Posts filed under ‘Stocks’

The Art & Science of Successful Investing

As I described in my book, How I Managed $20,000,000,000.00 by Age 32, I believe successful investing is achieved by integrating aspects of both art and science. The science aspect of investing is fairly straightforward – most of the accounting and valuation math involved could be solved by a 7th grader. The more challenging aspect to successful investing is controlling the vacillating emotions of fear and greed when searching for attractive investments.

When people ask me about my investment philosophy, I do not like to be pigeon-holed into one style box because normally my portfolios hold investments that outsiders would deem both value and growth oriented. Since I am an absolute return investor, I am more concerned about how I can maximize upside returns while minimizing downside risk for my investors.

Because valuation is such an important factor in my process (price always matters), the most accurate description of my style would likely be “high octane GARP” (Growth At a Reasonable Price). While many GARP investors limit themselves to current or historical valuation metrics, my process has allowed me to take a more long-term, forward looking analysis of valuations, which has directed me to participate in some large winners, like Amazon (AMZN), Apple (AAPL), and Google/Alphabet (GOOGL), to name a few. To many observers, positions like these have traditionally been falsely considered “expensive” growth stocks.

Case in point is Google/Alphabet, which went public at $85 per share in 2004. At the time, the broad Wall Street consensus was the IPO (Initial Public Offering) price was way overheated. As it turned out, the stock has reached $1,000 per share and the Price-Earnings ratio (P/E) was a steal at less than 3x had you bought Google at the IPO price. ($85 2004 price/$33.98 2017 EPS estimate). Google is a perfect example of a dominant market leader that has been able to grow earnings dramatically for many years. In short order after going public, Google’s earnings ended up more than quintupling in less than three years and the stock price quintupled as well, proving that ill-advised focus on stale, traditional valuation metrics can lead you to wrong conclusions. Certainly, finding stocks that can increase in value by more than 11x fold is easier said than done, however, applying longer-term valuation metrics to dominant growth leading franchises will allow you to occasionally find monster winners like Google.

The greatest long-term winners don’t start off as the largest weightings, but due to the compounding of returns, position sizes can explode over time. As Peter Lynch states,

“You don’t need a lot of good hits every day. All you need is two to three good stocks a decade.”

Google/Alphabet proves what can appear expensive in the short-run is, in many cases, wildly cheap based on future earnings growth. Earnings tomorrow may be significantly larger than earnings today. Lynch emphasizes the importance of earnings over current prices,

“People concentrate too much on the ‘P’ (Price), but the ‘E’ (Earnings) really makes the difference.”

“Just because a stock is cheaper than before is no reason to buy it, and just because it’s more expensive is no reason to sell.”

The Google/Alphabet chart below shows the incredible price appreciation that can be realized from compounding earnings growth.

The Google example also underscores the importance of patience. Although the stock has been a massive home-run since its IPO, the stock barely budged from late 2006 through 2011. Accurately picking the perfect timing to make an investment is nearly impossible. I concur with Bill Miller when he stated,

“We expect the stocks we buy today to contribute to our performance several years hence. While it’s nice if they contribute to this year’s performance, this year’s performance should be driven by decisions we made in previous years. If we keep doing this, we hope that we will provide adequate returns in the future.”

Regarding timing, Miller adds,

“Nobody buys at lows and sells at highs except liars.”

The Sidoxia Philosophy

Over time, as I have fine-tuned my investment philosophy, I have not been bashful in borrowing winning ideas from growth gurus like Peter Lynch, Phil Fisher, William O’Neil, and Ron Baron, to name a few. By the same token, I am not shy about stealing ideas from value veterans like Warren Buffett, Seth Klarman, and Bill Miller as well.

While I don’t agree with Warren Buffett’s “forever” time horizon, I do believe in the power of compounding he espouses, which requires a longer-term investment horizon. The power of compounding is accelerated not only by committing to a long-term horizon, but also by the benefits accrued from lower trading costs and taxes. What’s more, taking a long view lowers your blood pressure and creates fewer ulcers. Legendary growth manager, T. Rowe Price, captures the essence of this idea here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

The Science of Investing

As discussed earlier, successful investing is an endeavor that involves the practices of both art and science – too much of either approach can be detrimental to your financial health. Quantitative screening can be an excellent tool for identifying new securities for research along with streamlining the fundamental analysis process. However, many investment funds rely too heavily on the quantitative science. The adage that “correlation does not equal causation” is an important credo to follow when reviewing various quantitative models (see Butter in Bangladesh).

The collapse of the infamous, multi-billion Long Term Capital Management hedge fund should also be a lesson to everyone (see When Genius Failed ). If world renowned Nobel Prize winners, Robert Merton and Myron Scholes, can single-handedly bring the global market to its knees as a result of using inconsistent and unreliable quantitative models, then I feel validated for my fundamentally-based investment approach.

