Posts filed under ‘Themes – Trends’

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

Profits

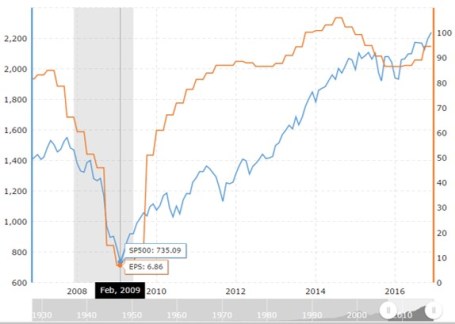

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

Interest Rates

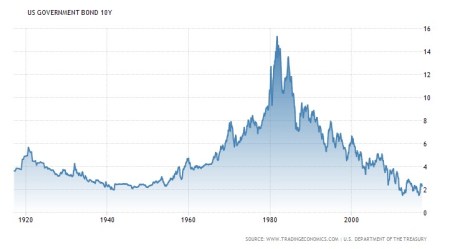

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Fallacy Behind Populism and Automation Fears

The rise of global populism and anti-immigration sentiments, coupled with the perpetual rising trend of automation and robotics has stoked the fear fires of job security. Many stories perpetuate erroneous stereotypes and falsehoods. The news reports and blog articles come in various flavors, but in a nutshell the stories state the U.S. is hemorrhaging jobs due to the thieves of illegal immigration and heartless robotics. The job displacement theory is built upon the idea that these two sources of labor (immigrants & robots) are cheaper and more productive than traditional blue collar and white collar American workers.

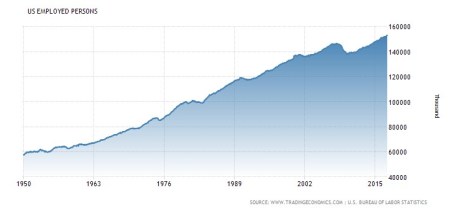

Although these logical beliefs make for great soundbites, and may sell subscriptions and advertising, unfortunately the substance behind the assertions holds little water. Let’s take a look at the facts. In the most recent April jobs report, nonfarm payrolls employment increased by 211,000 jobs, according to the U.S. Bureau of Labor Statistics. Since early 2009 the unemployment rate has plummeted from 10.0% down to a historically low level of 4.4%. Over the similar timeframe, the economy has added over 15,000,000 new jobs. Does this sound like an environment in which immigrants and robots are killing all American jobs?

Sounds like a bunch of phoney-baloney, if you ask me. Just look at the employed person chart below, which shows a rising employment trend over the last seven decades, with the exception of some brief recessionary periods.

As I point out in a previous article (see Rise of the Robots), from the beginning of the United States, the share of the largest segment of the economy (agriculture) dropped by more than 98%, yet the standard of living and output in the agriculture sector have still exploded. There may not have been robots two and a half centuries ago, but technology and automation were alive and well, just as they are today. Although there were no self-driving cars, no internet, no biotech drugs, and no mobile phones, there were technological advances like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds over time.

Source: Carpe Diem

And while there most certainly were farmers who regrettably were displaced by these technologies, there were massive new industries fostered by the industrial revolution, which redeployed labor to new burgeoning industries like manufacturing, aerospace, transportation, semiconductors, medicine, and many more.

While it may be difficult to fathom what industries will replace the workers displaced by self-service kiosks at restaurants, airports, and retail stores, famed economist Milton Friedman summed it up best when he stated:

“Human wants & needs are infinite, and so there will always be new industries, there will always be new professions.”

As globalization and technology continue permeating through society, it is true, the importance of education becomes more critical. Billions of people around the globe in developing markets, along with automation technology, will be stealing lower-paying American jobs that require repetitive processes. Educating our workforce up the value-add food chain is imperative.

The bottom-line is that integration of technology and automation will improve the standard of living for the masses. Sure, immigration will displace some workers, but if legislative policy can be designed to cherry-pick (attract) the cream of the skilled foreign crop (and retrain displaced workers), skilled immigrants will keep on innovating and creating higher valued jobs. Just consider a recent study that shows 51% of U.S. billion-dollar startups were founded by immigrants.

The populist drum may continue to pound against immigration, and horror stories of job-stealing robots may abound, however the truth cannot be erased. Over the long-run, the fallacies behind populism and automation will be uncovered. The benefits and truths surrounding highly skilled immigrants and robots will be realized, as these dynamics dramatically improve the standard of living and productivity of our great economy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Glass Half Full or Half Empty?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2017). Subscribe on the right side of the page for the complete text.

We live in a time of confusing dichotomies, which makes deciphering the flood of daily data quite challenging. In that context, determining whether the current economic fundamentals should be viewed from a glass half empty of glass half full perspective can be daunting.

