Monitoring the Tricks Hidden Up Corporate Sleeves

As Warren Buffett correctly states, “If you are in a poker game and after 20 minutes, you don’t know who the patsy is, then you are the patsy.” The same principle applies to investing and financial analysis. If you are unable to determine who is cooking (or warming) the books via deceptive practices, then you will be left holding a bag of losses as tears of regret pour down your face. The name of the stock investing game (not speculation game) is to accurately gauge the financial condition of a company and then to correctly forecast the trajectory of future earnings and cash flows.

Unfortunately for investors, many companies work quite diligently to obscure, hide, and distort the accuracy of their current financial condition. Without the ability of making a proper assessment of a company’s financials, an investor by definition will be unable to value stocks.

There are scores of accounting tricks that companies hide up their sleeves to mislead investors. Many people consider GAAP (Generally Accepted Accounting Principles) as the laws or rules governing financial reporting, but GAAP parameters actually provide companies with extensive latitude in the way accounting reports are implemented. Here are a few of the ways companies exercise their wiggle room in disclosing financial results:

Depreciation Schedules: Related to GAAP accounting, adjustments to longevity estimates by a company’s management team can tremendously impact a company’s reported earnings. For example, if a $10 million manufacturing plant is expected to last 10 years, then the depreciation expense should be $1 million per year ($10m ÷ 10 years). If for some reason the Chief Financial Officer (CFO) suddenly changes his/her mind and decides the building should last 40 years rather than 10 years, then the company’s annual expense would miraculously decrease -75% to $250,000. Voila, an instant $750,000 annual gain created out of thin air! Other depreciation tricks include the choice of accelerated or straight-line depreciation.

Capitalizing Expenses: If you were a management team member with a goal of maximizing current reported profitability, would you be excited to learn that you are not required to report expenses on your income statement? For many the answer is absolutely “yes”. A common example of this phenomenon occurs with companies in the software industry (or other companies with heavy research and development), where research expenses normally recognized on the income statement get converted instead to capitalized assets on the balance sheet. Eventually these capitalized assets get amortized (recognized as expenses) on the income statement. Proponents argue capitalizing expenses better matches future revenues to future expenses, but regardless, this scheme boosts current reported earnings, and delays expense recognition.

Stuffing the Channel: No, this is not a personal problem, but rather occurs when companies force their goods on a distributor or customer – even if the goods (or service) are not requested. This deceitful practice is performed to drive up short-term revenue, even if the reporting company receives no cash for the “stuffing”. Ballooning receivables and substandard cash flow generation can be a sign of this cunning, corporate custom.

Accounts Receivable/Loans: Ballooning receivables is a potential sign of juiced reported revenues and profits, but there are more nuanced ways of manipulating income. For instance, if management temporarily lowers warranty expenses and product return assumptions, short-term profits can be artificially boosted. In addition, when discussing financial figures for banks, loans can also be considered receivables. As we experienced in the last financial crisis, many banks under-provisioned for future bad loans (i.e. didn’t create enough cash reserves for misled/deadbeat borrowers), thereby overstating the true, underlying, fundamental earnings power of the banks.

Inventories: As it relates to inventories, GAAP accounting allows for FIFO (First-In, First-Out) or LIFO (Last-In, Last-Out) recognition of expenses. Depending on whether prices of inventories are rising or falling, the choice of accounting method could boost reported results.

Pension Assumptions: Most companies like their employees…but not the expenses they have to pay in order to keep them. Employee expenses can become excessively burdensome, especially for those companies offering their employees a defined benefit pension plan. GAAP rules mandate employers to contribute cash to the pension plan (i.e., retirement fund) if the returns earned on the assets (i.e., stocks & bonds) are below previous company assumptions. One temporary fix to an underfunded pension is for companies to assume higher plan returns in the future. For example, if companies raise their return assumptions on plan assets from 5% to a higher rate of 10%, then profits for the company are likely to rise, all else equal.

Non-GAAP (or Pro Forma): Why would companies report Non-GAAP numbers on their financial reports rather than GAAP earnings? The simple answer is that Non-GAAP numbers appear cosmetically higher than GAAP figures, and therefore preferred by companies for investor dissemination purposes.

Merger Magic: Typically when a merger or acquisition takes place, the acquiring company announces a bunch of one-time expenses that they want investors to ignore. Since there are so many moving pieces in a merger, that means there is also more opportunities to use smoke and mirrors. The recent $8.8 billion write-off of Hewlett-Packard’s (HPQ) acquisition of Autonomy is evidence of merger magic performed.

EBITDA (Earnings Before Interest Taxes Depreciation & Amortization): Skeptics, like myself, call this metric “earnings before all expenses.” Or as Charlie Munger says, Warren Buffett’s right-hand man, “Every time you see the word EBITDA, substitute it with the words ‘bulls*it earnings’!”

This is only a short-list of corporate accounting gimmicks used to distort financial results, so for the sake of your investment portfolio, please check for any potential tricks up a company’s sleeve before making an investment.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HPQ/Autonomy, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Beware: El-Erian & Gross Selling Buicks…Not Chevys

As my grandmother always told me, “Be careful where you get your advice!” Or as renowned Wall Street trader Gerald Loeb once said, “The Buick salesman is not going to tell you a Chevrolet will fit your needs.” In other words, when it comes to investment advice, it is important to realize that opinions and recommendations are often biased and steeped with inherent conflicts of interest. Having worked in the financial industry over several decades, I have effectively seen it all.