While there are some artistic facets to valuation techniques, in large part, the valuation science is a fairly straightforward mathematical exercise. Unfortunately, the market consists of emotional and unpredictable individuals who continually change their opinions. Eventually the financial markets prod prices in the right direction, but over shorter time intervals, proper investment analysis requires some imperfect estimation.

Emotions regularly result in individuals overpaying for stocks, and this tendency is a risky strategy for any investment. In many cases investors chase darling stocks highlighted in news headlines, but regrettably these pricy investments often end up performing poorly. When it comes to hot stocks, I’m on the same page as famed value investor Bill Miller,

“If it’s in the papers, it’s in the price. One needs to anticipate, not react.”

Usually a news event that makes headlines is already factored into the stock price. The financial markets are generally forward looking mechanisms, not backward looking.

The Art of Investing

“It’s tough to make predictions, especially about the future.”

-Yogi Berra

Investing is undoubtedly a challenging undertaking, but like almost any profession, the more experience one has, the better results generally achieved. Experience alone does not guarantee extraordinary performance, in large part due to emotional pressures. Investing would be much easier for everyone, if you didn’t have to worry about controlling those pesky emotions of fear and greed. The best investment decisions, and frankly any decision, are rarely made under these heightened emotions.

The most successful set of investors I have studied and modeled my investment process after are professionals who have married the quantitative science with the fundamental art of investing. At Sidoxia, we use a disciplined cash flow based valuation approach, along with thorough fundamental analysis to identify attractively valued, market leading franchises that can sustain above average growth. It sounds like a mouthful, but over time, it has worked well for the benefit of my clients and me.

The market leading franchises we invest in tend to have a competitive advantage, whether in the form of superior research and development, low-cost manufacturing, leading marketing, and/or other exceptional functions in the company that allow the entity to consistently garner more growth and more market share from its competitors. Quality franchises tend to also employ first-class management teams that have a proven track record, along with thoughtful, systematic processes in place to maintain their competitive edge. These competitive advantages are what allow companies to produce exceptional earnings growth for extended periods of time, thereby producing outstanding long-term performance for shareholders.

Finding sustainable growth in competitive niche markets is nearly impossible, and that is why I center my attention on large or emerging sectors of the economy that can support long runways of growth. When analyzing companies with durable, long runways of earnings growth, I concentrate on those developing, share-taking companies and dominant market leaders. In other words, disruptive companies that are entering new markets with vast potential and established companies that are gaining significant share in large markets. Well-known growth authority, Phil Fisher summarized the objective,

“The greatest investment rewards come to those who by good luck or good sense find the occasional company that over the years can grow in sales and profits far more than industry as a whole.”

I am privileged and honored to manage the hard earned investments of my clients. If this was a simple profession, everyone would do it, and I would not be employed as an investment manager. I have developed what I believe is a superior way of managing money, but I realize my investment process is not the only way to make money. If you were to assemble 10 different investment managers in the same room, and ask them, “What is the best way to invest money?,” you are likely to get 10 different answers. Having been in the investment industry and managed money for over 25 years, my experience has shown me that the vast majority of professional managers have underperformed the passive benchmarks. However, there are investment managers who have survived the test of time. For those veterans incorporating a disciplined, systematic approach that integrates the artistic and scientific aspects of investing, exceptional long-term returns can be achieved and have been achieved.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AMZN, GOOG/GOOGL, and AAPL, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

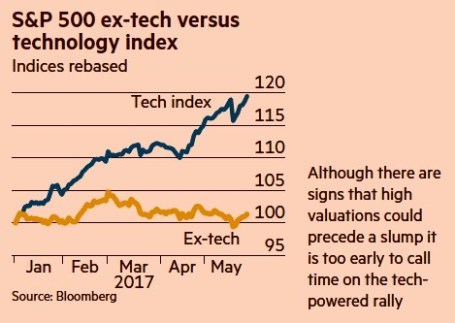

Investors Slowly Waking to Technology Tailwinds

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

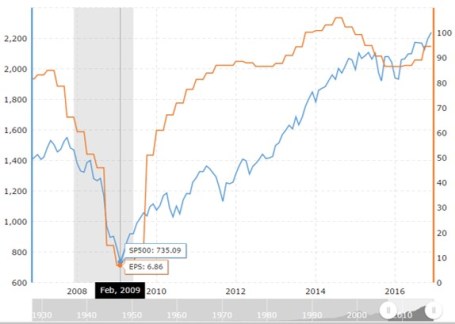

Profits

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

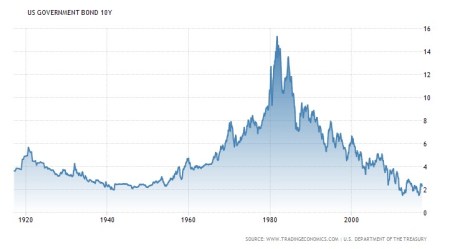

Interest Rates

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

No April Fool’s Joke – Another Record

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 3, 2017). Subscribe on the right side of the page for the complete text.

