Betting on Green: Not All Performance is Equal

Not all performance is created equally. Now is the time of year where professional money managers jockey for position before year-end, either with the intent of locking in above-average performance or throwing up a Hail Mary pass in hopes of gaining lost performance ground. Typically, top performing managers are lauded for their eye-popping returns and shrewd investing acumen, when in fact, often these managers have been playing a game of roulette in which a risky, low probability strategy of betting on “green zero” has paid off (a winner about 2.6% of the time).

With tens of thousands hedge fund managers, mutual fund managers, and investment advisors self-reporting their results, even if the performance is accurate, the “Law of Large Numbers” dictates a small percentage will outperform. In other words, short-term luck can often trump long-term skill in the investment world, so investors really need to take a look under the covers to better understand the composition of the results.

Here are some factors contributing to performance distortions and misunderstandings:

Leverage: Adding leverage to your investment strategy is a lot like switching from a bicycle to a motorcycle. The new vehicle may get you to your destination faster, but the risks are lot higher than riding a bike, including death. The same principles apply to investing. A leveraged portfolio may be a fun ride when prices appreciate, but the agony on the downside can be equally painful in reverse. Often, many managers obscure the amount of leverage, and point to absolute returns rather than risk-adjusted returns, which rightfully account for the underlying volatility of the security or investment. To better measure investment performance on an apples-to-apples basis, risk-adjusted ratios such as Sharpe ratios and Treynor ratios should be used.

Concentration/Style Drift: Similarly to playing a game of roulette, putting all your money on black can result in a very handsome payout, but the downside can be just as severe. In the late 1990s growth managers benefited tremendously by concentrating their portfolios into technology stocks because prices appreciated virtually unabated. Many value managers succumbed to style drift by abandoning their value investment mandates and chasing performance. Investors should scrutinize the composition of their portfolios to better comprehend the bets managers are making. Excessive concentration or style drift may lead to a rude awakening.

Benchmark Cherry Picking: Buried in the fine print of an investment prospectus or pitchbook, a performance benchmark, which acts like a measuring stick, can usually be found. The non-standardized game of performance reporting is a lot like a beauty contest in which the investment manager can pick ugly competitors to make themselves look better. Typically a manager compares their performance against the worst performing benchmark or index, and if the benchmark performance improves, a manager can again substitute the old benchmark with a newer, uglier one.

Spaghetti Effect: Another misleading marketing strategy used by many investment firms is what I like to call the “Throwing-Spaghetti-Against-the-Wall” technique, which involves throwing as many strategies at investors as it takes and see what sticks. Famed hedge fund manager John Paulson, who made Herculean profits during the collapse of the subprime crisis, used this strategy in hopes of capitalizing on his sudden fame. The results haven’t been pretty over the last few years as his major funds have massively underperformed and assets have collapsed from about $38 billion at the peak to less than an estimated $20 billion now. Paulson has proved that parlaying one successful bet into many spaghetti throwing strategies (Advantage, Advantage Plus, Partners Fund, Enhanced Fund, Credit Opportunities, and Recovery) can lead to billions in gained assets, albeit shrinking.

Window-Dressing: Portfolio managers are notorious for selling their stinkers and buying the darlings at the end of a quarter, just so they can avoid uncomfortable questions from investors. By analyzing a manager’s portfolio turnover (i.e., the average holding period for a position), an investor can gauge how much shuffling is really going on. Generally speaking, managers performing this value-destroying, smoke and mirrors behavior are doing more harm than good due to all the trading costs and frictions.

While periodically reviewing absolute reported returns is important, more critical than that is analyzing the risk-adjusted returns of a portfolio, so apples-to-apples comparisons can be made. Any and all strategies are bound to underperform for periods of time, but in order to make rational investment decisions investors need to truly understand the underlying strategy and philosophy of the manager(s). Without following all these steps, investors will have better luck putting their money on green.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any Paulson funds or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Uncertainty: Love It or Hate It?

Source: Photobucket

Uncertainty is like a fin you see cutting through the water – many people are uncertain whether the fin sticking out of the water is a great white shark or a dolphin? Uncertainty generates fear, and fear often produces paralysis. This financially unproductive phenomenon has also reared its ugly fin in the investment world, which has led to low-yield apathy, and desensitization to both interest rate and inflation risks.

The mass exodus out of stocks into bonds worked well for the very few that timed an early 2008 exit out of equities, but since early 2009, the performance of stocks has handily trounced bonds (the S&P has outperformed the bond market (BND) by almost 100% since the beginning of March 2009, if you exclude dividends and interest). While the cozy comfort of bonds has suited investors over the last five years, a rude awakening awaits the bond-heavy masses when the uncertain economic clouds surrounding us eventually lift.

The Certainty of Uncertainty

What do we know about uncertainty? Well for starters, we know that uncertainty cannot be avoided. Or as former Secretary of the Treasury Robert Rubin stated so aptly, “Nothing is certain – except uncertainty.”

Why in the world would one of the world’s richest and most successful investors like Warren Buffett embrace uncertainty by imploring investors to “buy fear, and sell greed?” How can Buffett’s statement be valid when the mantra we continually hear spewed over the airwaves is that “investors hate uncertainty and love clarity?” The short answer is that clarity is costly (i.e., investors are forced to pay a cherry price for certainty). Dean Witter, the founder of his namesake brokerage firm in 1924, addressed the issue of certainty in these shrewd comments he made some 78 years ago, right before the end of worst bear market in history:

“Some people say they want to wait for a clearer view of the future. But when the future is again clear, the present bargains will have vanished.”

Undoubtedly, some investors hate uncertainty, but I think there needs to be a distinction between good investors and bad investors. Don Hays, the strategist at Hays Advisory, straightforwardly notes, “Good investors love uncertainty.”

When everything is clear to everyone, including the novice investing cab driver and hairdresser, like in the late 1990s technology bubble, the actual risk is in fact far greater than the perceived risk. Or as Morgan Housel from Motley Fool sarcastically points out, “Someone remind me when economic uncertainty didn’t exist. 2000? 2007?”