However, one unique aspect I have grown accustomed to is the nauseating and fatiguing over-exposure of PIMCO’s dynamic bond duo, CEO Mohamed El-Erian and founder Bill Gross. Over the last four years and 13 consecutive quarters of GDP growth (likely 14 after Q4 revisions), I and fellow CNBC viewers have been forced to endure the incessant talk of the “New Normal” of weak economic growth to infinity. Actual results have turned out quite differently than the duet’s cryptic and verbose predictions, which have piled up over their seemingly non-stop media interview schedule. Despite the doomsday rhetoric from the bond brothers, El-Erian and Gross have witnessed a more than doubling in equity prices, which has soundly trounced the performance of bonds over the last four years.

After being mistaken for such a long period, certainly the PIMCO marketing machine would revise their pessimistic outlook, right? Wrong. In true biased fashion, El-Erian cannot admit defeat. Just this week, El-Erian argues stocks are artificially high due to excessive liquidity pumped into the financial system by central banks (see video below). I’m the first one to admit Federal Reserve Chairman Ben Bernanke is explicitly doing his best to force investors into risky assets, but doesn’t generational low interest rates help bond prices too? Apparently that mathematical fact has escaped El-Erian’s bond script.

Source: Yahoo! Finance (Daily Ticker)

El-Erian’s buddy, Bill Gross, can’t help himself from jumping on the stock rain parade either. Just six weeks ago Gross followed the bond-pumping playbook by making another dour prediction that the market would rise less than 5% in 2013. Unfortunately for Gross, his crystal ball has also been a little cloudy of late, with the S&P 500 index already up more than +6.5% this year. Since doomsday outlooks are what keeps the $2 trillion PIMCO machined primed, it’s no surprise we hear about the never-ending gloom. For those keeping score at home, let’s please not forget Bill Gross’s infamously wrong Dow 5,000 prediction (see article).

PIMCO Smoke & Mirrors: Stock Funds with NO Stocks

Just when I thought I had seen it all, I came across PIMCO’s Equity-Related funds. Never in my career have I seen “equity” mutual funds that invest solely in “bonds.” Well, apparently PIMCO has somehow creatively figured out how to create stock funds without investing in stocks. I guess that is one strategy for a bond-centric company of getting into the equity fund market? This is either ingenious or bordering on the line of criminal. I fall into the latter camp. How the SEC allows the world’s largest bond company to deceivingly market billions in bond-filled stock funds to individual investors is beyond me. After innocent people got fleeced by unscrupulous mortgage brokers and greedy lenders, in this Dodd-Frank day and age, I can’t help but wonder how PIMCO is able to solicit a StockPlus Fund that has 0% invested in common stocks. You can judge for yourself by reviewing their equity-related funds on their website (see also chart below):

PIMCO Equity-Related Funds with No Equity

PIMCO Active Equity Funds Struggle

With more than 99% of PIMCO’s $2 trillion in assets under management locked into bonds, company executives have made a half-hearted effort of getting into the equity markets, even though they’ve enjoyed high-fiving each other during the three-decade-long bond bull market (see Downhill Marathon Machine). In hopes of diversifying their bond-heavy revenue stream, in 2009 they hired the head of the high-profile $700 billion, government TARP program (Neil Kashkari). Subsequently, PIMCO opened its first set of actively managed funds in 2010. Regrettably for PIMCO, the sledding has been quite tough. In 2012, all six actively managed equity funds lagged their benchmarks. Moreover, just a few weeks ago, Kashkari their rock star hire decided to quit and pursue a return to politics.

Mohamed El-Erian and Bill Gross have never been camera shy or bashful about bashing stocks. PIMCO has virtually all their bond eggs in one basket and their leaderless equity division is struggling. What’s more, like some car salesmen, they have had a creative way of describing the facts. If it’s a Chevy or unbiased advice you’re looking for, I recommend you steer clear from Buick salesmen and PIMCO headquarters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in PIMCO funds, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Vice Tightens for Those Who Missed the Pre-Party

The stock market pre-party has come to an end. Yes, this is the part of the bash in which an exclusive group is invited to enjoy the fruits of the festivities before the mobs arrive. That’s right, unabated access to the nachos; no lines to the bathroom; and direct access to the keg. For those of us who were invited to the stock market pre-party (or crashed it on their own volition), the spoils have been quite enjoyable – about a +128% rebound for the S&P 500 index from the bottom of 2009, and a +147% increase in the NASDAQ Composite index over the same period (excluding dividends paid on both indexes).

Although readers of Investing Caffeine have received a personal invitation to the stock market pre-party since I launched my blog in early 2009, many have shied away, out of fear the financial market cops may come and break-up the party.

Rather than partake in stock celebration over the last four years, many have chosen to go down the street to the bond market party. Unlike the stock market party, the fixed-income fiesta has been a “major-rager” for more than three decades. However, there are a few signs that this party has gotten out-of-control. For example, crowds of investors are lined up waiting to squeeze their way into some bond indulgence; after endless noise, neighbors are complaining and the cops are on their way to shut the party down; and PIMCO’s Bill Gross has just jumped off the roof to do a cannon-ball into the pool.

Even though the stock-market pre-party has been a blast, stock prices are still relatively cheap based on historical valuation measurements, meaning there is still plenty of time for the party to roll on. How do we know the party has just started? After five years and about a half a trillion dollars hemorrhaging out of domestic funds (see Calafia Beach Pundit), there are encouraging signs that a significant number of party-goers are beginning to arrive to the party. More specifically, as it relates to stocks, a fresh $10 billion has flowed into domestic equity mutual funds during this January (see ICI chart below). This data is notoriously volatile, and can change dramatically from month-to-month, but if this month’s activity is any indication of a changing mood, then you better hurry to the stock party before the bouncer stops letting people in.