Having children is great, but a disadvantage to having younger kids are the April Fool’s jokes they like to play on parents. Fortunately, this year was fairly benign as I only suffered a nail-polish covered bar of soap in the shower. However, what has not been a joke has been the serious series of new record highs achieved in the stock market. While it is true the S&P 500 index finished roughly flat for the month (-0.0%) after hitting new highs earlier in March, the technology-laden NASDAQ index continued its dominating run, advancing +1.5% in March contributing to the impressive +10% jump in the first quarter. For 2017, the NASDAQ supremacy has been aided by the stalwart gains realized by leaders like Apple Inc. (up +24%), Facebook Inc. (up +23%), and Amazon.com Inc. (up +18%). The surprising fact to many is that these records have come in the face of immense political turmoil – most recently President Trump’s failure to deliver on a campaign promise to repeal and replace the Obamacare healthcare system.

Like a broken record, I’ve repeated there are much more important factors impacting investment portfolios and the stock market other than politics (see also Politics Schmolitics). In fact, many casual observers of the stock market don’t realize we have been in the midst of a synchronized, global economic expansion, helped in part by the stabilization in the value of the U.S. dollar over the last couple of years.

Source: Investing.com

As you can see above, there was an approximate +25% appreciation in the value of the dollar in late-2014, early-2015. This spike in the value of the dollar suddenly made U.S. goods sold abroad +25% more expensive, resulting in U.S. multinational companies experiencing a dramatic profitability squeeze over a short period of time. The good news is that over the last two years the dollar has stabilized around an index value of 100. What does this mean? In short, this has provided U.S. multinational companies time to adjust operations, thereby neutralizing the currency headwinds and allowing the companies to return to profitability growth.

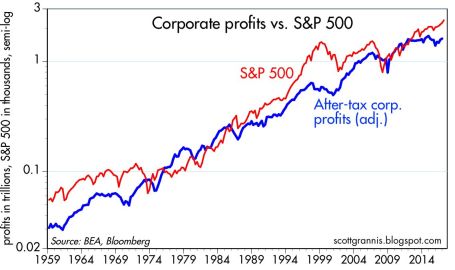

Source: Calafia Beach Pundit

And profits are back on the rise indeed. The six decade long chart above shows there is a significant correlation between the stock market (red line – S&P 500) and corporate profits (blue line). The skeptics and naysayers have been out in full force ever since the 2008-2009 financial crisis – I profiled these so-called “sideliners” in Get out of Stocks!.

As the stock market continues to hit new record highs, the doubters continue to scream danger. There will always be volatility, but when the richest investor of all-time, Warren Buffett, continues to say that stocks are still attractively priced, given the current interest rate environment, that goes a long way to assuage investor concerns.

Politically, a lot could still go wrong as it relates to healthcare, tax reform, and infrastructure spending, to name a few issues. However, it’s still early, and it’s possible positive surprises could also occur. More importantly, as I’ve noted before, corporate profits, interest rates, valuations, and investor sentiment are much more important factors than politics, and on balance these factors are on the favorable side of the ledger. These factors will have a larger impact on the long-term direction of stock prices.

With approval ratings of Congress and the President at low levels, investors have had trouble finding humor in politics, even on April Fool’s Day. Another significant factor more important than politics is the issue of retirement savings by Americans, which is no joke. As you finalize your tax returns in the coming weeks, it behooves you to revisit your retirement plan and investment portfolio. Inefficiently investing your money or outliving your savings is no laughing matter. I’ll continue with my disciplined financial plan and leave the laughing to my kids, as they enjoy planning their next April Fool’s Day prank.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, FB, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Munger: Buffett’s Wingman & the Art of Stock Picking

Simon had Garfunkel, Batman had Robin, Hall had Oates, Dr. Evil had Mini Me, Sonny had Cher, and Malone had Stockton. In the investing world, Buffett has Munger. Charlie Munger is one of the most successful and famous wingmen of all-time – evidenced by Berkshire Hathaway Corporation’s (BRKA/B) outperformance of the S&P 500 index by approximately +624% from 1977 – 2009, according to MarketWatch. Munger not only provides critical insights to his legendary billionaire boss, Warren Buffett, but he was also Chairman of Berkshire’s insurance subsidiary, Wesco Financial Corporation from 1984 until 2011. The magic of this dynamic duo began when they met at a dinner party 58 years ago (1959).

In an article he published in 2006, the magnificent Munger describes the “Art of Stock Picking” in a thorough review about the secrets of equity investing. We’ll now explore some of the 93-year-old’s sage advice and wisdom.

Model Building

Charlie Munger believes an individual needs a solid general education before becoming a successful investor, and in order to do that one needs to study and understand multiple “models.”

“You’ve got to have models in your head. And you’ve got to array your experience both vicarious and direct on this latticework of models. You may have noticed students who just try to remember and pound back what is remembered. Well, they fail in school and in life. You’ve got to hang experience on a latticework of models in your head.”

