hathaway (BRKA/B) is so large now (total assets over $372 billion), it takes a sizeable elephant deal to be big enough to move the materiality needle for Berkshire.

“We’re looking for elephants. For one thing, there aren’t many elephants out there, and all the elephants don’t want to go in our zoo…It’s going to be rare that we are going find something selling in the tens of billions of dollars; where I understand the business; where the management wants to join up with Berkshire; where the price makes the deal feasible; but it will happen from time to time.”

Buffett’s target universe is actually fairly narrow, if you consider his estimate of about 50 targets that meet his true elephant definition. He has been quite open about the challenges of managing such a gigantic portfolio of assets. The ability to outperform the indexes becomes more difficult as the company swells because size becomes an impediment – “gravity always wins.”

With experience and age comes quote-ability, and Warren Buffett has no shortage in this skill department. The fact that Buffett’s investment track record is virtually untouchable is reason enough to hang upon his every word, but his uncanny aptitude to craft stories and analogies – such as gold fondling and elephant hunting – guarantees I will continue waiting with bated breath for his next sage nuggets of wisdom.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities) and commodity related equities, but at the time of publishing SCM had no direct position in BRKA/B, XOM or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

From Merger Wedding to eHarmony

Source: Photobucket

“Keep your eyes wide open before marriage, and half-shut afterwards.”

– Benjamin Franklin

Stocks share a lot of the same dynamics with dating and marriage. Some may choose to play the field through partnerships and joint ventures, while others may choose to remain independent as eternal bachelors/bachelorettes. Others, however, are willing to take the plunge. Unfortunately some marriages don’t last. But if things don’t work out, there is no need to worry because eHarmony.com (or resident investment bank) will always be there to help find your next perfect match.

Unlucky in Love

An example of a bloody divorce is the mega-merger between AOL Inc. and Time Warner (TWX) in 2000. The relationship was so destructive that investors witnessed AOL’s peak value of $222 billion in December 1999 (Fortune) plummet to around $3 billion today…ooooph!

Compared to some relationships, AOL lasted much longer. In fact Yahoo! Inc. (YHOO) didn’t even get to celebrate a honeymoon with Microsoft Corp. (MSFT) in February 2008 when the behemoth software company offered a +62% premium ($31 per share) for the gigantic portal. Microsoft’s $45 billion cash and stock offer was ruled unworthy by Yahoo’s board, so the company decided to leave Microsoft at the altar. Even after considering Yahoo’s latest price spike on acquisition rumors, Microsoft’s original bid is still almost double Yahoo’s current stock price of $16 per share.

Merger Scuttlebutt

As I discussed in my earlier mergers and acquisitions article (M&A) conditions are ripening with large corporate cash piles, a continued economic recovery, improved capital markets availability, and cheap credit costs (at least for those that qualify). With the clouds slowly lifting in the M&A world, suitors are shaking the trees for more potential opportunities.

While some acquirers may have altruistic intentions in combining companies, some marriages are done for pure gold-digging purposes. Private equity firms Blackstone Group (BX) and Silver Lake are rumored to be circling the Yahoo wagons and courting AOL as a potential partner in a joint bid. Whatever the expectations, if private equity plays a role in a Yahoo bid, the internet company should not become disillusioned with romantic warm and fuzzies – private equity firms like to get straight down to dirty business. Yahoo owns a 35% stake in Yahoo Japan and a 43% interest in leading Chinese e-commerce company, Alibaba Group. If a joint private equity bid were ever to win, I believe there would be a strong impetus to realize shareholder value by carving up these non-operating stakes. Consolidating overhead and streamlining expenses would likely be a top priority as well.

The Perfect Marriage

A “perfect marriage” could almost be called an oxymoron because like any relationship, there is significant work required by both parties. The divorce rate is estimated at around 40-50% in North America (Europe around the same), however mergers even fail at a higher 70% rate, according to Bain and Company study. I would argue successfully integrating larger deals are even more difficult, hampering the success rate even further. Merging two poorly managed companies purely for cost purposes is probably not the best way to go. Crashing two garbage trucks together is not going to create a Ferrari. I wouldn’t go as far as to say Yahoo and AOL are garbage trucks, but they face numerous, substantial challenges. Maybe these two companies are more akin to Mazdas transforming into a Toyota Camry (TM).