What’s There to Worry About?

I’ve heard financial bears argue a lot of things, but I haven’t heard any make the case there is little uncertainty currently. I’ll let you be the judge by listing these following issues I read and listen to on a daily basis:

- Fiscal cliff induced recession risks

- Syria’s potential use of chemical weapons

- Iran’s destabilizing nuclear program

- North Korean missile tests by questionable new regime

- Potential Greek debt default and exit from the eurozone

- QE3 (Quantitative Easing) and looming inflation and asset bubble(s)

- Higher taxes

- Lower entitlements

- Fear of the collapse in the U.S. dollar’s value

- Rigged Wall Street game

- Excessive Dodd-Frank financial regulation

- Obamacare

- High Frequency Trading / Flash Crash

- Unsustainably growing healthcare costs

- Exploding college tuition rates

- Global warming and superstorms

- Etc.

- Etc.

- Etc.

I could go on for another page or two, but I think you get the gist. While I freely admit there is much less uncertainty than we experienced in the 2008-2009 timeframe, investors’ still remain very cautious. The trillions of dollars hemorrhaging out of stocks into bonds helps make my case fairly clear.

As investors plan for a future entitlement-light world, nobody can confidently count on Social Security and Medicare to help fund our umbrella-drink-filled vacations and senior tour golf outings. Today, the risk of parking your life savings in low-rate wealth destroying investment vehicles should be a major concern for all long-term investors. As I continually remind Investing Caffeine readers, bonds have a place in all portfolios, especially for income dependent retirees. However, any truly diversified portfolio will have exposure to equities, as long as the allocation in the investment plan meshes with the individual’s risk tolerance and liquidity needs.

Given all the uncertain floating fins lurking in the economic background, what would I tell investors to do with their hard-earned money? I simply defer to my pal (figuratively speaking), Warren Buffett, who recently said in a Charlie Rose interview, “Overwhelmingly, for people that can invest over time, equities are the best place to put their money.” For the vast majority of investors who should have an investment time horizon of more than 10 years, that is a question I can answer with certainty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including BND, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Lily Pad Jumping & Term Paper Cramming

Article is an excerpt from previously released Sidoxia Capital Management’s complementary December 3, 2012 newsletter. Subscribe on right side of page.

Over the last year, investors’ concerns have jumped around like a frog moving from one lily pad to the next. From the debt ceiling debate to the European financial crisis, and then from the presidential election to now the “fiscal cliff.” With the election behind us (Obama winning 332 electoral votes vs 206 for Romney; and Obama 50.8% of the popular vote vs 47.5% for Romney), the frog’s bulging eyes are squarely focused on the fiscal cliff. For the uninformed frogs that have been swimming underwater, the fiscal cliff is the roughly $600 billion in automatic tax hikes and spending cuts that are scheduled to be triggered by the end of this year, if Congress cannot come to some type of agreement (for more fiscal cliff information see videos here). The mathematical consequences are clear: Congress + No Deal = Recession.

While political brinksmanship and theater are nothing new, the explosive amount of data is something new. In our mobile world of 6 billion cell phones (more than the number of toothbrushes on our planet) and trillions of text messages sent annually, nobody can escape the avalanche of global data. Google (GOOG), Facebook (FB), Twitter, and millions of blogs (including this one) didn’t exist 15 years ago, therefore fiscal boogeymen like obscure Greek debt negotiations and Chinese PMI figures wouldn’t have scared pre-internet generations underneath their beds like today’s investors. The fact of the matter is our country has triumphed over plenty of significant issues (many of them scarier than today’s headlines), including wars, assassinations, currency crises, banking crises, double digit inflation, SARS, mad cow disease, flash crashes, Ponzi schemes, and a whole lot more.

Although today’s jumpy investors may worry about the lily pads of a double-dip recession in the US, a financial meltdown in Europe, and/or a hard landing in China, fiscal frogs will undoubtedly be worried about different lily pads (concerns) twelve months from now. This may not be an insightful observation for day traders, but for the other 99% of investors, taking a longer term view of the daily news cycle may prove beneficial.

Fiscal Cliff Term Paper Due on Friday December 21st

As a college student, chugging Jolt Cola, in combination with a couple dosages of NoDoz, was part of the routine procrastination process the day before a term paper was due. Apparently Congress has also earned a PhD in procrastination, judging by the last minute conclusion of the debt ceiling negotiations last summer. There are only a few more weeks until politicians break for the Christmas holiday break, therefore I am setting an Investing Caffeine mandated fiscal cliff due date of December 21st. Could Congress turn in its term paper early? Anything is possible, but unfortunately turning in the assignment early is highly unlikely, especially when politically bashing your opponent is perceived as a better re-election tactic compared to bipartisan negotiation.

A higher probability scenario involves Americans stuck listening to Nancy Pelosi, Harry Reid, John Boehner, and Mitch McConnell on a daily basis as these politicians finger-point and call the other side obstructionists. While I’m not alone in believing a deal will ultimately get done before Christmas, how credible and substantive the announcement will be depends on whether the politicians seriously face entitlement and tax reforms. Regardless, any deal announced by Investing Caffeine’s December 21st due date will likely be received well by the market, as long as a framework for entitlement and tax reform is laid out for 2013.

Frog News Bites

Source: Photobucket

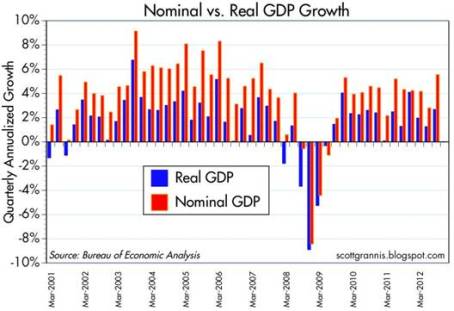

GDP Revised Higher: Despite all the gloom and uncertainties, the barometer of the economy’s health (i.e., Real Gross Domestic Product), was revised higher to 2.7% growth for the third quarter (from 2.0%). Nominal growth, a related measurement that includes inflation, reached a five-year high of 5.55%. In the wake of Superstorm Sandy, which caused upwards of $50 billion in damage, fourth quarter GDP numbers are likely to be artificially depressed. The silver lining, however, is first quarter 2013 figures may get an economic boost from reconstruction efforts.