Although Munger indicates there are 80 or 90 important models, the examples he provides include mathematics, accounting, biology, physiology, psychology, and microeconomics.

Advantages of Scale

Great businesses in many cases enjoy the benefits of scale, and Munger devotes a good amount of time to this subject. Scale advantages can be realized through advertising, information, psychological “social proofing,” and structural factors.

The newspaper industry is an example of a structural scale business in which a “winner takes all” phenomenon applies. Munger aptly points out, “There’s practically no city left in the U.S., aside from a few very big ones, where there’s more than one daily newspaper.”

General Electric Co. (GE) is another example of a company that uses scale to its advantage. Jack Welch, the former General Electric CEO, learned an early lesson. If the GE division is not large enough to be a leader in a particular industry, then they should exit. Or as Welch put it, “To hell with it. We’re either going to be # 1 or #2 in every field we’re in or we’re going to be out. I don’t care how many people I have to fire and what I have to sell. We’re going to be #1 or #2 or out.”

Bigger Not Always Better

Scale comes with its advantages, but if not managed correctly, size can weigh on a company like an anchor. Munger highlights the tendency of large corporations to become “big, fat, dumb, unmotivated bureaucracies.” An implicit corruption also leads to “layers of management and associated costs that nobody needs. Then, while people are justifying all these layers, it takes forever to get anything done. They’re too slow to make decisions and nimbler people run circles around them.”

Becoming too large can also create group-think, or what Munger calls “Pavlovian Association.” Munger goes onto add, “If people tell you what you really don’t want to hear what’s unpleasant there’s an almost automatic reaction of antipathy…You can get severe malfunction in the high ranks of business. And of course, if you’re investing, it can make a lot of difference.”

Technology: Benefit or Burden?

Munger recognizes that technology lowers costs for companies, but the important question that many managers fail to ask themselves is whether the benefits from technology investments accrue to the company or to the customer? Munger summed it up here:

“There are all kinds of wonderful new inventions that give you nothing as owners except the opportunity to spend a lot more money in a business that’s still going to be lousy. The money still won’t come to you. All of the advantages from great improvements are going to flow through to the customers.”

Buffett and Munger realized this lesson early on when productivity improvements gained from technology investments in the textile business all went to the buyers.

Surfing the Wave

When looking for good businesses, Munger and Buffett are looking to “surf” waves or trends that will generate healthy returns for an extended period of time. “When a surfer gets up and catches the wave and just stays there, he can go a long, long time. But if he gets off the wave, he becomes mired in shallows,” states Munger. He notes that it’s the “early bird,” or company that identifies a big trend before others that enjoys the spoils. Examples Munger uses to illustrate this point are Microsoft Corp. (MSFT), Intel Corp. (INTC), and National Cash Register from the old days.

Large profits will be collected by those investors that can identify and surf those rare large waves. Unfortunately, taking advantage of these rare circumstances becomes tougher and tougher for larger investors like Berkshire. If you’re an elephant trying to surf a wave, you need to find larger and larger waves, and even then, due to your size, you will be unable to surf as long as small investors.

Circle of Competence

Circle of competence is not a new subject discussed by Buffett and Munger, but it is always worth reviewing. Here’s how Munger describes the concept:

“You have to figure out what your own aptitudes are. If you play games where other people have the aptitudes and you don’t, you’re going to lose. And that’s as close to certain as any prediction that you can make. You have to figure out where you’ve got an edge. And you’ve got to play within your own circle of competence.”

For Munger and Buffett, sticking to their circle of competence means staying away from high-technology companies, although more recently they have expanded this view to include International Business Machines (IBM), which they are now a large investor.

Market Efficiency or Lack Thereof

Munger acknowledges that financial markets are quite difficult to beat. Since the markets are “partly efficient and partly inefficient,” he believes there is a minority of individuals who can outperform the markets. To expand on this idea, he compares stock investing to the pari-mutuel system at the racetrack, which despite the odds stacked against the bettor (17% in fees going to the racetrack), there are a few individuals who can still make decent money.

The transactional costs are much lower for stocks, but success for an investor still requires discipline and patience. As Munger declares, “The way to win is to work, work, work, work and hope to have a few insights.”

Winning the Game – 10 Insights / 20 Punches

As the previous section implies, outperformance requires patience and a discriminating eye, which has allowed Berkshire to create the bulk of its wealth from a relatively small number of investment insights. Here’s Munger’s explanation on this matter:

“How many insights do you need? Well, I’d argue: that you don’t need many in a lifetime. If you look at Berkshire Hathaway and all of its accumulated billions, the top ten insights account for most of it….I don’t mean to say that [Warren] only had ten insights. I’m just saying, that most of the money came from ten insights.”

Chasing performance, trading too much, being too timid, and paying too high a price are not recipes for success. Independent thought accompanied with selective, bold decisions is the way to go. Munger’s solution to these problems is to provide investors with a Buffett 20-punch ticket:

“I could improve your ultimate financial welfare by giving you a ticket with only 20 slots in it so that you had 20 punches ‑ representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all.”