From my perspective, if companies really are dead set on engaging in acquisitions, then I urge management teams to focus on smaller digestible deals. Specifically, concentrate on those deals with experienced senior management teams who understand and respect the unique culture of the acquirer. Mergers also often fail due to excessive optimism and overly optimistic assumptions. This is an area in which Warren Buffett excels. Rarely do you observe the Oracle of Omaha overpaying for an acquisition, but rather he patiently waits for his fat pitch, and when it floats over the plate, Buffett is quick to throw out a lowball offer that will dramatically increase the probabilities of long-term merger success (think Geico, Sees Candy, Burlington Northern, etc.).

In the end, a joint relationship may not be forged between Yahoo, AOL and private equity firms, but if talks disintegrate, no need to worry – alternative partnerships can be explored on eHarmony.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in YHOO, MSFT, TWX, BX, BRKA, TM, Alibaba, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Winner’s Curse: HP’s Storage Prize

Congratulations HP (HPQ)…you are the proud winner of 3Par Inc. (PAR), a relatively small enterprise storage hardware and software company, for the bargain price of 125x’s 2011 earnings! Never mind that you were late to the game in your winning $2.4 billion bid against Dell Inc. (DELL), or that you paid more than triple the price ($33 per share) that 3Par was trading just 21 days ago (< $10 per share). At least you have a storage trophy you can show all your friends and you don’t have to carry around all those heavy bills anymore.

Winner’s Curse

In bidding wars and auctions, the victor of the price battle runs the risk of earning the “Winner’s Curse.” The curse falls upon those that bid a price that exceeds an auctioned asset’s intrinsic value. How can this occur? Well for one reason, the bidder may not have complete information regarding the value of the asset. Secondly, there can be emotional factors, or ego, that play a role in the decision and price paid. Lastly, unique factors, such as strategic benefits or synergies may exist that allow one bidder to offer a higher price than other auction participants. For example, consider an exploration and production company (XYZ Drilling Co.) that is bidding for drilling lease rights in Prudhoe Bay, Alaska. If XYZ Drilling Co. has unique existing drilling operations in the same area as the auctioned assets, XYZ Drilling Co. may be in a better position of making a profitable bid relative to its peers.

HP vs. Dell – A Deeper Look

Let’s take a deeper dive into the HP bid of 3Par. While HP generates a lot of cash by selling printers, cartridges, and computers, the company doesn’t exactly have a bullet-proof balance sheet. Unlike let’s say Apple Inc. (AAPL), which has about $46 billion in cash on its balance sheet with no debt (see Steve Jobs: Gluttonous Hog), HP actually carries more debt than cash (about $20 billion in debt and $15 billion in cash). What’s more, HP has little tangible equity, once $42 billion in goodwill and intangible assets are subtracted from the total asset value of the company – leaving HP with an astronomically high ratio of 275x’s price to tangible book value. For most companies operating with a positive net cash position, making acquisitions accretive is not that difficult in this current environment – when cash is decaying away with a paltry 1% return. Unfortunately for HP, their accretive hurdle is higher than a cash-rich company. Their weighted average cost of capital is ratcheted significantly higher due to a net debt position (not net cash).

Here is the viewpoint on the deal from Ashok Kumar, senior technology analyst at Rodman & Renshaw LLC:

“It’s in excess of $3 million per employee. To put it in perspective, today 3Par has about 5 percent [market share] of the very high-end market and for these premiums to pay out, [HP] would have to expand their market share to about 25 percent or about $1.5 billion, which is 5x the projected growth rate. And all of that would come at the expense of incumbents [like] IBM, EMC, Hitachi.”