Source: Calafia Beach Pundit

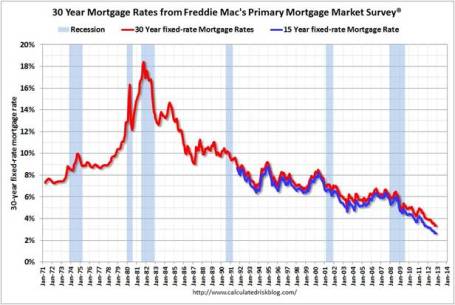

Housing Recovery Continues: Buoyed by record low interest rates (30-yr fixed mortgages < 3.5%), housing sales and prices continue on an upward trajectory. New home sales came in at 368,000 in October, below expectations, but sales are still up around +20% from 2011 (Calculated Risk).

Source: Calculated Risk

Confidence Still Low but Climbing: The recently reported consumer confidence figures reached the highest level in more than four years, but as Scott Grannis highlights, this is nothing to write home about. These current confidence levels match where we were during the 1990-91 and 1980-82 recessions.

Source: Calafia Beach Pundit

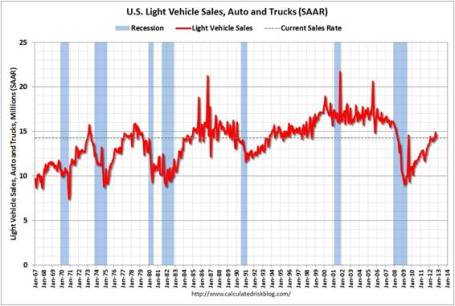

Car Sales Picking Up: Fiscal cliff discussions haven’t discouraged consumers from buying cars. As you can see from the chart below, car and truck sales reached 14.3 million annualized units in October. November sales are expected to rise about +13% on a year-over-year basis, reaching approximately 15.3 million units.

Source: Calculated Risk

CIA Chief Fired in Sex Scandal: If you didn’t get enough of the Lindsay Lohan bar brawl dirt in New York, never fear, there was plenty of salacious details emanating from Washington DC this month. A complicated web of Florida socialites, a biographer, email chains, and a bare-chested FBI agent led to the firing of CIA director David Petraeus.

Source: The Financial Times

Death to Twinkies: After lining stomachs with golden cream-filled cakes for more than 80+ years, Hostess Brands was forced to halt production of Twinkies, Ding Dongs, and Ho Hos. Negotiations with union bakers crumbled, which led to Hostess Brands’ Chapter 7 bankruptcy and liquidation proceedings. My financial brain understands, but my sweet tooth is still grieving (see also Twinkie Investing).

Source: Photobucket

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in FB, Twitter or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Top 10 (or so) Things I’m Thankful For

With the holidays now upon us, this period provides me the opportunity to briefly escape the daily investment rat race, and reflect on the numerous aspects of my life for which I am grateful. There is so much to be thankful for, but it’s easy to lose sight of what’s important, especially when time is flying by in the blink of an eye. As the old saying goes, “Life is like a roll of toilet paper. The closer you get to the end, the faster it goes.” The proliferation of gray hair, coupled with my sprouting kids, is a constant reminder that life is not slowing down for me, but actually speeding up.

As I lay here like a slug on the couch, which is slowly absorbing me, I take no shame in unbuttoning my top pant button to relieve the belly-busting pressure of excessive turkey and mash potato consumption. The cranberry sauce on my chin and pumpkin pie crust on my shirt does not distract me from the football game or prevent me from reflecting upon my life’s gifts.

In that vein, here is a list of my top 10 things for which I am grateful:

10. Sugar: Without sweets, being relegated to a life of bread, water, and broccoli would be a boring challenge. Thankfully, once I became a grown adult earning a paycheck, I also earned the right to eat Cap’n Crunch (with Crunch Berries) for breakfast; peanut butter-Nutella & banana sandwich for lunch; apple fritter & milk for dinner; and some Double Stuf Oreos for dessert (yes, only one ‘f’ in Stuf!).

9. College Sports: Watching professional sports is fun, but when A-Rod earns $275 million for the NY Yankees and rides the pine during the playoffs, the business aspects take a little allure away from the sport. Although college athletes may sneak a few bucks under the table, they are nonetheless a lot less corrupted, and the electric atmosphere of a live college event cannot be replicated. The opportunities are fewer due to adult responsibilities, but nothing beats a crisp fall afternoon on the couch with a bowl of hot chili, a frosty beverage, and a remote control, while flipping through a series of college football games.

8. Gadgets: Seems like yesterday when I was introduced to my first computer, a 1983 Compaq Portable computer that weighed 28 pounds; had a 9 inch green screen; integrated two 320k drives; and retailed originally for about $3,500….ouch! Today, my iPhone 5 is more than 99% lighter, stores 100,000 times more information, and costs a fraction of the price. If you add my iPad, Kindle, Roku video streaming box, my DVR set-top box, my GPS, and other electronic gadgets, it’s hard to imagine how I could have lived a life without these luxuries five years ago.

7. Cards: I analyze numbers, probabilities, and emotions in my day job every day, it’s no wonder that I somehow need to do the same thing in my leisure time. No-Limit Texas Hold ‘Em is the name of the game, and I was introduced to it by world champion “poker brat” Phil Helmuth when he personally taught a group of us at an investment conference in 2003. I haven’t entered the $10,000 World Series of Poker in Las Vegas yet, but it’s on my bucket list.