Source: Investment Company Institute (ICI)

Vice Begins to Tighten on Party Outsiders

Many stock market outsiders have either been squeezed into the bond market, hidden in cash, or hunkered down in a bunker with piles of gold. While some of these asset classes have done okay since early 2009, all have underperformed stocks, but none have performed worse than cash. For those doubters sitting on the equity market sidelines, the pain of the vice squeezing their portfolios has only intensified, especially as the economy and employment picture slowly improves (see chart below) and stock prices persist directionally upward. For years, fear-mongering stock skeptics have warned of an imploding dollar, exploding inflation, a run-away deficit/debt, a reckless money-printing Federal Reserve, and political gridlock. Nevertheless, none of these issues have been able to kill this equity bull market.

Source: Calafia Beach Pundit

But for those willing and able investors to enter the stock party today, one must realize this party will only get riskier over time. As we exit the pre-party and enter into the main event, you never know who may join the party, including some uninvited guests who may steal money, get sick on the carpet, participate in illegal activities, and/or ruin the fun by clashing with guests. We have already been forced to deal with some of these uninvited guests in recent years, including the “flash crash,” debt ceiling debate, European financial crisis, fiscal cliff, and lastly, sequestration is about to arrive as well (right after parking his car).

New investors can still objectively join the current equity party, but it is necessary to still be cognizant of not over-staying your welcome. However, for those party-pooping doubters who already missed the pre-party, the vice will continue to tighten, leaving stock cynics paralyzed as they watch additional missed opportunities enjoyed by the rest of us.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Debuts Video & Goes to the Movies

Article is an excerpt from previously released Sidoxia Capital Management’s complementary February 1, 2013 newsletter. Subscribe on right side of page.

The red carpet was rolled out for the stock market in January with the Dow Jones Industrial Average rising +5.8% and the S&P 500 index up an equally impressive +5.0% (a little higher rate than the 0.0001% being earned in bank accounts). Movie stars are also strutting their stuff down the red carpet this time of the year as they collect shiny statues at ritzy award shows like the Golden Globes and Oscars. Given the vast volumes of honors bestowed, we thought what better time to put on our tuxes and create our own 2013 nominations for the economy and financial markets. If you are unhappy with our selections, you are welcome to cast your own votes in the comments section below.

By award category, here are Sidoxia’s 2013 selections:

Best Drama (Government Shutdown & Debt Ceiling): Washington D.C. has provided no shortage of drama, and the upcoming blockbusters of Shutdown & Debt Ceiling are worthy of its Best Drama nomination. If Congressional Democrats and Republicans don’t vote in favor of a new “Continuing Resolution” by March 27th, then our United States government will come to a grinding halt. At issue is Republican’s desire for additional government spending cuts to lower our deficit, which is likely to exceed $1 trillion for the fifth consecutive year. If you like more heart pumping drama, the Senate has just passed a Debt Ceiling extension through May 18th…mark those calendars!

Best Horror Film (Sequestration): Most people have already seen the scary prequel, The Fiscal Cliff, but the sequel Sequestration deserves the horror film honors of 2013. This upcoming blood-filled movie about broad, automatic, across-the-board government cost cuts will make any casual movie-watcher scream in terror. The $1.2 trillion in spending cuts (over 10 years) are so gory, many viewers may voluntarily leave the theater early. If you are waiting for the release, Sequestration is coming to a theater near you on March 1st, unless Congress, in an unlikely scenario, cancels the launch.

Best Director (Ben Bernanke): Federal Reserve Chairman Ben Bernanke’s film, entitled, The U.S. Economy, had a massive budget of about $16 trillion dollars, based on estimates of last year’s GDP (Gross Domestic Product). Nevertheless, Bernanke managed to do whatever it took (including trillions of dollars in bond buying) to prevent the economic movie studio from collapsing into bankruptcy. While many movie-goers were critical of his directorial debut, inflation has remained subdued thus far, and he has promised to continue his stimulative monetary policies (i.e., keep interest rates low) until the national unemployment rate falls below 6.5% or inflation rises above 2.5%.

Best Foreign Film (China): Americans are not the only people who produce movies globally. A certain country with a population of nearly 1.4 billion people also makes movies too…China. In the most recently completed 4th quarter, China’s economy experienced blockbuster growth in the form of +7.9% GDP expansion. This was the fastest pace achieved by China in two whole years. To put this metric into perspective, compare China’s heroic growth to the bomb created by the U.S. economy, which registered a disappointing -0.1% contraction at the economic box office. China’s popularity should bring in business all around the globe.

Best Special Effects (Japan): After coming out with a series of continuous flops, Japan recently launched some fresh new special effects in the form of a $116 billion emergency stimulus package. The country also has plans to superficially enhance the visual portrayal of its economy by implementing its own faux money-printing program modeled after our country’s quantitative easing actions (i.e., the Federal Reserve stimulus). As a result of these initiatives, the Japanese Nikkei index – their equivalent of our Dow Jones Industrial index – has risen by +29% in less than 3 months to a level of 11,138.66 (click here for chart). But don’t get too excited. This same Nikkei index peaked at 38,957 in 1989, a far cry from its current level.

Best Action Film (Icahn vs. Ackman): This surprisingly entertaining action film features a senile 76-year-old corporate raider and a white-haired, 46-year-old Harvard grad. The investment foes I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. In addition to terms such as crybaby, loser, and liar, the 27-minute verbal spat (view more here) between Icahn (his net worth equal to about $15 billion) and Ackman (net worth approaching $1 billion) includes some NC-17 profanity. The clash of these investment titans stems from a decade-old lawsuit, in addition to a recent disagreement over a controversial short position in Herbalife Ltd. (HLF), a nutritional multi-level marketing firm.