More specifically, stock markets have again recently hit new all-time record highs, yet if you read the newspaper headlines, you might think we’re in the midst of Armageddon. Last month, the Dow Jones Industrial Average stock index eclipsed 21,000 and the technology-heavy NASDAQ index surpassed the psychologically important 6,000 threshold. In spite of the records, here’s a sampling of the steady stream of gloomy feature stories jamming the airwaves:

- French Elections – Danger of European Union Breakup

- Heightened Saber Rattling by U.S. Towards North Korea

- Threat of U.S. Government Shutdown

- First 100 Days – Obamacare repeal failure, tax reform delays, no significant legislation

- NAFTA Trade Disputes

- Russian Faceoff Over Syrian Civil War & Terrorism

- Federal Reserve Interest Rate Hikes Could Derail Stock Market

- Slowing GDP / Economic Data

Given all this doom, how is it then that stock markets continue to defy gravity and continually set new record highs? Followers of my writings understand the crucial, driving dynamics of financial markets are not newspaper, television, magazine, and internet headlines. The most important factors are corporate profits, interest rates, valuations, and investor sentiment. All four of these elements will bounce around, month-to-month, and quarter-to-quarter, but for the time being, these elements remain constructive on balance, despite the barrage of negative, gut-wrenching headlines.

Countering the perpetual flow of gloomy, cringe-worthy headlines, we have seen a number of positive developments:

- Record Breaking Corporate Profits: Profits are the chief propellant for higher stock prices, and so far, for the 1st quarter, S&P 500 company profits are estimated to have risen +12.4% – the highest rate since 2011, according to Thomson Reuters I/B/E/S. As I like to remind my readers, stock prices follow profits over the long-run, which is evidenced by the chart below.

Source: Trading Economics

- Interest Rates Low: With interest rate levels still near generational lows (10-Year Treasury @ 2.28%), and inflation relatively stable around 2%, this augurs well for most asset prices. For U.S. consumers there are many stimulative effects to lower interest rates, whether you are buying a house, purchasing a car, paying off a school loan, and/or reducing credit card debt. Lower rates equal lower payments.

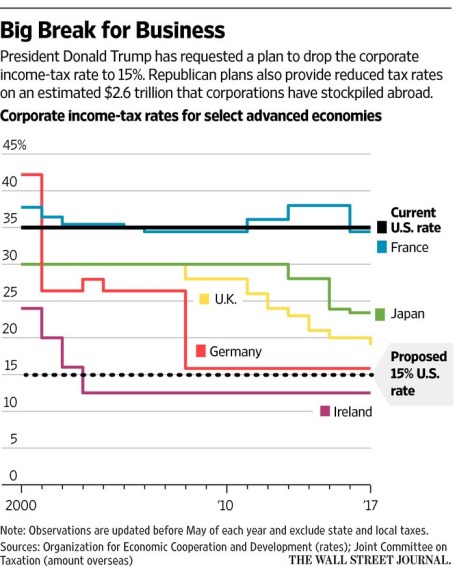

- Potential Tax Reform: There are numerous stimulative components to the largest planned tax-cut in history. First of all, cutting the tax rate from 35% to 15% for corporations and small businesses (i.e. pass-through entities like LLCs and S-Corps) would place a lot of dollars back in the pockets of taxpayers and should stimulate economic growth. Other components of the White House proposal include the termination of the estate tax, the elimination of the AMT (Alternative Minimum Tax) targeted at wealthier households, and the doubling of the standard deduction to help middle-income families. All of this sounds great on paper, but not a lot of details have been provided yet on how these benefits will be paid for – removing state tax deductions alone is unlikely to fully offset revenue declines. The chart below highlights how high U.S. corporate income tax rates are relative to other foreign counterparts.

Source: The Wall Street Journal

- Business Spending & Confidence on the Rise: Ever since the 2008-09 Great Recession, the U.S. has been a better house in a bad neighborhood relative to other global developed economies. However, the recovery has been gradual and muted due to tight-fisted companies being slow to hire and invest. Although recent Q1 GDP economic data came in at a sluggish +0.7% growth rate, the bright spot embedded in the data was a +12% annualized increase in private fixed investment. This is consistent with the spike we’ve seen in recent business and consumer confidence surveys (see chart below). Although this confidence has yet to translate into an acceleration in broader economic data, the ramp in capital spending and positive business sentiment could be a leading indicator for faster economic growth to come. Stimulative legislation enacted by Congress (i.e., tax reform, infrastructure spending, foreign repatriation, etc.) could add further fuel to the economic growth engine.