6. Challenges: I’m a washed up basketball hack after an insignificant high school career and about 12 years of old-man basketball leagues, but my competitive juices keep flowing today. In hopes of not turning to a fully gelatinous blob, I have periodically pushed myself to some competitive athletic challenges, including a hike to the peak of Mt. Whitney; a couple half marathons; a sprint triathlon; a Colorado bike trip; and a few seasons of indoor co-ed soccer. Next up, I’m training for a “century” bike ride – a 100 mile race in early 2013 near Santa Barbara. I guess I better work off some of that stuffing, mash potatoes, and gravy.

5. Good Books: I pretty much read for a living on average 8-12 hours per day, but I suppose I’m a glutton for punishment. Given all my other interests and responsibilities, it’s tough to find the free time to curl up to a good book, but if I can squeeze in a book every quarter, I give myself a pat on the back. Nothing beats true, real-life experiences, but I’ve learned a tremendous amount through all the books I’ve read (for leisure and schooling). Regrettably diversity has gotten the short end of the stick, since about half the books I read are investment related, including a few that I’ve reviewed here on my blog like The Big Short, Too Big to Fail, The Greatest Trade Ever, and Winning the Loser’s Game (to name a few). Currently, I’m reading a fascinating New York Times Bestseller on world religions, called Religious Literacy, which leads me to my next Top 10 item…

4. Spirituality: While I am probably a lot more apathetic and ignorant in the area of religion as compared to the average person, nevertheless I have learned to appreciate the importance and benefits of religion and spirituality through my life experiences. From Judaism to Islam, and Buddhism to Christianity, there is no denying the moral lessons and spiritual balance these religions provide billions of people around the globe. I have a long way to go on my spiritual journey, but I’m slowly learning and progressing. On days where the Dow plummets a few hundred points or when the share price of a top holding tanks, I’m quickly reminded of the importance of spiritual balance.

3. Travel: While many people have hardly ventured from their hometown during their lifetime, I have been blessed with the fortune of seeing many places around the world. Not only have I lived on the East Coast, West Coast, and in the Midwest, but I have also traveled to five different continents. Appreciating different cultures and viewpoints is what truly makes life more interesting for me.

2. Friends: The digital age has not only brought friends closer together through social networks like Facebook (FB) and LinkedIn (LNKD), but has also pushed us further apart because vicariously spying on someone online is much easier than calling someone or grabbing coffee with them. Thankfully, I have a core set of friends that I can share my life’s ups and downs.

1a. Investing: Enough said. I’ve been investing for close to 20 years, and this blog is evidence of the blood, sweat, and tears I’ve dedicated to this endeavor. Various investments will go in and out of favor, and economic cycles will go up and down, but one trend that I know will persist is that I will be investing for the rest of my life.

1b. Health: It goes without saying, but if I don’t have my own good health, then very little on my top 10 list is possible. I’ve outlived two close family members of mine, so needless to say, I am very thankful to be breathing and living.

1c. Family: Having all these great experiences, including al the highs and lows, means absolutely nothing, if you have nobody to share them with. My family means the world to me, and days like Thanksgiving remind me of how lucky I really am.

Although this list was originally scheduled for 10 items, it looks like it has unintentionally expanded to a few more. But how can you blame me? I’ve had some tough times like everyone, but it is virtually impossible to not be thankful for the life I get to live now. Not only do I get to do what I love, but I also get paid to do it.

Last but not least, a special thanks needs to also go out to you, my devoted blog reader. I know you’re devoted, because you have made it to the end of this lengthy article. Without you, I wouldn’t have the motivation to continually scribble down my random thoughts.

Happy Thanksgiving and happy holidays!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AMZN, and AAPL, and a short position in NFLX. At the time of publishing SCM had no direct positions in LNKD, FB, HPQ or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Twinkie Investing – Sweet but Unhealthy

Source: Photobucket

It’s a sad day indeed in our history when the architect of the Twinkies masterpiece cream-filled sponge cakes (Hostess Brands) has been forced to close operations and begin bankruptcy liquidation proceedings. Food snobs may question the nutritional value of the artery-clogging delights, but there is no mistaking the instant pleasure provided to millions of stomachs over the 80+ years of the Twinkies dynasty. Most consumers understand that a healthy version of an organic Twinkie will not be found on the shelves of a local Whole Foods Market (WFM) store anytime soon. The reason people choose to consume these 150-calorie packages of baker bliss is due to the short-term ingestion joy, not the vitamin content (see Nutritional Facts below). Most people agree the sugar high gained from devouring half a box of Twinkies outweighs the long-term nourishing benefits reaped by eating a steamed serving of alfalfa sprouts.

Much like dieting, investing involves the trade-offs between short-term impulses and long-term choices. Unfortunately, the majority of investors choose to react to and consume short-term news stories, very much like the impulse Twinkie gorging, rather than objectively deciphering durable trends that can lead to outsized gains. Day trading and speculating on the headline du jour are often more exciting than investing, but these emotional decisions usually end up being costlier to investors over the long-run. Politically, we face the same challenges as Washington weighs the simple, short-term decisions of kicking the fiscal debt and deficits down the road, versus facing the more demanding, long-term path of dealing with these challenges.

With controversial subjects like the fiscal cliff, entitlement reform, taxation, defense spending, and gay marriage blasting over our airwaves and blanketing newspapers, no wonder individuals are defaulting to reactionary moves. As you can see from the chart below, the desire for a knee jerk investment response has only increased over the last 70 years. The average holding period for equity mutual funds has gone from about 5 years (20% turnover) in the mid 1960s to significantly less than 1 year (> 100% turnover) in the recent decade. Advancements in technology have lowered the damaging costs of transacting, but the increased frequency, coupled with other costs (impact, spread, emotional, etc.), have been shown to be detrimental over time, according to John Bogle at the Vanguard Group.