The great thing about Munger and Buffett’s advice is that it is digestible by the masses. Like dieting, investing can be very simple to understand, but difficult to execute, and legends like these always remind us of the important investing basics. Even though Charlie Munger may be slowing down a tad at 93-years-old, Warren Buffett and investors everywhere are blessed to have this wingman around spreading his knowledge about investing and the art of stock picking.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, BRKA/B, GE, MSFT, INTC, IBM but at the time of this 3/12/17 updated publishing, SCM had no direct position in National Cash Register, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

March Madness or Retirement Sadness?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2017). Subscribe on the right side of the page for the complete text.

“March Madness” begins in a few weeks with a start of the 68-team NCAA college basketball tournament, but there has also been plenty of other economic and political madness going on in the background. As it relates to the stock market, the Dow Jones Industrial Average index reached a new, all-time record high last month, exceeding the psychologically prominent level of 20,000 (closing the month at 20,812). For the month, the Dow rose an impressive +4.8%, and since November’s presidential election it catapulted an even more remarkable +13.5%.

Despite our 45th president just completing his first State of the Union address to the nation, American voters remain sharply divided across political lines, and that bias is not likely to change any time soon. Fortunately, as I’ve written on numerous occasions (see Politics & Your Money), politics have no long-term impact on your finances and retirement. Sure, in the short-run, legislative policies can create winners and losers across particular companies and industries, but history is firmly on your side if you consider the positive track record of stocks over the last couple of centuries. As the chart below demonstrates, over the last 150 years or so, stock performance is roughly the same across parties (up +11% annually), whether you identify with a red elephant or a blue donkey.

Nevertheless, political rants flooding our Facebook news feeds can confuse investors and scare people into inaction. Pervasive fake news stories regarding the supposed policy benefits and shortcomings of immigration, tax reform, terrorism, entitlements, foreign policy, and economic issues often result in heightened misperception and anxiety.

More important than reading Facebook political rants, watching March Madness basketball, or drinking green beer on St. Patrick’s Day, is saving money for retirement. While some of these diversions can be temporarily satisfying and entertaining, lost in the daily shuffle is the retirement epidemic quietly lurking in the background. Managing money makes people nervous even though it is an essential part of life. Retirement planning is critical because a mountain of the 76 million Baby Boomers born between 1946 – 1964 have already reached retirement age and are not ready (see chart below).

The critical problem is most Americans are ill-prepared financially for retirement, and many of them run the risk of outliving their savings. A recent study conducted by the Economic Policy Institute (EPI) shows that nearly half of families have no retirement account savings at all. The findings go on to highlight that the median U.S. family only has $5,000 in savings (see also Getting to Your Number). Even after considering my tight-fisted habits, that kind of money wouldn’t be enough cash for me to survive on.

Saving and investing have never been more important. It doesn’t take a genius to understand that government entitlements like Social Security and Medicare are at risk for millions of Americans. While I am definitely not sounding the alarm for current retirees who have secure benefits, there are millions of others whose retirement benefits are in jeopardy.

Missing the 20,000 Point Boat? Dow 100,000

Making matters worse, saving and investing has never been more challenging. If you thought handling all of life’s responsibilities was tough enough already, try the impossible task of interpreting the avalanche of instantaneous political and economic headlines pouring over our electronic devices at lighting speed.

Knee-jerk reactions to headlines might give investors a false sense of security, but the near-impossibility of consistently timing the stock market has not stopped people from attempting to do so. For example, recently I have been bombarded with the same question, “Wade, don’t you think the stock market is overpriced now that we have eclipsed 20,000?” The short answer is “no,” given the current factors (see Don’t Be a Fool). Thankfully, I’m not alone in this response. Warren Buffett, the wealthiest billionaire investor on the planet, answered the same question this week after investing $20,000,000,000 more in stocks post the election:

“People talk about 20,000 being high. Well, I remember when it hit 200 and that was supposedly high….You know, you’re going to see a Dow [in your lifetime] that certainly approaches 100,000 and that doesn’t require any miracles, that just requires the American system continuing to function pretty much as it has.”

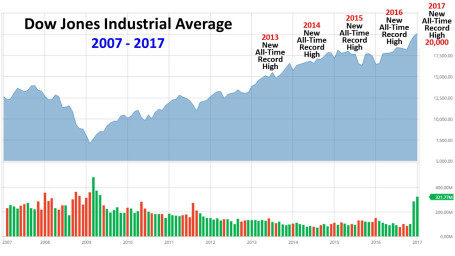

Like a deer in headlights, many Americans have been scared into complacency. To their detriment, many savers have sat silently on the sidelines earning near-0% returns on their savings, while the stock market has reached new all-time record highs. While Dow 20,000 might be new news for some, the reality is new all-time record highs have repeatedly been achieved in 2013, 2014, 2015, 2016, and now 2017 (see chart below).