Source: Trading Economics

- Economy Keeps Chugging Along: As the wealthiest country on the planet, we Americans can become a little spoiled with success, which helps explain the media’s insatiable appetite for growth. Nevertheless, the broader economic data show a continuing trend of improvement. Simply consider the trend occurring in these major areas of the economy:

- Unemployment – The jobless rate has been chopped by more than half from a 10.0% cycle peak to 4.5% today.

- Housing – The number of annual existing home sales has increased by more than +60% from the cycle low to 5.7 million units, which still leaves plenty of headroom for growth before 2006 peak sales levels are reached.

- Consumer Spending – This segment accounts for roughly 70% of our country’s economic activity. Although we experienced a soft patch in Q1 of 2017, as you can see from the chart below, we Americans have had no problem spending more to keep our economy functioning.

Source: Trading Economics

While key economic statistics remain broadly constructive, there will come a time when prudence will dictate the pursuit of a more defensive investment strategy. When will that be? In short, the time to become more cautious will be when we see a combination of the following occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

To date, there is no objective evidence indicating these dynamics are in place, so until then, I will remain thirsty and grab my half glass full of water.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Managing the Chaos – Investing vs. Gambling

How does one invest amid the slew of palm sweating, teeth grinding headlines of Syria, North Korea, Brexit, expanding populism, Trumpcare, French candidate Marine Le Pen, and a potential government shutdown? Facing a persistent mountain of worries can seem daunting to many. With so many seemingly uncontrollable factors impacting short-term interest rates, foreign exchange rates, and equity markets, it begs the question of whether investing is a game of luck (gambling) or a game of skill?

The short answer is…it depends. Professional gambler Alvin “Titanic” Thompson captured the essence when someone asked him whether poker was a game of chance. Thompson responded by stating, “Not the way I play it.”

If you go to Las Vegas and gamble, most games are generally a zero sum-game, meaning there are an equal number of winners and losers with the house (casino) locking in a guaranteed spread (profit). For example, consider a game like roulette – there are 18 red slots, 18 black slots, and 2 green slots (0 & 00), so if you are betting on red vs. black, then the casino has a 5.26% advantage. If you bet long enough, the casino will get all your money – there’s a reason Lost Wages Las Vegas can build those extravagantly large casinos.

The same principles of money-losing bets apply to speculative short-term trading. Sure, there are examples of speculators hitting it big in the short-run, but most day traders lose money (see Day Trading Your House) because the odds are stacked against them. In order to make an accretive, profitable trade, not only does the trader have to be right on the security they’re selling (i.e. that security must underperform in the future), but they also have to be right on the security they are buying (i.e. that security must outperform in the future). But the odds for the speculator get worse once you also account for the trading fees, taxes, bid-ask spreads, impact costs (i.e., liquidity), and informational costs (i.e., front running, high frequency traders, algorithms, etc.).

The key to winning at investing is to have an edge, and the easiest way to have an investing edge is to invest for the long-run – renowned Professor Jeremy Siegel agrees (see Stocks for the Long Run). It’s common knowledge the stock market is up about two-thirds of the time, meaning the odds and wind are behind the backs of long-term investors. Short-term trading is the equivalent of going fishing, and then continually pulling your fishing line out of the water (you’re never going to catch anything). The fisherman is better off by researching a good location and then maintaining the lure in the water for a longer period until success is achieved.

Although most casino games are based on pure luck, there are some games of skill, like poker, that can produce consistent long-term positive results, if you are a patient professional with an advantage or edge (see Dan Harrington article ). Having an edge in investing is crucial, but an edge is not the only aspect of successful investing. How you structure a portfolio to control risk (i.e., money management), and reducing your personal behavioral biases are additional components to a winning investment strategy. Professional poker player Walter Clyde “Puggy” Pearson summed it up best when he described the three critical components to winning:

“Knowing the 60-40 end of a proposition, money management, and knowing yourself.”

At Sidoxia Capital Management, we have also achieved long-term success by following a systematic, disciplined process. A large portion of our investment strategy is focused on identifying market leading franchises with a long runway of growth, and combining those dynamics with positions trading at attractive or fair values. As part of this process, we rank our stocks based on multiple factors, primarily using data from our proprietary SHGR ranking (see Investing Holy Grail) and free cash flow yield analysis, among other important considerations. Based on the risk-reward profiles of our existing holdings and the pool of targeted investments, we can appropriately size our positions accordingly (i.e., money management). As valuations rise, or risk profiles deteriorate, we can make the corresponding portfolio positions cuts, especially if we find more attractive alternative investments. Having a proven, systematic, unbiased process has helped us tremendously in minimizing behavioral pitfalls (i.e., knowing yourself) when we construct client portfolios.