Source: John Bogle (Vanguard Group)

During volatile periods, like this post-election period, it is always helpful to turn to the advice of sage investors, who have successfully managed through all types of unpredictable periods. Rather than listening to the talking heads on TV and radio, or reading the headline of the day, investors would be better served by following the advice of great long-term investors like these:

“In the short run the market is a voting machine. In the long run it’s a weighing machine.” -Benjamin Graham (Famed value investor)

“Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth.” -Jack Gray (Grantham, Mayo, Van Otterloo)

“The stock market serves as a relocation center at which money is moved from the active to the patient.” – Warren Buffett (Berkshire Hathaway)

“It was never my thinking that made big money for me. It always was my sitting.” – Jesse Livermore (Famed trader)

“The farther you can lengthen your time horizon in the investment process, the better off you will be.”- David Nelson (Legg Mason)

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.” T. Rowe Price (Famed Growth Investor)

“Time arbitrage just means exploiting the fact that most investors…tend to have very short-term time horizons.” -Bill Miller (Famed value investor)

“Long term is not a popular time-horizon for today’s hedge fund short-term mentality. Every wiggle is interpreted as a new secular trend.” -Don Hays (Hays Advisory – Investor/Strategist)

A legendary growth investor who had a major impact on how I shaped my investment philosophy is Peter Lynch. Mr. Lynch averaged a +29% return per year from 1977-1990. If you would have invested $10,000 in his Magellan fund on the first day he took the helm, you would have earned $280,000 by the day he retired 13 years later. Here’s what he has to say on the topic of long-term investing:

“Your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

“My best stocks performed in the 3rd year, 4th year, 5th year, not in the 3rd week or 4th week.”

“The key to making money in stocks is not to get scared out of them.”

“Worrying about the stock market 14 minutes per year is 12 minutes too many.”

It is important to remember that we have been through wars, assassinations, banking crises, currency crises, terrorist attacks, mad-cow disease, swine flu, recessions, and more. Through it all, our country and financial markets most have managed to survive in decent shape. Hostess and its iconic Twinkies brand may be gone for now, but removing these indulgent impulse items from your diet may be as beneficial as eliminating detrimental short-term investing urges.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in WFM, BRKA/B, LM, TROW or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fiscal & Political Chemotherapy

Chemotherapy is a treatment that uses a mixture of toxic drugs designed to destroy cancer cells, so patients can recover to a healthy state. Similarly, our government system combines a mixture of toxic politicians designed to destroy our nation’s problems, so Americans can benefit from a healthy, expanding economy. In the long run, history teaches us that despite painful periods of political battles, beneficial results are eventually achieved.

Unfortunately, in the short run, political side effects relating to our country’s legislative process can result in extremely unpleasant outcomes, just like experienced during chemotherapy treatment (including nausea, vomiting, hair loss, and fatigue). Politically, we are going through a comparably repulsive period. The good news is, regardless of your political persuasion, a major source of contention is now behind us in the rearview mirror (i.e., the presidential elections) and we can temporarily recover from the barrage of venomous super PAC commercials that have temporarily halted.

Regrettably, the looming “Fiscal Cliff” poses larger consequences than election outcomes, if these out-of-control economic issues are not credibly resolved (see Fiscal Cliff: Repeat or Dead Meat?). Most Americans realize a responsible mixture of real spending cuts coupled with limited tax hikes, like proposed by the bipartisan Simpson-Bowles commission is a great starting blueprint to hammer out a deal. For the time being, I’m happy to hear both Republicans and Democrats are playing nicely in the sandbox. Republican Speaker of the House, John Boehner has signaled he is willing “to put (tax) revenue on the table” and President Obama has said he is “open to compromise.” So what’s all the worry then? We already know that $600 billion in tax increases and spending cuts kick in seven weeks from now, which has the real potential of spinning our economy into another recession if Congress doesn’t act.

You don’t need to go far back in history to see what the effects could be from continued gridlock or a lackluster agreement that kicks the can down the curb. For starters, last year’s initially unsuccessful debt ceiling negotiations resulted in a swift kick in the pants for stocks, as investors watched the S&P 500 index crater -18% within three short weeks. If the $600 billion impact of the Fiscal Cliff and sequestration actually occur, many pundits are predicting up to a -4% hit to GDP (Gross Domestic Product), which makes it virtually certain the economy will slip back into recession.

This game of political chicken can last only for so long. Congressional approval ratings are near record lows, and if inaction continues, voters will ultimately take powers into their own hands and vote out apathetic politicians.

Preparing for the Melt-Up

Would I be surprised to see a market pullback in the coming weeks and months? The short answer: NO. While I may be cynical about the short-term probabilities of a bipartisan “grand bargain” because brinksmanship will likely win in the coming weeks, as both sides jockey for negotiating leverage, I am also keenly aware of the melt-up risk that few investors are currently talking about. You don’t have to be a brain surgeon or rocket scientist to see the amount of pessimism that has built up over recent years. If you don’t believe me, you can just look at the following charts to get the gist:

i) A half of a trillion dollars has been pulled out of the equity markets by nervous investors, despite the market more than doubling from its 2009 lows.

Source: Calafia Beach Pundit (Scott Grannis)

ii) Panicked bond buying has caused the yield on the benchmark 10-year Treasury note to evaporate by about -90% since its peak more than 30 years ago.

10-Year Treasury Yield (Source: Yahoo! Finance)

iii) Fear insurance has been gobbled up by worrywarts as witnessed by gold prices sky-rocketing more than 500% in a little more than a decade.

Historical gold prices (Source: InvestmentTools.com)

A grand bargain doesn’t guarantee a return to the stock market circa the 1990s, but in an environment where trillions of dollars have been stuffed under the mattresses of corporations and individuals, earning next to nothing, it won’t take much to ignite the animal spirits of investors. Changing the perception of a market that sees the glass as -90% empty to the view of a glass 10% full, could lead to a happier 2013 for equity investors. However, if no Fiscal Cliff agreement is made, locating me may be a challenge – I suggest you try me in my bunker.