While I am not advocating for all people to throw their entire savings into stocks, it is vitally important for individuals to construct diversified portfolios across a wide range of asset classes, subject to each person’s unique objectives, constraints, risk tolerance, and time horizon. The risk of outliving your savings is real, so if you need assistance, seek out an experienced professional. March Madness may be here, but don’t get distracted. Make investing a priority, so your daily madness doesn’t turn into retirement sadness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Re-Questioning the Death of Buy & Hold Investing

Article originally posted September 17, 2010: At the time this original article was written, the Dow Jones Industrial Average was hovering around 11,500. Last week, the Dow closed at 20,624. Sure there have been plenty of ups and downs since 2010, but as I suggested seven years ago, perhaps “buy and hold” still is not dead today?

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements arre obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty-year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly, there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: At the time the article was originally written, Sidoxia Capital Management (SCM) and some of its clients owned certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. As of 2/19/17 – Sidoxia owned AAPL, AMZN, and was short NFLX. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Super Bowl Blitz – Dow 20,000

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 3, 2017). Subscribe on the right side of the page for the complete text.

If you have been following the sports headlines, then you know the Super Bowl 51 NFL football championship game between the four-time champion New England Patriots and the zero-time champion Atlanta Falcons is upon us. It’s that time of the year when more than 100 million people will congregate in front of big screen TVs across our nation and stare at ludicrous commercials (costing $5 million each); watch a semi-entertaining halftime show; and gorge on thousands of calories until stomachs bloat painfully.

The other headlines blasting across the media airwaves relate to the new all-time record milestone of 20,000 achieved by the Dow Jones Industrials Average (a.k.a., “The Dow”). For those people who are not glued to CNBC business television all day, the Dow is a basket of 30 large company stocks subjectively selected by the editors of the Wall Street Journal with the intent of creating an index that can mimic the overall economy. A lot of dynamics in our economy have transformed over the Dow’s 132 year history (1885), so it should come as no surprise that the index’s stock components have changed 51 times since 1896 – the most recent change occurred in March 2015 when Apple Inc. (AAPL) was added to the Dow and AT&T Inc. (T) was dropped.

20,000 Big Deal?

The last time the Dow closed above 10,000 was on March 29, 1999, so it has taken almost 18 years to double to 20,000. Is the Dow reaching the 20,000 landmark level a big deal in the whole scheme of things? The short answer is “No”. It is true the Dow can act as a fairly good barometer of the economy over longer periods of time. Over the 1998 – 2017 timeframe, economic activity has almost doubled to about $18 trillion (as measured by Gross Domestic Product – GDP) with the added help of a declining interest rate tailwind.

In the short-run, stock indexes like the Dow have a spottier record in correlating with economic variables. At the root of short-term stock price distortions are human behavioral biases and emotions, such as fear and greed. Investor panic and euphoria ultimately have a way of causing wild stock price overreactions, which in turn leads to poor decisions and results. We saw this firsthand during the inflation and subsequent bursting of the 2000 technology bubble. If that volatility wasn’t painful enough, last decade’s housing collapse, which resulted in the 2008-2009 financial crisis, is a constant reminder of how extreme emotions can lead to poor decision-making. For professionals, short-term volatility and overreactions provide lucrative opportunities, but casual investors and novices left to their own devices generally destroy wealth.

As I have discussed on my Investing Caffeine blog on numerous occasions, the march towards 20,000 occurred in the middle of arguably the most hated bull market in a generation or two (see The Most Hated Bull Market). It wasn’t until recently that the media began fixating on this arbitrary new all-time record high of 20,000. My frustration with the coverage is that the impressive phenomenon of this multi-year bull market advance has been largely ignored, in favor of gloom and doom, which sells more advertising – Madison Avenue execs enthusiastically say, “Thank you.” While the media hypes these stock records as new, this phenomenon is actually old news. In fact, stocks have been hitting new highs over the last five years (see chart below).

More specifically, the Dow has hit consecutive, new all-time record highs in each year since 2013. This ignored bull market (see Gallup survey) may not be good for the investment industry, but it can be good for shrewd long-term investors, who react patiently and opportunistically.

Political Football

In Washington, there’s a different game currently going on, and it’s a game of political football. With a hotly contentious 2016 election still fresh in the minds of many voters, a subset of unsatisfied Americans are closely scrutinizing every move of the new administration. Love him or hate him, it is difficult for observers to accuse President Trump of sitting on his hands. In the first 11 days of his presidential term alone, Trump has been very active in enacting almost 20 Executive Orders and Memoranda (see the definitional difference here), as he tries to make supporters whole with his many previous campaign trail promises. The persistently increasing number of policies is rising by the day (…and tweet), and here’s a summarizing list of Trump’s executive actions so far:

- Refugee Travel Ban

- Keystone & Dakota Pipelines

- Border Wall

- Deportations/Sanctuary Cities

- Manufacturing Regulation Relief

- American Steel

- Environmental Reviews

- Affordable Care Act Requirements

- Border Wall

- Exit TPP Trade Deal

- Federal Hiring Freeze

- Federal Abortion Freeze

- Regulation Freeze

- Military Review

- ISIS Fight Plan

- Reorganization of Security Councils

- Lobbyist Bans

- Deregulation for Small Businesses

President Trump has thrown another political football bomb with his recent nomination of Judge Neil Gorsuch (age 49) to the Supreme Court in the hopes that no penalty flags will be thrown by the opposition. Gorsuch, the youngest nominee in 25 years, is a conservative federal appeals judge from Colorado who is looking to fill the seat left open by last year’s death of Justice Antonin Scalia at the age 79.