On the Bright Side

Although the price paid by Hewlett-Packard for 3Par is ridiculously too high, this deal alone is not going to break HP’s piggybank. HP is currently raking in about $8 billion in cash flow per year, so absent aggressive share buybacks or other large acquisitions, HP should be able to pay off the cost of the deal in a few quarters. Secondarily, HP does gain some synergies by integrating 3Par’s blocklevel data storage expertise into HP’s existing portfolio of other storage technologies ( i.e., StoreOnce and IBRIX). Thirdly, HP gains some strategic defensive benefits by keeping 3Par out of Dell’s hands, a potentially formidable competitor in the storage space, given the intensive overlap in customer bases between HP & Dell. Lastly, HP will no doubt be able to introduce and cross-sell 3Par products into Hewlett’s vastly larger customer distribution channels and reap the resulting rewards.

All in all, the 3Par acquisition by HP makes perfect strategic sense, however the price paid will turn out to be a much better deal for 3Par shareholders, rather than HP shareholders. HP ultimately shelled out a hefty price tag to become the victorious party in the 3Par bidding war, but rather than increasing shareholder value, HP ended up achieving the “Winner’s Curse.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in HPQ, PAR, DELL, IBM, EMC, Hitachi, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity: Hitting Maturity Cliff

Photo source: 1Funny.com

Wow, those were the days when money was as cheap and available as that fragile, sandpaper-like toilet paper you find at gas stations. Private equity took advantage of this near-free, pervasive capital and used it to the greatest extent possible. The firms proceeded to lever up and gorge themselves on a never-ending list of target companies with reckless abandon (see also Private Equity Shooting Blanks). Now the glory days of abundant, ultra-cheap capital are history.

Rather than rely on low-cost bank debt, private equity firms are now turning to the fixed income markets – specifically the high yield market (a.k.a. junk bonds). As The Financial Times points out, more than $170 billion of junk bonds have been issued this year, in large part to refinance debt issued in the mid-2000s that has gone sour due to overoptimistic projections and a flailing U.S. economy. In special instances, private equity owners are fattening their own wallets by declaring special dividends for themselves.

Even though some of these over-levered, private equity portfolio companies have received a temporary reprieve from facing the harsh economic realities thanks to these refinancings, the cliff of maturing debt in 2012 is fast approaching. Some have estimated that $1 trillion in maturing debt will roll through the market in the 2012-2014 timeframe. Either the economy (or operating performance) improves enough for these companies to service their debt, or these companies will find themselves falling off these maturity cliffs into bankruptcy.

Junk is Not Risk-Free

Driving this trend of loan recycling is risk aversion to stocks and a voracious appetite for yield in a yield desert. Stuffing the money under the mattress, earning next to nothing on CDs (Certificates of Deposit) and money market accounts, will not help in meeting many investors’ long-term objectives. The “uncertain uncertainty” swirling around global equity markets has nervous investors flocking to bonds. The opening of liquidity in the high yield markets has served as a life preserver for these levered companies desperate to refinance their impending debt. This high-yield debt refinancing window is also an opportunity for companies to lower their interest expense burden because of the current, near record-low interest rates.

But as the name implies, these “junk bonds” are not risk free. For starters, embedded in these bonds is interest rate risk – with a Federal Funds rate at effectively zero, there is only one upward direction for interest rates to go (bad for bond prices). In addition, credit risk is a concern as well. In the midst of the financial crisis, many of these high-yield bonds corrected by more than -40% from their highs in 2008 until the bottom achieved in early 2009. If the economy regresses back into a double-dip recession, many of these bonds stand to get pummeled as default rates escalate (see also, bond risks).

Pace Not Slowing

Source: Dealogic via WSJ

Does the appetite for high yield appear to be slowing? Au contraire. In the most recent week, Dealogic noted $15.4 billion in junk bonds were sold. The FT sees the pace of junk deals handily outpacing the record of $185.4 billion set in 2006.