While our fiscal and political health conditions have reached crisis levels in recent years, there are reasons to be optimistic, now that a hotly contested presidential election has concluded and discussions move forward on a Fiscal Cliff solution. Chemotherapy involves a toxic and destructive regiment of harsh medicines, but in certain situations, like the present political environment, investors need to survive the unpleasant side effects before economic health and prosperity can be gained.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Conquering the Political & Economic Hurricanes

Article is an excerpt from previously released Sidoxia Capital Management’s complementary November 1, 2012 newsletter. Subscribe on right side of page.

Hurricane Sandy wreaked havoc across the East Coast, negatively impacting an estimated 60 million people and leaving more than 8 million people literally in the dark, without power. The hurricane may have been downgraded to a “superstorm” but the 90+ mile per hour winds and waves reaching up to 40 feet high created devastating economic impacts. How large were these impacts you may ask? This big swirly cloud that slammed into the Atlantic coastline shut down about ¼ of our economy; led to about 15,000 canceled flights; is expected to cut our nation’s

Q4 output by up to -1.5% in GDP (Gross Domestic Product); and closed our financial markets for two days (the longest weather related closure of the New York Stock Exchange since 1888). Although the damage has been distressing for millions, about 5 million kids I think were okay with missing school on Monday (I’m going out on a limb with that guess).

Besides a superstorm-hurricane offered to us by Mother Nature, our country is about to undergo a new political hurricane next week with our nation’s presidential elections. Many polls show a statistical dead heat among the two candidates (Mitt Romney and Barack Obama), but political pundits point to the key battleground state of Ohio as the key determinant of the overall election results (Obama currently appears to have a slight lead in several polls). Some wildcard issues that could throw a wrench in an incumbent victory include a potential apathetic turnout by the Democratic voter base (hurt worse by “Superstorm Sandy”); worsening employment figures reported four days before the election; or perhaps a political gaffe. None of these polls are set in stone, and the situation remains rather fluid (no Sandy pun intended).

Regardless, whatever the political outcome, history shows us that the victor’s political affiliation has little correlation with the results in the financial markets. Ed Yardeni illustrated this point recently with the following chart:

Source: Yardeni.com

What many people seem to overlook is that there are many other variables besides political affiliation that can and will impact future financial market performance including, Congressional control that may be dominated or split by the opposing political party; monetary policy set by the Federal Reserve Bank; or uncontrollable globalization influences. As emerging market countries continue to outpace our economic growth, our country’s power and persuasion will naturally diminish due to the “law of large numbers”. In other words, as the largest, most powerful economic country in the world, the mathematical gravity hinders our country’s ability to grow rapidly.

Despite the economic and political challenges our country faces, we continue to move in the right direction, albeit at a very slow historical pace. As you can see from Ed Yardeni’s chart below, our recovery from the recent recession (bottom red line) is the worst recovery in more than 50 years. On the bright side, the freshly reported Q3 GDP figures came in at a +2.0% GDP rate – uninspiring, but an improvement from Q2, and better than Wall Street consensus forecasts.

Source: Yardeni.com

The growth has been considerably weak, yet the U.S. has still recorded 13 consecutive quarters of positive growth. Not bad considering Europe is in recession and countries like Spain are Greece are suffering unemployment rates of about 25%.

In order to maintain or accelerate economic growth, most Americans understand the Fiscal Cliff (~$700 billion in automatic spending cuts and tax hikes) needs to get resolved immediately. Failure to face this urgent challenge could have dire consequences, so voting for politicians who understand the immediacy of this problem is important.

Moving into Seasonally Strong Period

Selling in May, and going away for six months has not been a profitable strategy this year, as measured by the S&P 500 index. Furthermore, investors have also survived the historically scary performance months of September and October. Nothing is ever guaranteed, but historically the months of November through April tend to be rewarding periods.

Blowing against this positive seasonal trend have been lifeless earnings. In fact, corporate profits and revenue growth have slowed to a trickle in Q3, thanks to lackluster results from companies like Caterpillar (CAT); General Electric (GE); 3M Company (MMM); United Technologies (UTX); McDonalds (MCD); and others. Denying the global slowdown is difficult, but there are signs of stabilization and fortunately financial markets look forward and not backward.

Overshadowing some of that recent slowing growth has been the positive development in the housing market. As one can see in the chart below, housing starts are up significantly at +60% from early last year, but history tells us there is still plenty of room to move higher.

Source: Calafia Beach Report

Year-to-date stock performance has been nothing short of spectacular either. Although stocks were down about -2% in October, the S&P 500 index remains up +12% through October, and that excludes about +2% in dividends. If you look at the overall asset classes in the chart below, real estate is the winning segment this year with U.S. stocks not far behind. Commodities have fared the worst and the fixed income asset class showed modest gains relative to global equities.

Source: Hays Advisory Blog

Within U.S. stocks, the largest of large stocks (“Megacaps”) have enjoyed the best results. This trend is not surprising given the significant uncertainties investors are reviewing (e.g., elections, Fiscal Cliff, Europe, etc.).

Source: Calafia Beach Report

The recent Hurricane Sandy turned superstorm caused enormous damage to our country, and the political and economic hurricanes we have experienced over the last few years have yet to be conquered. The good news, in all these cases (physical and financial), is that the clouds are in the process of lifting; the worst damage should be behind us; our outlook will be more certain; and we can now begin focusing on the rebuilding process.

Like Washington, individual investors cannot afford to ignore their own personal Fiscal Cliffs. In a future entitlement-pressured world, investors need to proactively develop an investment plan, because ignoring your investments by kicking the can down the road only does more harm than good. I’m confident that, regardless of the election results next week, cooler heads will eventually prevail, and Democrats and Republicans can work together to solve our country’s Fiscal Cliff problems. Superstorm Sandy will not be the last natural disaster our country faces, but like investing, the more prepared one is for these unforeseen events, the better you will be equipped to conquer your financial future.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in CAT, MMM, GE, UTX, MCD, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chewing on Some Apple Pie

Apple pie is an unrivaled American dessert that optimally mixes the elements of dough, sugar, cinnamon, and apples. With Thanksgiving just around the corner, I can already taste that Costco (COST) apple pie that is about to snap my belt buckle open as I proceed to eat pie for breakfast, lunch, and dinner. A different dessert of the stock variety, Apple Inc. (AAPL), recently received a sour reception after reporting its 3rd quarter financial results.