Politics – Schmolitics

When it comes to the stock market and the economy, many people like to make the president the hero or the scapegoat. Like a quarterback on the football field, the president certainly has influence in shaping the political and economic game plan, but he is not the only player. There is an infinite number of other factors that can (and do) contribute to our country’s success (or lack thereof).

Those economic game-changing factors include, but are not limited to: Congress, the Federal Reserve, Supreme Court, consumer sentiment, trade policy, demographics, regulations, tax policy, business confidence, interest rates, technology proliferation, inflation, capital investment, geopolitics, terrorism, environmental disruptions, immigration, rate of productivity, fiscal policy, foreign relations, sanctions, entitlements, debt levels, bank lending, mergers and acquisitions, labor rules, IPOs (Initial Public Offerings), stock buybacks, foreign exchange rates, local/state/national elections, and many, many, many other factors.

Regardless to which political team you affiliate, if you periodically flip through your social media stream (e.g., Facebook), or turn on the nightly news, you too have likely suffered some sort of political fatigue injury. As Winston Churchill famously stated, “Democracy is the worst form of government except for all the other forms that have been tried from time to time.”

When it comes to your finances, getting excited over Dow 20,000 or despondent over politics is not a useful or efficient strategy. Rather than becoming emotionally volatile, you will be better off by focusing on building (or executing) your long-term investment plan. Not much can be accomplished by yelling at a political charged Facebook rant or screaming at your TV during a football game, so why not calmly concentrate on ways to control your future (financial or otherwise). Actions, not fear, get results. Therefore, if this Super Bowl Sunday you’re not ready to review your asset allocation, budget your annual expenses, or contemplate your investment time horizon, then at least take control of your future by managing some nacho cheese dip and handling plenty of fried chicken.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, T, FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Wiping Your Financial Slate Clean

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 3, 2017). Subscribe on the right side of the page for the complete text.

The page on the calendar has turned, and we now have a new year, and will shortly have a new president, and new economic policies. Although there is nothing magical about starting a fresh, new year, the annual rites of passage also allow investors to start with a clean slate again and reflect on their personal financial situation. Before you reach a desired destination (i.e., retirement), it is always helpful to know where you have been and where are you currently. Achieving this goal requires filtering through a never-ending avalanche of real-time data flooding through our cell phones, computers, TVs, radios, and Facebook accounts. This may seem like a daunting challenge, but that’s where I come in!

Distinguishing the signals from the noise is tough and there was plenty of noise in 2016 – just like there is every year. Before the S&P 500 stock index registered a +9.5% return in 2016, fears of a China slowdown blanketed headlines last January (the S&P 500 fell -15% from its highs and small cap stocks dropped -26%), and the Brexit (British exit) referendum caused a brief 48-hour -6% hiccup in June. Oil was also in the news as prices hit a low of $26 a barrel early in the year, before more than doubling by year-end to $54 per barrel (still well below the high exceeding $100 in 2014). On the interest rate front, 10-Year Treasury rates bottomed at 1.34% in July, while trillions of dollars in global bonds were incomprehensibly paying negative interest rates. However, fears of inflation rocked bond prices lower (prices move inversely to yields) and pushed bond yields up to 2.45% today. Along these lines, the Federal Reserve has turned the tide on its near-0% interest rate policy as evidenced by its second rate hike in December.

Despite the abbreviated volatility caused by the aforementioned factors, it was the U.S. elections and surprise victory of President-elect Donald Trump that dominated the media airwaves for most of 2016, and is likely to continue as we enter 2017. In hindsight, the amazing Twitter-led, Trump triumph was confirmation of the sweeping global populism trend that has also replaced establishment leaders in the U.K., France, and Italy. There are many explanations for the pervasive rise in populism, but meager global economic growth, globalization, and automation via technology are all contributing factors.