The Wall Street Journal used the following deals to provide a flavor of how companies are using high-yield debt in the present market:

“First Data Corp. sold $510 million of 10-year notes this week, at 9.125%, to pay down bank debt due in 2014. Peabody Energy sold $650 million of 6.5%, 10-year notes to pay off the same amount of higher-priced debt due in three years. MultiPlan Inc., a health-care cost-management provider, sold $675 million of notes this week, at 9.875%, to help fund a buyout of the company. Cott Corp., a maker of store-branded soft drinks, sold $375 million of debt at 8.125% to fund its purchase of another company, Cliffstar Corp.”

The roads on the junk bond highway appear to be pothole free at the moment, however a cliff of debt is rapidly approaching over the next few years, so high-yield investors should travel carefully as conditions in the junk market potentially worsen. As we witnessed in 2008-2009, it can take a while to hit rock bottom in the riskier areas of the credit spectrum.

Read full Financial Times and Wall Street Journal articles on the high yield market.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including HYG and JNK), but at the time of publishing SCM had no direct position in First Data Corp., Peabody Energy (BTU), MultiPlan Inc., Cott Corp. (COT), Cliffstar Corp., or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Jobs: The Gluttonous Cash Hog

Really? Do you think Steve Jobs actually needs to hoard $42 billion in cash reserves on the company’s balance sheet, when they are already adding to the gargantuan mountain of money at a $12 billion clip per year. Let’s not forget, this gaudy amount of money is being added after all operating expenses and capital expenditures have been paid for.

Perhaps Steve is just a little worried about the economy, and wants a little extra loose change around for a rainy day? I’d buy that argument, but Mr. Jobs and the rest of the executives just witnessed the worst financial crisis in a generation, and the company still managed to generate about $9 billion in free cash flow in both fiscal 2008 and 2009.

If Apple was not creating cash flow like those cascading chocolate fountains I see at wedding receptions, then perhaps a cash safety blanket is needed for acquisitions? Here’s what Steve had to say about Apple’s cash levels in February:

Steve Jobs (Source: Photobucket)

“We know if we need to acquire something – a piece of the puzzle to make something big and bold – we can write a check for it and not borrow a lot of money and put our whole company at risk…The cash in the bank gives us tremendous security and flexibility.”

Let’s explore that idea a little further. First of all, what type of experience does Apple have in doing large acquisitions? Not a lot, and just to humor myself I ran a screen on a universe of more than 10,000 stocks and I came up with 111 companies with a value (market capitalization) greater than $40 billion. Unless Apple plans on buying companies like Coca Cola (KO), Chevron Corp. (CVX), Pfizer (PFE), or United Parcel Service (UPS), I think Apple can part ways with some of their billions. Certainly, there are a handful of theoretical targets in the areas of technology and content, but for certain, (a) any large deal would face intense regulatory scrutiny, and (b) if truly there were grand synergies from doing a massive deal, then most definitely they would be able to issue stock (if Jobs hates debt) to help fund the deal. It is pure nonsense and laughable to believe any “big and bold” acquisition would put the company “at risk.” The only thing at risk for doing a large deal would be Apple’s stock price.

The truth of the matter is returning cash to shareholders would be a fantastic self-disciplining tool, like putting mayonnaise on a brownie to prevent excess calorie consumption. Steve should give current or former CEOs of AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, and Nextel a call to see how those large deals worked out for them. Apple could use an acquisition security blanket, but they do not need a circus tent of cash.

Times of Change

Although times have changed, some executives have not. Many tech companies, including Apple, have nostalgic memories of the go-go tech bubble days of the 1990s when growth at any price was the main mantra and no attention was paid to prudent capital allocation. With a stagnant stock market over the last twelve years, and interest rates sitting sluggishly at record lows (effectively 0% on the Federal Funds rate), investors are demanding prudent decision-making when it comes to capital allocation. Mr. Jobs, it is time to expand your narrow views and show the stewardship of sensibly managing the cash of your loyal investors.