Best Documentary (Europe): As with a lot of reality-based films, many don’t receive a lot of attention. So too has been the commentary regarding the eurozone, which has been relatively peaceful compared to last spring. Despite the comparative media silence, European unemployment reached a new high of 11.8% late last year. This European documentary is not one you should ignore. European Central Bank (ECB) President Mario Draghi just stated, “The risks surrounding the outlook for the euro area remain on the downside.”

Best Original Song (National Anthem): We won’t read anything politically into Beyonce’s lip-synced rendition of The Star-Spangled Banner at the presidential inauguration, but she is still worthy of the Sidoxia nomination because music we hear in the movies is also recorded. I’m certain her rapping husband Jay-Z agrees whole-heartedly with this viewpoint.

Best Motion Picture (Sidoxia Video): It may only be three minutes long, but as my grandmother told me, “Great things come in small packages.” I may be a little biased, but judge for yourself by watching Sidoxia’s Oscar-worthy motion picture debut:

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Herbalife Strife: Icahn & Ackman Duke It Out

I have seen a lot of things in my two decades in the investment industry, but seeing a verbal cage fight between a senile 76 year-old corporate raider and a white-haired, 46 year-old Harvard grad makes for surprisingly entertaining viewing. The investment heavyweights I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. If getting a few billionaires yelling at each other on live TV is not enough to interest you, then how about adding some tongue-laced f-bombs coupled with blow-by-blow screaming from background traders?

What’s the source of the venomous, spitting hatred between these stock market tycoons? In short, it can be boiled down to a decade old lawsuit (profitable for both I might add), and a disagreement over the short position of a controversial stock, Herbalife (HLF). Regarding the legal spat, in 2003 the SEC was investigating Ackman while his Gotham Partners hedge fund was collapsing, so Ackman asked Icahn to buy shares of Hallwood Realty in hopes of salvaging his fund. Eventually, Icahn bought shares, but a difference in opinion over the transaction led to a lawsuit that Icahn lost, thereby forcing him to pay Ackman $9 million.

Icahn also had a beef with Ackman’s handling of Herbalife: Parading in front of hundreds of investors to self-indulgently create a bear raid on an unsuspecting company is poor form in Icahn’s view, and Carl wanted to make sure Ackman was aware of this investing faux pas.

Normally, investing reporting over cable television is rather mundane, unless you consider entertainers like Jim Cramer yelling “booyah” amusing (see also my article on Mr. Booyah)? On the other hand, if you enjoy billionaires embracing the spirit of the Jerry Springer Show by screaming purple-faced profanities, then you should check out the CNBC cage fight here in its entirety:

If you lack time in your busy schedule to soak in the full bloody battle, then here is a synopsis of my favorite highlights:

Icahn on Ackman the “Crybaby”: “I really sort of have had it with this guy Ackman….I get a call from this Ackman guy. I’m telling you, he’s like the crybaby in the schoolyard. I went to a tough school in Queens. They used to beat up the little Jewish boys. He was like a little Jewish boy crying that the world was taking advantage of him.”

Ackman Referring to Icahn as a “Bully” and Himself as “Roadkill on the Hedge Fund Highway”: “Why did he [Icahn] threaten to sue me? He was a bully. Okay? I was not in a good place in my business career. I was under investigation by Spitzer, winding down my fund. There was negative press about Gotham Partners. I was short MBIA (MBI). They were aggressively attacking me and Carl Icahn thought this guy [Ackman] is roadkill on the hedge fund highway… This is not an honest guy [Icahn] who keeps his word. This is a guy who takes advantage of little people.”

Agitated Icahn Tearing a New One for Scott Wapner (CNBC Commentator): “I didn’t get on to be bullied by you [Wapner]… I’m going to talk about what I want to talk about. Okay? If you want to take that position, I will never go on CNBC. You can say what the hell you want. I’m going to talk about what Ackman just said about me, not about Herbalife. I’ll talk about Herbalife when I want to, not when you ask me. I’m never going on a show with you again, that’s for damn sure. Let’s start with what I want to say. Ackman is a liar.”

Icahn on Another Ackman Rampage: “I will tell you something. As far as I’m concerned, he wanted to have dinner with me and I laughed. I couldn’t figure out if he was the most sanctimonious guy or the most arrogant… the guy takes inordinate risk…I don’t have an investment with Ackman. I wouldn’t have one if you paid me, if Ackman paid me to do it… I made a huge mistake getting involved with him…After he won [the lawsuit], he planted some article in the New York Times pounding his chest telling the world how great he was. You know, as far as I’m concerned the guy is a major loser.”

New CNBC Revenue Stream?

There hasn’t been this much fireworks since Professor Jeremy Siegel took Bill Gross to task on the Pimco Boss’s assessment that the “cult of equity is dying” last July. In retrospect, that minor tiff was child’s play relative to the Icahn vs. Ackman battle. With CNBC viewership down from pre-crisis levels, the network may strongly consider instituting a new pay-per-view revenue stream dedicated to battles between opposing investment enemies. I will even offer up my services to verbally smack down some of the enemies I’ve written about previously. If my phones don’t ring, then I can always offer up my American Investment Idol concept in which I can play Simon Cowell.