The world is under assault…but that has always been the case. Throughout investment history, there have been wars, assassinations, unexpected election outcomes, banking crises, currency crises, natural disasters, health epidemics, and more. Unfortunately, millions have gambled and bet their money away based on these frivolous, ever-changing, short-term headlines. On the other hand, those investors who understand the 60-40 end of a proposition, coupled with the importance of money management and controlling personal biases, will be the skillful winners to prosper over the long-run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investing in a World of Black Swans

In the world of modern finance, there has always been the search for the Holy Grail. Ever since the advent of computers, practitioners have looked to harness the power of computing and direct it towards the goal of producing endless profits. Today the buzz words being used across industries include, “AI – Artificial Intelligence,” “Machine Learning,” “Neural Networks,” and “Deep Learning.” Regrettably, nobody has found a silver bullet, but that hasn’t slowed down people from trying. Wall Street has an innate desire to try to turn the ultra-complex field of finance into a science, just as they do in the field of physics. Even banking stalwart JPMorgan Chase (JPM) and its renowned CEO/Chairman Jamie Dimon suffered billions in losses in the quest for infinite income, due in large part to their over-reliance on pseudo-science trading models.

Preceding JPM’s losses, James Montier of Grantham Mayo van Otterloo’s asset allocation team gave a keynote speech at a CFA Institute Annual Conference in Chicago, where he gave a prescient talk explaining why bad models were the root cause of the financial crisis. Montier noted these computer algorithms essentially underappreciate the number and severity of Black Swan events (low probability negative outcomes) and the models’ inability to accurately identify predictable surprises.

What are predictable surprises? Here’s what Montier had to say on the topic:

“Predictable surprises are really about situations where some people are aware of the problem. The problem gets worse over time and eventually explodes into crisis.”

When Dimon was made aware of the 2012 rogue trading activities, he strenuously denied the problem before reversing course and admitting to the dilemma. Unfortunately, many of these Wall Street firms and financial institutions use value-at-risk (VaR) models that are falsely based on the belief that past results will repeat themselves, and financial market returns are normally distributed. Those suppositions are not always true.

Another perfect example of a Black Swan created by a bad financial model is Long Term Capital Management (LTCM) – see also When Genius Failed. Robert Merton and Myron Scholes were world renowned Nobel Prize winners who single-handedly brought the global financial market to its knees in 1998 when LTCM lost $500 million in one day and required a $3.6 billion bailout from a consortium of banks. Their mathematical models worked for a while but did not fully account for trading environments with low liquidity (i.e., traders fleeing in panic) and outcomes that defied the historical correlations embedded in their computer algorithms. The “Flash Crash” of 2010, in which liquidity evaporated due to high-frequency traders temporarily jumping ship, is another illustration of computers wreaking havoc on the financial markets.

The problem with many of these models, even for the ones that work in the short-run, is that behavior and correlations are constantly changing. Therefore any strategy successfully reaping outsized profits in the near-term will eventually be discovered by other financial vultures and exploited away.

Another pundit with a firm hold on Wall Street financial models is David Leinweber, author of Nerds on Wall Street. As Leinweber points out, financial models become meaningless if the data is sliced and diced to form manipulated and nonsensical relationships. The data coming out can only be as good as the data going in – “garbage in, garbage out.”

In searching for the most absurd data possible to explain the returns of the S&P 500 index, Leinweiber discovered that butter production in Bangladesh was an excellent predictor of stock market returns, explaining 75% of the variation of historical returns. By tossing in U.S. cheese production and the total population of sheep in Bangladesh, Leinweber was able to mathematically “predict” past U.S. stock returns with 99% accuracy. To read more about other financial modeling absurdities, check out a previous Investing Caffeine article, Butter in Bangladesh.

Generally, investors want precision through math, but as famed investor Benjamin Graham noted more than 50 years ago, “Mathematics is ordinarily considered as producing precise, dependable results. But in the stock market, the more elaborate and obtuse the mathematics, the more uncertain and speculative the conclusions we draw therefrom. Whenever calculus is brought in, or higher algebra, you can take it as a warning signal that the operator is trying to substitute theory for experience.”

If these models are so bad, then why do so many people use them? Montier points to “intentional blindness,” the tendency to see what one expects to see, and “distorted incentives” (i.e., compensation structures rewarding improper or risky behavior).

Montier’s solution to dealing with these models is not to completely eradicate them, but rather recognize the numerous shortcomings of them and instead focus on the robustness of these models. Or in other words, be skeptical, know the limits of the models, and build portfolios to survive multiple different environments.

Investors seem to be discovering more financial Black Swans over the last few years in the form of events like the Lehman Brothers bankruptcy, Flash Crash, and Greek sovereign debt default. Rather than putting too much faith or dependence on bad financial models to identify or exploit Black Swan events, the over-reliance on these models may turn this rare breed of swans into a large bevy.