The Trump Bump

Even though Trump has yet to accept the oath of Commander-in-Chief, recent investor optimism has been fueled by expectations of a Republican president passing numerous pro-growth policies and legislation through a Republican majority-controlled Congress. Here are some of the expected changes:

- Corporate/individual tax cuts and reform

- Healthcare reform (i.e., Obamacare)

- Proposed $1 trillion in infrastructure spending

- Repatriation tax holiday for multinational corporate profits

- Regulatory relief (e.g., Dodd-Frank banking and EPA environmental reform)

The chart below summarizes the major events of 2016, including the year-end “Trump Bump”:

While I too remain optimistic, I understand there is no free lunch as it relates to financial markets (see also Half Trump Full). While tax cuts, infrastructure spending, and regulatory relief should positively contribute to economic growth, these benefits will have to be weighed against the likely costs of higher inflation, debt, and deficits.

Over the 25+ years I have been investing, the nature of the stock market and economy hasn’t changed. The emotions of fear and greed rule the day just as much today as they did a century ago. What has changed today is the pace, quality, and sheer volume of news. In the end, my experience has taught me that 99% of what you read, see or hear at the office is irrelevant as it relates to your retirement and investments. What ultimately drives asset prices higher or lower are the four key factors of corporate profits, interest rates, valuations, and sentiment (contrarian indicator) . As you can see from the chart below, corporate profits are at record levels and forecast to accelerate in 2017 (up +11.9%). In addition, valuations remain very reasonable, given how low interest rates are (albeit less low), and skeptical investor sentiment augurs well in the short-run.

Source: FactSet

Regardless of your economic or political views, this year is bound to have plenty of ups and downs, as is always the case. With a clean slate and fresh turn to the calendar, now is a perfect time to organize your finances and position yourself for a better retirement and 2017.

Wade W. Slome, CFA, CFP®

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Searching for the Growth Stock Holy Grail

Remember Research in Motion (now Blackberry Limited – BBRY)? What about Krispy Kreme Doughnuts? How about Crocs (CROX)? Or maybe even Webvan, the online grocery delivery company that went bankrupt during the bursting of the dot-com bubble? These are all examples of once heralded growth companies that lost their mojo along their growth expansion ways.

Not every stock can grow to the $80+ billion market cap stratosphere like Apple Inc. (AAPL), Starbucks Corp. (SBUX), and Wal-Mart Stores (WMT), so finding companies with the right mixture of growth characteristics can be challenging. Objective stock market observers can disagree on the ingredients of a successful growth stock recipe, but generally speaking, the real explosive appreciation in stock prices come from those companies that can compound earnings growth over longer periods of time.

But how can one discover the Holy Grail of compounding earnings? At Sidoxia Capital Management, there are a handful of key factors we look for in successful growth companies. In the hyper-competitive global marketplace, these are crucial questions we want adequately answered before we invest our clients’ money:

- Does the company sell a product or service that cuts costs?

- Does the company offer a product or service with unique entertainment value?

- Does the company offer a superior product or service compared to its competitors?

Even if a target investment can affirmatively answer two or three of these questions, often the most important question is the following:

- Does the company have a sustainable competitive advantage in providing a product or service?

If the company does not have some type of durable competitive advantage, then some other company can just copy the product or service, and sell it at a lower price. This sadly leads to margin and P/E (Price-Earnings) multiple compression – both negative outcomes.

The aforementioned factors are not the end-all, be-all for successful growth stocks, but rather the minimum price of admission. Even if the previous criteria boxes are sufficiently checked off, the company being researched must still be fairly or attractively priced. For example, it doesn’t take a genius to figure out Apple is a successful company with unique advantages. More specifically, the company has $240 billion in cash, $50 billion in profits, and $215 billion in revenue. The real question becomes, is the stock fairly or attractively priced?

Although Apple appears attractively valued at current prices, in many other instances that is not the case. Often, great companies have been discovered by a large swath of investors, and therefore trade at significant premiums, which increases the risk profile or reduces the upside potential of the investment.

Sucking the Last Puff

If a company’s product or service isn’t superior, cut costs, or entertain at a reasonable/attractive valuation, then investing is like taking the last puff or drag out of a cigarette butt. Some value investors are good at this craft, but often these managers get caught into so-called “value traps” – ask Bill Ackman about Valeant Pharmaceuticals (VRX). Many value investors thought they found a bargain when they bought Valeant shares after it fell -80% in price. The stock subsequently has fallen another -50%…ouch!.

It’s worth noting that growth can come from many different areas. Even mature industries can produce periods of cyclical growth, however identifying cyclical winners is challenging. The art for the investment manager is determining whether growth in a target investment is sustainable. In many instances, companies temporarily benefit from a rising tide that lifts all boats, before the tide goes out and sinks fundamentals down to lower levels.

Growth investing can be a dangerous hobby for short-term traders because the price volatility stemming from ever-changing earnings growth expectations creates excessive trading, taxes, and transaction costs. However, for long-term investors, the great growth manager, T. Rowe Price, summed it up best here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

Growth investing is both a science and an art, but does not require a degree in rocket science. If you can focus on the important growth criteria, and combine it with a long-term disciplined valuation process, you will be well on your way to discovering the growth stock Holy Grail.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in VRX, BBRY, SBUX, WMT, CROX, Krispy Kreme, Webvan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}