This may or may not be the last round of the Carl Icahn and Bill Ackman fight, but the ultimate bragging rights may depend on the ultimate outcome of Ackman’s Herbalife short. If Icahn makes a tender offer for Herbalife, I will anxiously wait for CNBC’s Scott Wapner to invite Carl back on the show. I can hardly wait…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, MBI, NYT, Hallwood Realty, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Risk of “Double-Rip” on the Rise

Okay, you heard it here first. I’m officially anointing my first new 2013 economic term of the year: “Double-Rip!” No, the biggest risk of 2013 is not a “double-dip” (the risk of the economy falling back into recession), but instead, the larger risk is of a double-rip – a sustained expansion of GDP after multiple quarters of recovery. I know, this sounds like heresy, given we’ve had to listen to perma-bears like Nouriel Roubini, Peter Schiff, John Mauldin, Mohamed El-Erian, Bill Gross, et al shovel their consistently wrong pessimism for the last 14 quarters. However, those readers who have followed me for the last four years of this bull market know where I’ve stood relative to these unwavering doomsday-ers. Rather than endlessly rehash the erroneous gospel spewed by this cautious clan, you can decide for yourself how accurate they’ve been by reviewing the links below and named links above:

Roubini calling for double-dip in 2012

Roubini calling for double-dip in 2011

Roubini calling for double-dip in 2010

Roubini calling for double-dip in 2009

If we switch from past to present, Bill Gross has already dug himself into a deep hole just two weeks into the year by tweeting equity markets will return less than 5% in 2013. Hmmm, I wonder if he’d predict the same thing now that the market is up about +4.5% during the first 18 days of the year?

Why Double-Rip Over Double-Dip?

How can stocks rip if economic growth is so sluggish? If forced to equate our private sector to a car, opinions would vary widely. We could probably agree the U.S. economy is no Ferrari. Faster growing countries like China, which recently reported 4th quarter growth of +7.9% (up from +7.4% in 3rd quarter), have lapped us complacent, right-lane driving Americans in recent years. But speed alone should not be investors’ only key objective. If speed was the number one priority, the only places investors would be placing their money would be in countries like Rwanda, Turkmenistan, and Libya (see Business Insider article). However, freedom, rule of law, and entrepreneurial spirit are other important investment factors to be considered. The U.S. market is more like a Toyota Camry – not very flashy, but it will reliably get you from point A to point B in an efficient and safe manner.

Beyond lackluster economic growth, corporate profit growth has slowed remarkably. In fact, with about 10% of the S&P 500 index companies reporting 4th quarter earnings thus far, earnings growth is expected to rise a measly 2.5% from a year ago (from a previous estimate of 3.0% growth). With this being the case, how can stock prices go up? Shrewd investors understand the stock market is a discounting mechanism of future fundamentals, and therefore stocks will move in advance of future growth. It makes sense that before a turn in the economy, the brakes will often be activated before accelerating into another fast moving straight-away.

In addition, valuation acts like shock absorbers. With generational low interest rates and a below-average forward 12-month P/E (Price-Earnings) ratio of 13x’s, this stock market car can absorb a significant amount of fundamental challenges. The oft quoted message that “In the short run, the market is a voting machine but in the long run it is a weighing machine,” from value icon Benjamin Graham holds as true today as it did a century ago. The recent market advance may be attributed to the voters, but long-term movements are ultimately tied to the sustainable scales of sales, earnings, and cash flows.

If that’s the case, how can someone be optimistic in the face of the slowing growth challenges of this year? What 2013 will not have is the drag of election uncertainty, the fiscal cliff, Superstorm Sandy, and an end-of-the-world Mayan calendar concern. This is setting the stage for improved fundamentals as we progress deeper into the year. Certainly there will be other puts and takes, but the absence of these factors should provide some wind under the economy’s sails.

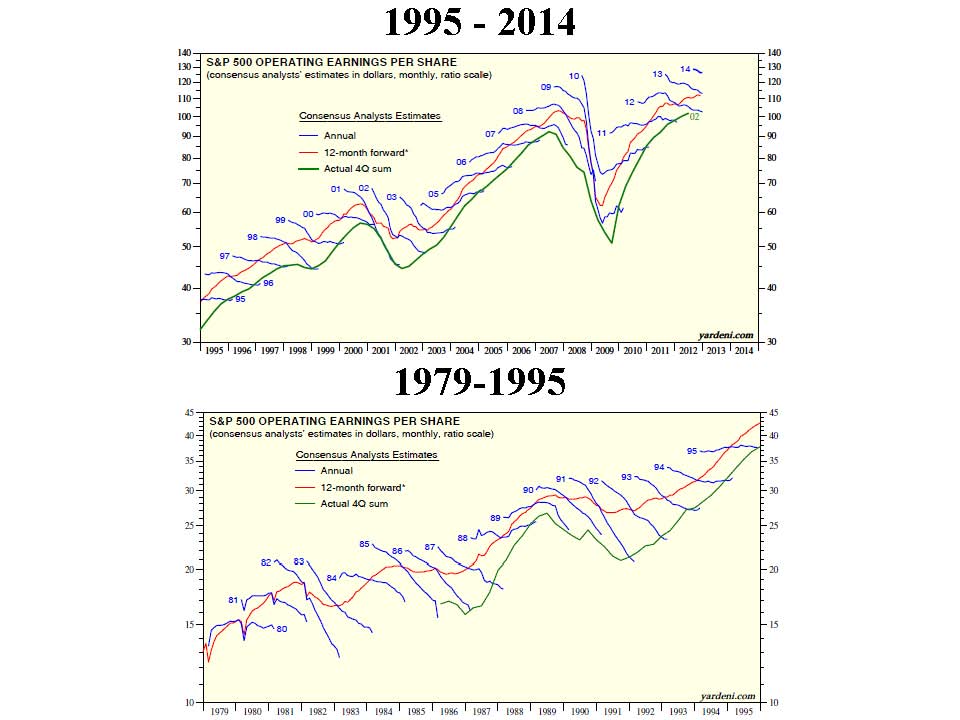

What’s more, history shows us that indeed stock prices can go up quite dramatically (more than +325% during the 1990s) when consensus earnings forecasts continually get trimmed. We have seen this same dynamic since mid-2012 – earnings forecasts have come down and stock prices have gone up. Strategist Ed Yardeni captures this point beautifully in a recent post on his Dr. Ed’s Blog (see charts below).