See Full Article on Montier: Failures of Modern Finance

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own JPM and certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Double Dip Expansion?

Ever since the 2008-2009 financial crisis, every time the stock market has experienced a -5%, -10%, or -15% correction, industry pundits and media talking heads have repeatedly sounded the “Double Dip Recession” alarm bells. As you know, we have yet to experience a technical recession (two reported quarters of negative GDP growth), and stock prices have almost quadrupled from a 2009 low on the S&P 500 of 666 to 2,378 today (up approximately +257%).

Over the last nine years, so-called experts have been warning of an imminent stock market collapse from the likes of PIIGS (Portugal/Italy/Ireland/Greece/Spain), Cyprus, China, Fed interest rate hikes, Brexit, ISIS, U.S. elections, North Korea, French elections, and other fears. While there have been plenty of “Double Dip Recession” references, what you have not heard are calls for a “Double Dip Expansion.”

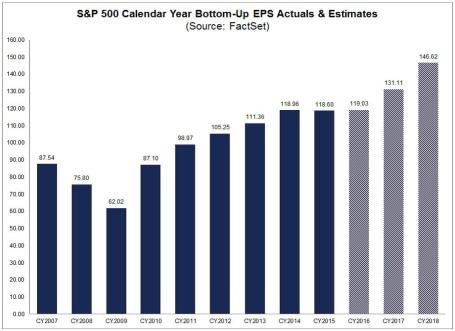

Is it possible that after the initial 2010-2014 economic expansionary rebound, and subsequent 2015-2016 earnings recession caused by sluggish global growth and a spike in the value of the U.S. dollar, we could possibly be in the midst of a “Double Dip Expansion?” (see earnings chart below)

Source: FactSet

Whether you agree or disagree with the new political administration’s politics, the economy was already on the comeback trail before the November 2016 elections, and the momentum appears to be continuing. Not only has the pace of job growth been fairly consistent (+235,000 new jobs in February, 4.7% unemployment rate), but industrial production has been picking up globally, along with a key global trade index that accelerated to 4-5% growth in the back half of 2016 (see chart below).

Source: Calafia Beach Pundit

This continued, or improved, economic growth has arisen despite the lack of legislation from the new U.S. administration. Optimists hope for an improved healthcare system, income tax reform, foreign profit repatriation, and infrastructure spending as some of the initiatives to drive financial markets higher.

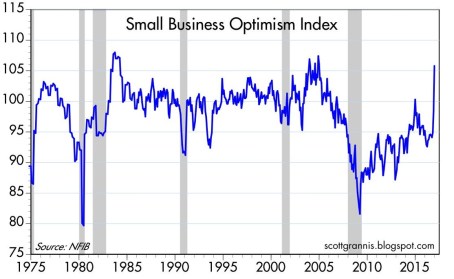

Pessimists, on the other hand, believe all these proposed initiatives will fail, and cause financial markets to fall into a tailspin. Regardless, at least for the period following the elections, investors and companies have perceived the pro-business rhetoric, executive orders, and regulatory relief proposals as positive developments. It’s widely understood that small businesses supply the largest portion of our nation’s jobs, and the upward spike in Small Business Optimism early in 2017 is a welcome sign (see chart below).

Source: Calafia Beach Pundit

Yes, it is true our new president could send out a rogue tweet; start a trade war due to a tariff slapped on a critical trading partner; or make a hawkish military remark that isolates our country from an ally. These events, along with other potential failed campaign promises, are all possibilities that could pause the trajectory of the current bull market. However, more importantly, as long as corporate profits, the mother’s milk of stock price appreciation, continue to march higher, then the stock market fun can continue. If that’s the case, there will likely be less talk of “Double Dip Recessions,” and more discussions of a “Double Dip Expansion.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Re-Questioning the Death of Buy & Hold Investing

Article originally posted September 17, 2010: At the time this original article was written, the Dow Jones Industrial Average was hovering around 11,500. Last week, the Dow closed at 20,624. Sure there have been plenty of ups and downs since 2010, but as I suggested seven years ago, perhaps “buy and hold” still is not dead today?

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements arre obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty-year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly, there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: At the time the article was originally written, Sidoxia Capital Management (SCM) and some of its clients owned certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. As of 2/19/17 – Sidoxia owned AAPL, AMZN, and was short NFLX. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Stocks: Be My Long-Term Valentine

With Valentine’s Day just around the corner, stock bulls remain in love as the major indexes once again hit another new, all-time record high this week (Dow 20,269). Unfortunately, however, there are many other investors afraid of going through another 2008-2009-like break-up, so they remain single as they watch from the sidelines. In a recent post, I point out, as repeated record highs continue to be broken, the skeptics remain fearful of divorcing their cash. While it is indeed true that since the end of the 2016 presidential election, some investors are beginning to date stocks again, there are still wide swaths of conflicted observers very afraid of potential rejection.