Despite reporting +27% year-over-year revenue growth and +23% earnings growth, investors have continued to spew the stock out as the share price has fallen from $700 per share down to $600 per share in about a month. With all this indigestion, is now the time to reach for the Tums or should we serve ourselves up another helping of some tasty Apple pie? Not everybody loves this particular fruity dessert, so let’s cut into the Apple pie stock and see if there is any dough to be made here.

Point #1 (Cash Giant): Apple Inc. is a profit machine with a fortress balance sheet. More specifically, Apple has around $121 billion dollars in cash in its checking account and generated over $42 billion in free cash flow in fiscal 2012. And by free cash flow, I mean the excess cash Apple gets to stuff in its pockets after ALL expenses have been paid AND after spending more than $8 billion in capital expenditures (including spending for their new 2.8 million sq. foot spaceship campus expected to open in 2015 and house 13,000 employees).

Point #2: (Brand): A brand has value that will not show up on a balance sheet, and according to Forbes, Apple’s brand is rated #1 on a global basis, outstripping iconic brands like IBM, McDonald’s (MCD) and Microsoft (MSFT). BrandZ, a division of advertising giant WPP, values Apple’s 2012 brand value at approximately $183 billion.

Point #3 (Product Pipeline): Apple is no one-trick pony. Apple’s iPhone sales account for about half of the company’s sales, but a whole new slate of products positions them well for the critical calendar fourth quarter period. Apple’s iPhone 5, iPad 3 (aka, “New iPad”), and iPad Mini should translate into robust holiday sales for Apple. What’s more, a +39% increase in Apple’s fiscal 2012 R&D (research and development) should mean a continued healthy pipeline of new products, including the ever-rumored new integrated version of Apple TV that could be coming in 2013.

Point #4 (Mobile & Tablets): Apple is at the center of the mobile revolution. There are approximately 5 billion cell phones globally, and about 2 billion new phones are sold each year. Of that 2 billion, Apple sold a paltry 125 million units (tongue firmly in cheek) with the market growing faster in Apple iPhone’s key smart phone market. As the approximately 500 million smart phone market grows to about 5 billion units over the next decade, Apple is uniquely positioned to capitalize on this trend. Beyond cell phones, the table market is bursting as traditional personal computer growth declines. Although Apple has made computers for 36 years, the company impressively generated +40% more revenue from fiscal 2012 iPad tablet sales, relative to Apple desktop and laptop sales.

Point #5 (Valuation): With all these positives, what type of premium would you pay for Apple’s stock? Does a +100% premium sound reasonable? OK, maybe a tad high, so how about a +50% premium? Alright, alright, I know you want a good bargain, so surely a +20% premium is warranted? Well in fact, if you account for Apple’s $121 billion cash hoard, Apple’s stock is currently trading at about a -22% DISCOUNT to the average S&P 500 stock on a P/E basis (Price-Earnings). You heard that correctly, a significant discount. If Apple is trading at a P/E discount, surely mature staple stocks like Procter & Gamble (PG) and Colgate Palmolive (CL), which both reported negative Q3 revenue declines coupled with meager bottom-line growth of 5%, deserve even steeper discounts…right? WRONG. These stocks trade at a 70-80% PREMIUM to Apple and a 35-40% PREMIUM to the overall market. Toilet paper and toothpaste I guess are a lot more popular than consumer electronics these days. Clear as mud to me.

Risks: I understand that Apple is not a risk-free Treasury security. Research in Motion’s (RIMM) rapid collapse over the last two years serves as a fresh reminder that in technology land, competition and obsolescence risks play a much larger role compared to other industries. Apple must still deliver on its product visions, and as the king of the hill Apple will have a big bulls-eye on its back from both competitors and regulators. Hence, we will continue to read overblown headlines about map application glitches and photographic purple haze.

In the end, a significant amount of pessimism is already built into Apple’s stock price (yes, I did say “pessimism” – even with the stock’s share price up +49% this year). If Apple can uphold the quality of its products and maintain modest growth, then I’m confident shareholders will happily eat another slice of Apple pie.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct positions in COST, IBM, MCD, CL, PG, MSFT, WPP, RIMM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

USA Inc.: Buy, Hold or Sell?

If the U.S. was a company, would you buy, hold, or sell the stock? A voluminous report put out last year by Mary Meeker sought to answer that very question. Since we’re in the thick of the presidential elections, why not review the important financial state of our great nation.

For those of you who may not know who she is, Mary Meeker is the well-known partner at Kleiner Perkins Caufield & Byers, who is also affectionately known as the “Queen of Internet.” Apparently, beyond her renowned expertise in analyzing and valuing tech companies and start-ups, she also has the knack of dissecting government statistics and distilling wonky numbers down to understandable terms for the masses. “Distilling” may be a generous term, given the massive size of her 460-page report, USA Inc., but nevertheless, I am going to attempt to synthesize this gargantuan report even further.

As a visual learner, I think some key cherry-picked slides from her report will help put our multi-trillion debts and deficits in context, so here goes…

The Scope of the Problem

If one spends a few hundred billion dollars here, and a few hundred billion dollars there, before you know it, a trillion dollars will have piled up. Currently our government has run $1 trillion+ budget deficits for three years, and the estimated deficit is for another trillion dollar deficit this fiscal year. If you have ever wondered how many football fields it takes to fill with a trillion dollars of cash, then today is your lucky day. The answer: 217 football fields.

Financial Statements: The Health Thermometer

In order to determine the relative health of USA Inc., Meeker created financial statements for our country, starting with the income statement. As you can see from the chart below, unfortunately USA Inc.’s expenses have been significantly larger than its revenues, creating a “discouraging” trend of negative cash flows (deficits). An entity that takes in $2.2 trillion in revenue and spends $3.5 trillion, cannot sustainably continue this trend for long, before significant financial problems arise. The largest contributing factor to our country’s losses (deficits) has been the exploding costs of entitlements, including Medicare, Medicaid, and Social Security.