CLICK TO ENLARGE – Source: Dr. Ed’s Blog

What Will Make Me Bearish?

Am I a perma-bull, incessantly wearing rose-colored glasses that I refuse to take off? I’ll let you come to your own conclusion. When I see a combination of the following, I will become bearish:

#1. I see the trillions of dollars parked in near-0% cash start coming outside to play.

#2. See Pimco’s Bill Gross and Mohammed El-Erian on CNBC fewer than 10 times per week.

#3. See money flow stop flooding into sub-3% bonds (Scott Grannis) and actually reverse.

#4. Observe a sustained reversal in hemorrhaging of equity investments (Scott Grannis).

#5. Yield curve flattens dramatically or inverts.

#6. Nouriel and his bear buds become bullish and call for a “triple-rip” turn in the equity markets.

#7. Smarter, more-experienced investors than I, á la Warren Buffett, become more cautious. I arrogantly believe that will occur in conjunction with some of the previously listed items.

Despite my firm beliefs, it is evident the bears won’t go down without a fight. If you are getting tired of drinking the double-dip Kool-Aid, then perhaps it’s time to expand your bullish horizons. If not, just wait 12 months after a market rally, and buy yourself a fresh copy of the Merriam-Webster dictionary. There you can locate and learn about a new definition…double-rip!

Read Also: Double-Dip Guesses are “Probably Wrong”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in Fiat, Toyota, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fence-Sitting: The Elusive Art of More Data and Pullbacks

The world of financial markets is full of fence-sitters, especially in the professional realm. Why? Well, for starters, fence-sitting provides the luxury of never being wrong. If fence-squatting observers do nothing and provide no opinions, then they cannot by definition be wrong or mistaken. Why should a professional put their neck out for an economic, sector, or investment specific forecast, if there is a potential of looking stupid or losing a job?

For many, the consequences of possibly being wrong feel so horrendous that participants choose instead to sit on the non-committal fence. In most cases, the fence posts on any financial issue or investment align along the comfort of consensus thinking. Unfortunately, consensus thinking has a limited shelf life, because the views held by the majority are constantly changing. Repeatedly modifying personal opinions to match consensus views may prevent the bruising of egos, however, this naïve strategy can be destructive to long-term returns. Here are a few examples:

2000

Consensus View: New Normal tech stocks will continue explosive growth; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2006

Consensus View: Home prices will rise forever and leverage is beautiful; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2010

Consensus View: Greece and European collapse to cause a double-dip global recession; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2011

Consensus View: U.S. credit downgrade will be bad for Treasuries and rates; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: Uncertainty surrounding election bad for equities; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: China’s slowing growth and real estate bubble expected to cause a global double-dip recession; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2012

Consensus View: Impending fiscal cliff bad for equities; Consensus Outcome: Wrong; Investor Net Result: Losses and/or Lost Profits.

2013

Consensus View: Debt ceiling debate bad for equities; Consensus Outcome: ???; Investor Net Result: ???.

2013

Consensus View: Looming sequestration bad for equities; Consensus Outcome: ???; Investor Net Result: ???.

In recent years the market has continued to climb a wall of worry, but will this year be different? We shall soon see.

Placing the concern du jour aside, if consensus fears coalesce around a specific upcoming event, chances are that particular issue is already factored into existing expectations and price structures. Therefore, rather than wasting personal “worry” bandwidth on those fears, investor anxiety should be dedicated to less prevalent but potentially more impactful unknown concerns. Or if you need clarification about the unknowns to worry about, perhaps Donald Rumsfeld can clarify the situation by highlighting the risk of “unknown unknowns”:

I Love Data and Pullbacks!

When faced with apprehension or uncertainty, many fence-sitting investors revert to wanting more data or waiting for a better price. For example, I often hear, “I love stock XYZ, but I want to wait for the earnings to come out,” or analyst day, or share buyback announcement, or merger closing, or restructuring, etc., etc., etc. For strategists and economists, they are famished for the next critically irrelevant weekly jobless claims number, Federal Reserve policy minutes, ISM monthly manufacturing data, or latest consumer confidence figure.

More data for fence sitters is not sufficient. I often listen to stock-pickers say, “I love XYZ stock, but not at the current $52.50 price, but I’ll back up the truck at $51.50!” Okay, so you’re telling me that you think the stock is worth +40% more, but you want to litigate the purchase price over $1?!

Sadly, there is a cost for all this fence-sitting: a) if good news comes out, investment prices catapult higher and the investor is stuck with a pricier investment; b) if bad news comes out, that long-awaited price pullback is usually not acted upon because fundamentals have now deteriorated; or c) in many cases the price grinds higher before the long-awaited jewel of information is disseminated. The net result is further fence-sitting paralysis, which paradoxically is not helped by more information or a price pullback.

The other reason fence-sitters say or do nothing is because articulating a gloomy thesis simply sounds smarter. For instance, saying “The reason I’m on the sidelines is because we are in a secular bear market due to the debasement of our currency as a result of inflationary Fed monetary policies,” sounds smarter and more compelling than “Stocks are cheap and are already factoring in a lot of negativity.”

Investing is an unbelievably challenging endeavor, but for those fence-sitters with an insatiable appetite for more data and elusive pullbacks, I humbly point out, there is an infinite amount of information that regenerates itself daily. In addition, there is nothing wrong with having a disciplined valuation process in place, but if your best investment ideas are predicated on a minor pullback, then enjoy watching your returns wither away…as you sit on your cozy fence.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

2012 Party Train Missed Thanks to F.U.D.

Article is an excerpt from previously released Sidoxia Capital Management’s complementary January 2, 2013 newsletter. Subscribe on right side of page.