As I’ve documented on numerous occasions, the skepticism is evident in the depressing long-term trends found in the weekly fund flows data and the disheartening record-low stock ownership statistics.

Long-Term Relationships

For some, casually dating can be fun and exciting. The same principle applies to short-term traders and speculators. In the short-run, the freedom to make free-wheeling, non-committal stock purchases can be exhilarating. Unfortunately, the fiscal and emotional costs of short-term dating/trading often outweigh the fleeting benefits.

How can you avoid the relationship blues? In short…focus on the long-term. Like any relationship, investing takes work, and there will always be highs, lows, and bumps in the road. It is better to think in terms of a marathon, rather than a sprint. The important lesson is to maintain a systematic, disciplined approach that you can apply irrespective of the changing investment environment. In other words, that means not loosely reacting (buying or selling) to presidential tweets of the day.

Famed investor Peter Lynch spoke about long-term stock fund investing in this manner

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship survives without experiencing wild swings, and stocks are no exception. Establishing deep roots to your investments via intensive fundamental analysis provides stability, especially if you are managing your portfolio personally. Even if you are outsourcing your investment management to an advisor like Sidoxia Capital Management, it is still important to understand your advisor’s investment process and philosophy. That way, when the economic and political winds are blowing fiercely, you won’t overreact emotionally and see your gains fly away.

Investing legend Warren Buffett has discussed the importance of intensive research on long-term investment performance through his “20-Hole Punch Card” rule:

“I could improve your ultimate financial welfare by giving you a ticket with only twenty slots in it so that you had twenty punches – representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all. Under those rules, you’d really think carefully about what you did, and you’d be forced to load up on what you’d really thought about. So you’d do so much better.”

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down regardless of the daily headlines.

Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually dating your investments, perhaps you should commit to a long-term relationship and divorce your bad short-term centric habits. Now that sounds like a sweet Valentine’s Day kiss your investment portfolio would enjoy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, T, FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Super Bowl Blitz – Dow 20,000

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 3, 2017). Subscribe on the right side of the page for the complete text.

If you have been following the sports headlines, then you know the Super Bowl 51 NFL football championship game between the four-time champion New England Patriots and the zero-time champion Atlanta Falcons is upon us. It’s that time of the year when more than 100 million people will congregate in front of big screen TVs across our nation and stare at ludicrous commercials (costing $5 million each); watch a semi-entertaining halftime show; and gorge on thousands of calories until stomachs bloat painfully.

The other headlines blasting across the media airwaves relate to the new all-time record milestone of 20,000 achieved by the Dow Jones Industrials Average (a.k.a., “The Dow”). For those people who are not glued to CNBC business television all day, the Dow is a basket of 30 large company stocks subjectively selected by the editors of the Wall Street Journal with the intent of creating an index that can mimic the overall economy. A lot of dynamics in our economy have transformed over the Dow’s 132 year history (1885), so it should come as no surprise that the index’s stock components have changed 51 times since 1896 – the most recent change occurred in March 2015 when Apple Inc. (AAPL) was added to the Dow and AT&T Inc. (T) was dropped.

20,000 Big Deal?

The last time the Dow closed above 10,000 was on March 29, 1999, so it has taken almost 18 years to double to 20,000. Is the Dow reaching the 20,000 landmark level a big deal in the whole scheme of things? The short answer is “No”. It is true the Dow can act as a fairly good barometer of the economy over longer periods of time. Over the 1998 – 2017 timeframe, economic activity has almost doubled to about $18 trillion (as measured by Gross Domestic Product – GDP) with the added help of a declining interest rate tailwind.

In the short-run, stock indexes like the Dow have a spottier record in correlating with economic variables. At the root of short-term stock price distortions are human behavioral biases and emotions, such as fear and greed. Investor panic and euphoria ultimately have a way of causing wild stock price overreactions, which in turn leads to poor decisions and results. We saw this firsthand during the inflation and subsequent bursting of the 2000 technology bubble. If that volatility wasn’t painful enough, last decade’s housing collapse, which resulted in the 2008-2009 financial crisis, is a constant reminder of how extreme emotions can lead to poor decision-making. For professionals, short-term volatility and overreactions provide lucrative opportunities, but casual investors and novices left to their own devices generally destroy wealth.