As the pie chart shows, the major categories of entitlements comprise a whopping 58% of USA Inc.’s 2010 total expenditures.

Trillion dollar deficits have been the norm over the last three years.

Why Entitlement Spending is a Problem

Why are entitlements such a massive problem? The plain and simple answer to why entitlements are a major issue is that government expenditures are growing too fast. You can’t have expenses growing significantly faster than revenues for 45 years and expect to be in happy financial place.

Another reason for the abysmal spending record is due to politicians horrendous forecasting abilities. Future promises are made by politicians to garner votes today, and when they make overly rosy estimates about the costs of those promises, future generations are left holding the underfunded bag. Meeker points out that when Medicare was instituted in 1966, total future spending of $110 billion turned out to be about 10x more expensive (see chart below) than originally planned…ouch!

No Defense for Defense

Trillion dollar deficits and debts can’t be solely blamed on entitlements, but $700 billion in annual defense expenditures is not exactly chump change. The inopportune timing of the financial crisis in 2008-2009 didn’t help either, while two unfunded wars were being fought. Even if you strip out the wars, defense spending is still obscenely high. Given our poor state of financial affairs, we cannot afford to be the globe’s babysitter (see Impoverished Global Babysitter). Legacy Cold War spending on obsolete ground warfare needs to be reprioritized to 21st Century threats (i.e. focus on unmanned drones and coordinated intelligence). When a government spends more than the top 25 countries combined (see chart below), that country can certainly find some defense fat to trim.

Demographic Headwinds

The out-of-control gluttonous government spending is a threat to our national security, and although I wish I could say time alone will heal our fiscal wounds, unfortunately the opposite is true. Time is our enemy because the ticking demographic time bomb is about to explode, unless government acts to solve our spending problems. For starters, Americans are living longer, which means entitlement spending has accelerated faster than revenues collected, and life expectancy consistently continues to rise. As you can see below, life expectancy has outpaced Social Security age adjustments by +23% over a 74 year period.

Another self inflicted problem contributing to our colossal health care costs is the obesity epidemic. Over an 18 year period, the rate of obesity more than doubled to 32%. Individuals can and should shoulder more of the burden for these belt-busting costs, and government should spend more on prevention and education in this area. Bad drivers pay higher premiums for their auto insurance, so why not have bad eaters pay higher premiums? Genetics certainly can play a role in obesity, but so to do eating habits. The same accountability principle should be applied to smokers who overly burden our healthcare system too.

The USA spends more on healthcare than all OECD countries combined and 3x the OECD per capita average, yet as you can see from the chart below, the USA is not getting a life expectancy bang for its buck. The argument that the U.S. has the best healthcare in the world may be true in some instances, but the overall data doesn’t support that assertion.

The Rubber Hits the Road

The problem is easy to identify: Government spending going out the door is running faster than the revenues coming in via taxes. The solution is easy to identify too: Politicians need to cut spending, increase taxes, and/or do a combination of the two options. Like dieting, the solutions are easy to identify but difficult to execute.

Source: Calafia Beach Pundit – Scott Grannis

Almost everyone wants the government to spend less, but at the same time nobody wants their benefits cut. You can’t have your cake and eat it too. Citing two different studies, Meeker shows how 80% of Americans want a balanced budget as a national priority, but only 12% are willing to cut spending on Medicare and Social Security.

The rubber will hit the road in the next few months when politicians in a post-presidential election period will be forced to face these difficult “Fiscal Cliff” choices – $700 billion+ in tax hikes and spending increases that jeopardize the current recovery and our fiscal future.

Source: PIMCO

As market maven Mary Meeker recognizes, our fiscal situation is quite “discouraging”. With that said, although USA Inc. may have earned a current “Sell” rating, Meeker acknowledges that our country can become a positive turnaround situation. If voters actively push politicians to making difficult but necessary financial decisions to lower deficits and debt, investors around the globe will be ready to “Buy” USA Inc.’s stock.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Google Caught Naked: Their Loss, Your Gain?

Google Inc. (GOOG) got caught naked yesterday with the early release of its lackluster numbers and “Pending Larry Quote,” but is Google’s loss your gain? An endless number of bloggers and media outlets were quick to jump on the bandwagon, highlighting the sophomor-ish early dissemination of quarterly results, and then simultaneously headlines were blasted about a -20% drop in profits.

I love these sensationalist headlines that I hear chirped in the local Starbucks (SBUX), on the elevator, or at the grocery store. The Armageddon headlines and cascading minute-by-minute charts make for entertaining viewing, but the gaudy $40 billion in cash piling up on Google’s balance sheet, including the measly $3 billion it added in the quarter, may also be news-worthy. Fear sells more than greed, which may explain why there is little mention of Google’s +45% revenue growth (equally misleading because of the Motorola deal). Let me remind you, the $3 billion of cold hard cash created in a single 90 day period is the equivalent size of many large established companies – companies like Groupon Inc. (GRPN), Tesla Motors Inc. (TSLA), and Weight Watchers International Inc. (WTW).

If people could take off their panic caps for a minute, they would be able to see the explosion in smart phones (now around 1 billion) is on pace to swell to 5 billion over the next decade. What will that mean for a market leader like Google with over ½ billion Android devices that is activating 1.3 million more every day? I don’t know for sure, but I’m willing to venture it is going to mean a lot of dough for Google. What further inspires my confidence? Well, the fact that Google’s mobile related revenues have gone from $2.5 billion run rate last year to over $8 billion today indicates they are on the right track.

Google got caught naked with its press release flub, and the frail Motorola acquisition may cause a little indigestion in the coming quarters, but any short-run Google losses may be your opportunity for long-term gains.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and GOOG, but at the time of publishing SCM had no direct positions in SBUX, TSLA, GRPN, WTW, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}