There was plenty of fear, uncertainty, and doubt (F.U.D.) in 2012, and the gridlock in Washington has been a contributing factor to investors’ angst. As the saying goes, the stock market climbs a “wall of worry” and that was certainly the case this year with the S&P 500 index rising +13.4% (over +15% including dividends), and the Nasdaq index soaring +15.9% before dividends. Short-term investors had ample worries to fret about throughout the year, including a European financial collapse, the presidential elections, fiscal cliff negotiations, and a Mayan doomsday (see this hilarious clip). Despite these fears dominating the daily airwaves and newspaper headlines, long-term investors holding an adequate equity asset allocation jumped on the non-stop 2012 party train.

While Americans were served a full plate of concerns this year, global investors benefited from European Central Bank intervention by Mario Draghi who promised to do “whatever it takes” to save the euro currency (the European dominated EAFE index rose +13.6% in 2012). Growth here in the U.S. slowed as cautious consumers and businesses horded cash, but a rebound in the domestic housing market provided support to the sluggish economic expansion (3rd quarter GDP growth was revised higher to +3.1% vs. 2011).

Now that the presidential elections are over and we achieved a partial fiscal cliff deal, the amount of F.U.D. going into 2013 will diminish, which should provide a tailwind to economic growth and the financial markets. The impending debt ceiling and deficit reduction talks may slow the train down, but if a sufficient resolution can be accomplished, the economic party train can continue chugging along.

Attention: Grab Your Ear Muffs

Economists and strategists will continue to sound smart and be completely wrong about their 2013 predictions (see Strategist Predictions & MacGyver), but that won’t stop average investors from neglecting their long-term investment plans. Investors have commonly overindulged in certain narrow asset classes like overpriced bonds and gold, which both underperformed equities in 2012. Diversification may sound like an overused finance cliché, but the principle is paramount if you are serious about reducing risk, beating inflation, and smoothing out incessant volatility.

2013 New Year’s Resolution: Avoid Personal Fiscal Cliff

With the New Year upon us, just because politicians have financial problems, it doesn’t mean you have to be fiscally irresponsible too. There is no better time than now to make a financial New Year’s resolution to avoid your own personal fiscal cliff. If you are too heavily parked in cash or over-exposed to low-yielding bonds subject to significant interest rate risk, then now is the time to re-evaluate your investment plan.

There is always something to worry about (see also Uncertainty: Love It?), but in order to prevent working into your 80s, a long-term investment plan needs to be implemented, regardless of economic headlines or market volatility. In other words, investors need to replace their short-term microscope for their long-term telescope. By committing to a disciplined fiscal New Year’s resolution, you can earn a ticket on the 2013 party train!

Monthly News Tidbits

The presidential elections dominated the news cycle in November, but there were a whole host of other tidbits occurring over the last thirty-one days. Here are some of the main storylines:

Congress Approves Mini Fiscal Cliff Deal: After months of debate, Congress painfully and reluctantly agreed upon an estimated $600 billion mini fiscal cliff deal that represents the largest tax increase in two decades. Contrary to a $4 trillion “Grand Bargain” deal, this bill amounts to a more modest reduction in the deficit over 10 years. The Senate passed the bill by a margin of 89-8 and the House of Representatives by a spread of 257-167. The fact that any deal got done is somewhat surprising since the gridlock has been especially rampant in the House. As proof of this assertion, one need only point to the chamber’s meager voting activity record – the House has passed the fewest bills in 60 years during its recent term.

Fiscal Cliff Bill Details: Despite the Senate’s convincing voting margin, large numbers of Congressional Democrats and Republicans were unhappy with the bill’s details. The President made good on his campaign promises by securing revenue-raising taxes from wealthy Americans. More specifically, the law contains provisions including a 39.6% rate on earners above $400,000; a 20% capital gains rate increase from 15%; new exemption/deduction limits; an estate tax increase to 40% from 35%; and a measure to help prevent near-term milk price spikes. There are plenty more details, but I will spare your eyeballs and brain from the painful minutiae. If you haven’t had enough partisan politics, no need to worry, you have the debt ceiling debate to look forward to in a few months.

Quantitative Easing Redux (QE4): Federal Reserve Chairman Ben Bernanke helped orchestrate additional monetary policy stimulus via a fourth round of quantitative easing (a.k.a., QE4). As part of this plan, the Fed will vastly expand its $2.8 trillion balance sheet in 2013 with additional monthly purchases of $45 billion of long-term Treasuries. By executing this invigorating QE4 bond buying program, the Fed pledges to keep interest rates in the cellar until the unemployment rate falls below 6.5% or inflation rises above 2.5%.

Same-Sex Marriage: The Supreme Court tackled a long-debated social issue and declared it would rule on the legality of a law denying benefits to same-sex couples in 2013.

New Female President: Additional hormones were added to the gender-skewed global pool of testosterone-filled leaders as South Korea elected its first female president, Park Geun-hye.

Global Bank Fined: Another greedy financial institution got caught with its hand in the cookie jar. UBS agreed to cough up a $1.5 billion penalty to the U.S., U.K., and Swiss authorities as part of an agreement to resolve its involvement in the manipulation of the London Interbank Offered Rate (LIBOR) – see also Wall Street Meets Greed Street.