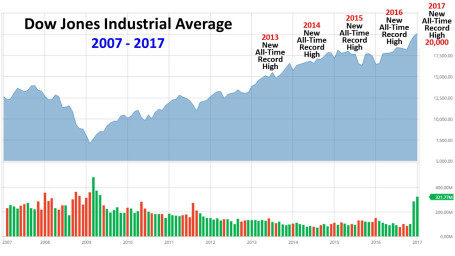

As I have discussed on my Investing Caffeine blog on numerous occasions, the march towards 20,000 occurred in the middle of arguably the most hated bull market in a generation or two (see The Most Hated Bull Market). It wasn’t until recently that the media began fixating on this arbitrary new all-time record high of 20,000. My frustration with the coverage is that the impressive phenomenon of this multi-year bull market advance has been largely ignored, in favor of gloom and doom, which sells more advertising – Madison Avenue execs enthusiastically say, “Thank you.” While the media hypes these stock records as new, this phenomenon is actually old news. In fact, stocks have been hitting new highs over the last five years (see chart below).

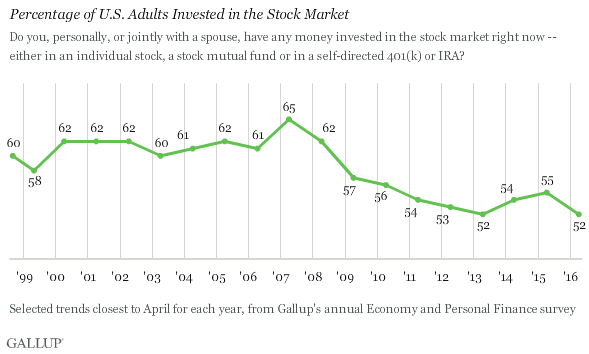

More specifically, the Dow has hit consecutive, new all-time record highs in each year since 2013. This ignored bull market (see Gallup survey) may not be good for the investment industry, but it can be good for shrewd long-term investors, who react patiently and opportunistically.

Political Football

In Washington, there’s a different game currently going on, and it’s a game of political football. With a hotly contentious 2016 election still fresh in the minds of many voters, a subset of unsatisfied Americans are closely scrutinizing every move of the new administration. Love him or hate him, it is difficult for observers to accuse President Trump of sitting on his hands. In the first 11 days of his presidential term alone, Trump has been very active in enacting almost 20 Executive Orders and Memoranda (see the definitional difference here), as he tries to make supporters whole with his many previous campaign trail promises. The persistently increasing number of policies is rising by the day (…and tweet), and here’s a summarizing list of Trump’s executive actions so far:

- Refugee Travel Ban

- Keystone & Dakota Pipelines

- Border Wall

- Deportations/Sanctuary Cities

- Manufacturing Regulation Relief

- American Steel

- Environmental Reviews

- Affordable Care Act Requirements

- Border Wall

- Exit TPP Trade Deal

- Federal Hiring Freeze

- Federal Abortion Freeze

- Regulation Freeze

- Military Review

- ISIS Fight Plan

- Reorganization of Security Councils

- Lobbyist Bans

- Deregulation for Small Businesses

President Trump has thrown another political football bomb with his recent nomination of Judge Neil Gorsuch (age 49) to the Supreme Court in the hopes that no penalty flags will be thrown by the opposition. Gorsuch, the youngest nominee in 25 years, is a conservative federal appeals judge from Colorado who is looking to fill the seat left open by last year’s death of Justice Antonin Scalia at the age 79.

Politics – Schmolitics

When it comes to the stock market and the economy, many people like to make the president the hero or the scapegoat. Like a quarterback on the football field, the president certainly has influence in shaping the political and economic game plan, but he is not the only player. There is an infinite number of other factors that can (and do) contribute to our country’s success (or lack thereof).

Those economic game-changing factors include, but are not limited to: Congress, the Federal Reserve, Supreme Court, consumer sentiment, trade policy, demographics, regulations, tax policy, business confidence, interest rates, technology proliferation, inflation, capital investment, geopolitics, terrorism, environmental disruptions, immigration, rate of productivity, fiscal policy, foreign relations, sanctions, entitlements, debt levels, bank lending, mergers and acquisitions, labor rules, IPOs (Initial Public Offerings), stock buybacks, foreign exchange rates, local/state/national elections, and many, many, many other factors.

Regardless to which political team you affiliate, if you periodically flip through your social media stream (e.g., Facebook), or turn on the nightly news, you too have likely suffered some sort of political fatigue injury. As Winston Churchill famously stated, “Democracy is the worst form of government except for all the other forms that have been tried from time to time.”