Believe it or not, there are still a few of us actual “investors” that still exist. I’m talking about investors who do not just speculatively rent a stock for a day, week, or month, but rather those who invest for the long-term because they believe in the vision and execution capabilities of management and believe the company’s capital will be invested in their best interest.

I do not mean to single Mr. Jobs out, because he is not the only gluttonous, cash-hog offender among CEOs. In many respects, Apple has the good fortune of becoming a cash-hoarding poster child. The company does indeed deserve credit for becoming a $225 billion technology-consumer-media-retail juggernaut that has spread its tentacles brilliantly across numerous massive markets, whether its PCs, cell phones, music, television, movies, games, advertising etc.…you get the picture. But just because you are an exceptionally gifted visionary doesn’t give you the right to destroy value of hopelessly idle cash, which is begging for a better home than a 0.25% T-Bill.

Solutions – Taming the Cash Hog:

1) Divvy Up Dividends: With $42 billion in cash on the balance sheet and additional annual free cash generation on pace for $12 billion per year, there is no reason Steve Jobs and the board couldn’t declare a dividend that would yield 3% today. If that feels like too much, then how about shave off a pittance of $5 billion or so to pay out a sustainable dividend, which would yield a market-matching 2% dividend yield to investors. This scenario would accommodate Apple with at least a few decades of a cash cushion to cover ALL the company’s operating expenses and capital expenditures. This meagerly, ultra-conservative dividend policy can actually persist (or grow) longer than expected, if Apple can sustainably grow profits – a good possibility.

2) Share Buyback: This solution is much less desirable from my perspective compared to the dividend route, since many of the large share repurchasers tend to also issue lots of new shares to employees and executives, thereby neutering the benefits of the share repurchases.

3) Bank of Apple – (B of A): Why doesn’t Jobs just create a new entity, plop $40 billion of cash from Apple Inc. into the venture, and then open it up as Bank of Apple. At least that way, as an investor in the bank, I could make more profitable lending spreads at B of A relative to the 0.25% yield earned on the mega-billions deteriorating on Apple’s corporate balance sheet.

The downside of instituting these cash reducing solutions:

- The company doesn’t have as much cash as it would like to do large stupid acquisitions.

- The company loses a bunch of day-traders and short-term stock renters that don’t even know what a dividend is.

The upside to efficiently allocating capital through a 2% dividend is Steve (and the other investors) will receive a nice fat quarterly check. In the case of Jobs, he’ll collect a handsome $27 million or so to his measly $1 annual salary. In the process, the company will also gain long term shareholders that buy into the strategic vision of the company.

Stubbornness has served Steve Jobs tremendously well in his career, and a successful CEO like Steve Jobs is not required to listen to my advice. However, I am hopeful that Mr. Jobs will see the hazards of choking on a rapidly growing $42 billion cash hoard and discover the benefits of slimming down a gluttonous cash hog.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct positions in KO, CVX, PFE, UPS, AOL, Time Warner, Mercedes Benz, Chrysler, Sprint, Nextel, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Google: The Quiet Steamroller

As Google Inc. (GOOG) has proceeded to steamroll most of its competition on the global advertising roads, they are learning to tread a little more lightly in hopes of avoiding unneeded scrutiny. There are very few places to hide, when your company is on track to achieve more than $20 billion in annual sales and is valued at more than $175 billion in the marketplace.

As Google revenues continue to rise and they look to take over the world (including their position in China), they are enlisting others to assist them in Washington as well. Through three quarters of 2009, the company increased their lobbyist budget by 41% to approximately $3 million, according to the Associated Press (AP).

Google Eating Bite Sized Acquisitions

Ever since the controversy caused by Google’s $3.1 billion takeover of web advertising network company DoubleClick (2007 announcement), and the failed joint search agreement with Yahoo! (YHOO) in 2008 due to government and advertiser concerns, Google has decided to consume smaller bite-sized companies as part of its acquisition strategy. Over the last five months alone, Google has acquired eight different small companies (generally less than $50 million acquisition price), including the following: 1) Picknik (photo editing website); 2) reMail (mobile search applications); 3) Aardvark (social networking focus); and 4) AdMob ($750 million mobile advertising network deal). Eric Schmidt, Google CEO, has stated he would like to do one smaller-sized acquisition per month. Google management also believes they have lowered the inherent risk in these smaller deals because of legacy ties to target companies – all these sought after companies house former Google employees, says Bloomberg. In addition to remaining below the radar, the string of small deals act as a supplement to Google’s hiring practices, which can become challenging in a scarce qualified engineering hiring environment.