Sandy Hook Distressing Disaster: The gun control debate was reignited when 20-year-old Adam Lanza gunned down 20 children and 7 adults (including his mother) at a Connecticut elementary school – Sandy Hook Elementary. Besides the examination of an assault weapons ban, the government needs to revisit the inadequate awareness and resources devoted to the serious issue of mental illness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including fixed income ETFs, but at the time of publishing SCM had no direct position in EFA, UBS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

2012 Investing Caffeine Greatest Hits

Source: Photobucket

Between Felix Baumgartner flying through space at the speed of sound and the masses flapping their arms Gangnam style, we all still managed to survive the Mayan apocalyptic end to the world. Investing Caffeine also survived and managed to grow it’s viewership by about +50% from last year.

Thank you to all the readers who inspire me to spew out my random but impassioned thoughts on a somewhat regular basis. Investing Caffeine and Sidoxia Capital Management wish you a healthy, happy, and prosperous New Year in 2013!

Here are some of the most popular Investing Caffeine postings over the year:

Explaining how billions of dollars in stock selling can lead to doubling in stock prices.

2) Uncertainty: Love It or Hate It?

Source: Photobucket

Good investors love ambiguity.

3) USA Inc.: Buy, Hold or Sell?

What would you do if our country was a stock?

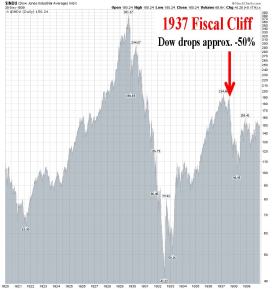

4) Fiscal Cliff: Will a 1937 Repeat = 2013 Dead Meat?

Source: StockCharts.com

Determining whether history will repeat itself after the presidential elections.

5) Robotic Chain Saw Replaces Paul Bunyan

How robots are changing the face of the global job market.

6) Floating Hedge Fund on Ice Thawing Out

Lessons learned from Iceland four years after Lehman Brothers.

7) Sidoxia’s Investor Hall of Fame

Continue reading at IC & perhaps you too can become a member?!

8) Broken Record Repeats Itself

It appears that the cycle from previous years is happening again.

9) The European Dog Ate My Homework

Explaining the tight correlation of European & U.S. markets, and what to do about it.

10) Cash Security Blanket Turns into Tourniquet

Stock market returns are beginning to make change perceptions about holding cash.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Gobbling Up the All-You-Can-Eat Data Buffet

Gorging oneself at an all-you-can eat buffet has its advantages, but managing the associated extra pounds and bloatedness carries its own challenges. In a similar fashion, businesses and consumers are devouring data at an exponential rate, while simultaneously attempting to slice, dice, manage, and store all of this information. Data is quickly becoming as cheap as oxygen, and there are virtually no limitations on the amount consumed.

With the help of my handy smart phone, tablet, and digital camera, I can almost store and watch every moment of my life, very much like the movie The Truman Show. Social media and cloud services, coupled with inexpensive storage, have only made it simpler to digitally archive my life. Pretty soon, with the click of a mouse (or tap of the tablet) everyone will be able to instantaneously access every important moment of their life from cradle to grave.

Consuming Data Bytes at a Time

If you are in the mood for consuming free data, there are plenty of free multi-gigabyte services to choose from, including Dropbox, Mozy, and SkyDrive among other. For those chomping on more than 25 gigabytes of data, paid services like Amazon.com’s (AMZN) Simple Storage Service (a.k.a, “S3”) allow users to store a terabyte of data for about $0.01 – $0.05 per month. However, if renting storage is not your gig (no pun intended), you can own your personal storage device for next to nothing. In fact, you can buy a 1 terabyte (equal to 1,000 gigabytes) external hard drive today for less than $70. If that’s too rich for your blood, then just wait 12 months or so and pay $50 bucks. To put a terabyte in context, this amount of storage can hold approximately 625,000 high quality photos or 412 DVD quality movies, according to a Financial Times article talking about “big data.”

A terabyte may sound like a lot, but if we’re going to be honest, this amount of storage is Tiddly Winks. Once we start talking about petabytes (1,000 terabytes), exabytes (1,000,000 terabytes), and zettabytes (1 billion terabytes), things begin to get a little more interesting (see chart below). If you consider that 2012 global data center traffic estimates amount to 2.6 zettabytes (or 2.6 billion terabytes), it doesn’t take long to appreciate the enormity of the data management challenge facing billions of people.

Source: The Financial Times

The Financial Times also points out the following:

“From the beginning of recorded time until 2003, we created five exabytes of data. In 2011 the same amount was created every two days. By 2013 it’s expected that the time will shrink to 10 minutes.”

Digital World Driving Data Appetite

What’s driving the global gusher of data growth? There’s not just one answer, but one can start understanding the scope of the issue after contemplating the trillions of annual text messages; 1 billion Facebook (FB) users; 800 million monthly YouTube visitors watching 4 billion hours of videos; six billion cell phones worldwide; and a global 122 million tablet market (IDC).

I certainly wasn’t the first person to discover this megatrend, but I am not hesitating to invest both my client’s money and my money into benefiting from this massive growth trend. Businesses are prospering from the data tidal wave too, as evidenced in part by Oracle Corp’s (ORCL) stellar quarterly earnings results reported just a few days ago. The mass migration of services to the “cloud” (software delivered over the internet) combined with the need to manage and store exploding industry data, resulted in Oracle reporting growth of +18% in its profitable Software License Sales and Cloud Subscriptions segment. With results like these, no wonder Oracle’s founder and CEO Larry Ellison owns a 141-mile square island, a multi-hundred million yacht, and is worth $41 billion according to Forbes (#3 on the Forbes 400 list).

Whether you realize it or not, we are all consuming heaps of all-you-can eat data at the digital buffet. Rather than rolling over into a data consumption coma, you will be much better off figuring out how to profit from the exploding data trends.

See also: The Age of Information Overload

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), GOOG, and AMZN, but at the time of publishing SCM had no direct positions in FB, ORCL, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}