When it comes to your finances, getting excited over Dow 20,000 or despondent over politics is not a useful or efficient strategy. Rather than becoming emotionally volatile, you will be better off by focusing on building (or executing) your long-term investment plan. Not much can be accomplished by yelling at a political charged Facebook rant or screaming at your TV during a football game, so why not calmly concentrate on ways to control your future (financial or otherwise). Actions, not fear, get results. Therefore, if this Super Bowl Sunday you’re not ready to review your asset allocation, budget your annual expenses, or contemplate your investment time horizon, then at least take control of your future by managing some nacho cheese dip and handling plenty of fried chicken.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, T, FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dow 20,000 – Braking News or Breaking News?

Investors from around the globe excitedly witnessed the Dow Jones Industrial Average index break the much-anticipated 20,000 level and set a new all-time record high this week. The question now becomes, is this new threshold braking news (time to be concerned) or breaking news (time to be enthused)? The true answer is neither. While the record 20,000 achievement is a beautifully round number and is responsible for a bevy of headlines splashing around the world, the reality is this artificial 20,000 level is completely arbitrary.

Time will tell whether this random numeric value will trigger the animal spirits of dispirited investors, but given all the attention, it is likely to jolt the attention span of distracted, ill-prepared savers. Unfortunately, the median family has only saved a meager $5,000 for retirement. For some years now, I have highlighted that this is the most hated bull market (see The Most Hated Bull Market Ever), and Gallup’s 2016 survey shows record low stock ownership, which also supports my view (chart below). Trillions of dollars coming out of stock funds is additional evidence of investors’ sour mood (see fund outflow data).

While investors have been selling stocks for years, record corporate profits, trillions in share buybacks, and trillions of mergers and acquisitions (in the face of a weak IPO market) have continually grinded stock prices to new record highs.

Pessimism Sells

The maligned press (deservedly so in many instances) has been quick to highlight a perpetual list of dread du jour. The daily panic-related topics do however actually change. Some days it’s geopolitical concerns in the Middle East, Russia, South China Sea, North Korea, and Iran and other days there are economic cries of demise in China, Brazil, Venezuela, or collapse in the Euro. And even when the economy is doing fine (unemployment rate chopped in half from 10%, near full employment), the media and talking heads often supply plenty of airtime to impending spikes of crippling inflation or Fed-induced string of choking interest rate increases.

I fondly look back on my articles from 2009, and 2010 when I profiled schlocks like Peter Schiff (see Emperor Schiff Has No Clothes) who recklessly peddled catastrophe to the masses. I guess Schiff didn’t do so well when he called for the NASDAQ to collapse to 500 (5,660 today) and the Dow to reach 2,000 (20,000 today).

Or how about the great forecaster John Mauldin who also piled onto death and destruction near the bottom in 2009 (see The Man Who Cries Wolf ). Here’s what Mauldin had to say:

“All in all, the next few years are going to be a very difficult environment for corporate earnings. To think we are headed back to the halcyon years of 2004-06 is not very realistic. And if you expect a major bull market to develop in this climate, you are not paying attention.” … “We are going to pay for that with a likely dip back into a recession.”

At S&P 856 (2,295 today) Mauldin added:

“This rally has all the earmarks of a major short squeeze…When the short squeeze is over, the buying will stop and the market will drop. Remember, it takes buying and lot of it to move a market up but only a lack of buying to create a bear market.”

Nouriel Roubini a.k.a. “Dr Doom” was another talking head who plastered the airwaves with negativity after the 2008-2009 financial crisis that I also profiled (see Pinning Down Roubini). For example, in early 2009, here’s what Roubini said:

“We are still only in the early stages of this crisis. My predictions for the coming year, unfortunately, are even more dire: The bubbles, and there were many, have only begun to burst.”

For long-term investors, they understand the never-ending doom and gloom headlines are meaningless noise. Legendary investor Peter Lynch pointed on on numerous occasions:

“If you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.”

(see also Peter Lynch video)

The good news is all the media pessimism and investor skepticism creates opportunities for shrewd investors focusing on key drivers of stock price appreciation (corporate earnings, interest rates, valuations, and sentiment).

While the eternally, half-glass full media is quick to highlight the negatives, it’s interesting that it takes an irrelevant, arbitrary level to finally create a positive headline for a new all-time record high of Dow 20,000. Frustratingly, the new all-time record highs reached by the Dow in 2013, 2014, 2015, and 2016 were almost completely ignored (see chart below):

Source: Barchart.com

What happens next? Nobody knows for certain. What is certain however is that using the breaking news headlines of Dow 20,000 to make critical investment decisions is not an intelligent long-term strategy. If you, like many investors, have difficulty in sticking to a long-term strategy, then find a trusted professional to help you create a systematic, disciplined investment strategy. Now, that is some real breaking news.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}