Microsoft Pot Calling Kettle Black

Microsoft (MSFT), the behemoth software giant with monopoly-like market share in the PC operating system market, is now fighting back against growing giant Google. This effectively amounts to the pot calling the kettle black, given Microsoft has already paid about $2.44 billion in fines to EU (European Union) relating to antitrust actions in the past 10 years, according to TechCrunch. Nonetheless, Microsoft CEO Steve Ballmer is not shy about throwing Google under the bus, stating Google is not playing fair in the search market. Furthermore, Microsoft has filed an antitrust complaint against Google in Europe as it relates to Ciao, an online shopping service powered by Microsoft, and cried foul over an agreement Google made with book publishers and authors on a separate project.

Google is not stupid. They have witnessed massive monopolistic companies like Microsoft and Intel (INTC) butt heads with regulators and pay billions in fines. Needless to say, Google will do everything in its power to avoid additional, unwanted oversight, while quietly driving their steamroller over the competition.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and GOOG, but at time of publishing had no direct position in MSFT, INTC, YHOO, or any other security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The China Vacuum, Sucking Up Assets

That's not Hoover making that sucking noise - it's China

Shhh, if you listen hard enough you can hear a faint sucking sound coming from the other side of the Pacific Ocean. In the midst of the greatest economic collapse since the Great Depression, China is rolling around the globe sucking up international assets as if it were a Hoover vacuum cleaner. As a member of the current account and budget surplus club, China is enjoying the membership privileges. Evidence is apparent in several forms.

Most recently, Chinese state oil and gas company, Sinopec (China Petrochemical Corporation) has bid close to $7 billion for Addax Petroleum, an oil explorer with significant energy assets in the Kurdistan region of northern Iraq.

Another deal, newly announced not too long ago, occurred on our own soil when another Chinese company (Sichuan Tengzhong Heavy Industrial Machinery Co.) made a bid for the ailing Hummer unit of bankrupt General Motors. Just as we have begun exporting our obesity to China through McDonald’s and KFC, now we are sharing our lovely gas guzzling habits.

In May, The Wall Street Journal reported the following:

Chinese companies and banks have also agreed to a string of credit and oil supply deals worth more than US$40 billion with countries such as Brazil, Russia and Kazakhstan, in line with efforts to secure its energy supply.

Beyond the oil markets, China is also hungry for other hard assets. The failed $20 billion investment in Chinalco (Aluminum Corporation of China) by Rio Tinto garnered a lot of press. But other deals are making headlines too. Metallurgical Corp. of China Ltd. (MCC) is planning a $5.15 billion thermal coal project in Queensland state, Australia in conjunction with Waratah Coal Pty Ltd. China has a voracious appetite for coal -its coal imports are estimated to surpass 50 million tons in 2009.

Cash is king, especially in crises like we are experiencing now, however we want to be careful that we don’t give away the farm out of desperation. Making tough decisions to preserve assets, like cutting expenditures and expenses, is a better strategy versus making fire sale disposals of crown jewels. Becoming energy independent and investing in environmentally sustaining technologies will serve our long term economic interests better as well.

If we’re not careful, that active Chinese Hoover vacuum cleaner is going to come over to our home turf and suck up more than just our loose change.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, RTP and was short MCD, but at the time of publishing SCM had no direct position in YUM, Sinopec (China Petrochemical Corporation), Addax Petroleum, Chinalco (Aluminum Corporation of China), Metallurgical Corp. of China Ltd. (MCC),Waratah Coal Pty Ltd or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}