Posts filed under ‘International’

Solving Europe and Your Deadbeat Cousin

The fall holidays are quickly approaching, and almost every family has at least one black-sheep member among the bunch. You know, the unemployed second cousin who shows up for Thanksgiving dinner intoxicated – who then proceeds to pull you aside after a full meal to ask you for some money because of an unlucky trip to Las Vegas. For simplicity purposes, let’s name our deadbeat cousin Joe.

Right now the European union (EU) is dealing with a similar situation, but rather than being forced to deal with money-begging cousin named Joe, the EU is being forced to confront the irresponsible debt-binging practices of its own relatives – the PIIGS (Portugal, Ireland, Italy, Greece, and Spain). The European troika (International Monetary Fund/IMF; European Union/EU; and European Central Bank/ECB), spearheaded by German and French persuasion, is contemplating everything from prescribing direct bank recapitalization, bailouts via the leveraging of the EFSF (European Financial Stability Facility), ECB bond purchases, debt guarantees, unlimited central bank loans, and more.

New stress tests are being reevaluated as we speak. Previous tests failed in gaining the necessary credibility because inadequate haircuts were applied to the values of PIIGS debt held by European banks. European Leaders are beginning to gain some religion as to the urgency and intensity of the financial crisis. Just today, Germany’s chancellor (Angela Merkel) and France’s President (Nicolas Sarkozy) announced that they will introduce a comprehensive package of measures to stabilize the eurozone by the end of this month, right before the summit of the G20 leading global economies in Cannes, France.

Pick Your Poison

Whatever the path used to mop up debt excesses, the options for solving the financial mess can be lumped together in the following categories:

1. Austerity: Plain, unadulterated spending cuts is one prescription being administerd in hopes of curing bloated European sovereign debt issues. Negatives: Slowing economic growth, slowing tax receipts, potentially widening deficits (reference Greece), and political reelection self interests call into question the feasibility of the austerity option. Positives: Austerity is a morally correct fiscal response, which has the potential of placing a country’s financial situation back on a sustainable path.

2. Bailouts: The troika is also talking about infusing the troubled banks with new capital. Negatives: This action could result in more debt placed on country balance sheets, a potentially lower credit rating, higher costs of borrowing, higher tax burden for blameless taxpayers, and often an impossible political path of success. Positives: Financial markets may respond constructively in the short-run, but providing an alcoholic more alcohol doesn’t solve long-term fiscal responsibility, and also introduces the problem of moral hazard.

3. Haircuts: Voluntary or involuntary haircuts to principal debt obligations may occur in conjunction with previously described bailout efforts, depending on the severity of debt levels. Negatives: There are many different sets of constituents and investors, which can make voluntary haircut/debt restructuring terms difficult to agree upon. If the haircuts are too severe, banking reserves across the EU will become decimated, which will only lead to more austerity, bailouts, and potential credit downgrades. Such actions could hamper or eliminated future access to capital, and the cost of access to future capital could be cost prohibitive for the borrowing countries that defaulted/restructured. Positives: Haircuts eliminate or lessen the need for other more painful austerity or restructuring measures, and force borrowers to become more fiscally responsible, not to mention, investors are forced to conduct more thorough due diligence.

4. Printing Press: Buying back debt with freshly printed euros hot off the press is another strategy. Negatives: Inflation is an invisible tax on everyone, including those constituents who are behaving in a fiscally responsible manner. Positives: Not only is this strategy more politically palatable because the inflation tax is spread across the whole union, but this path to debt reduction also does not require as painful and unpopular cuts in spending as experienced in other options.

The Costs

What is the cost for this massive European debt-binging rehabilitation? Estimates vary widely, but a JP Morgan analyst sized it up this way as explained in the The Financial Times:

“In a worst-case, severe recession scenario, €230bn in new capital is needed to meet Basel III requirements, assuming a 60 per cent debt writedown on Greece, 40 per cent on Ireland and Portugal and 20 per cent on Italy and Spain, and that banks withhold dividends.”

More bearish estimates with larger bond loss haircuts, stricter regulatory guidelines, and harsher austerity measures have generated recapitalization numbers north of €1 trillion euros. Regardless of the estimates, European governments, regulators, and central banks are likely to select a combination of the poisons listed above. There is no silver bullet solution, and any of the chosen paths come with their own unique set of consequences.

As time passes and the European crisis matures, I am confident that you will be hearing more about ECB involvement and the firing-up of the printing presses. Perhaps the ECB will fund and work jointly with the EFSF to soak up debt and/or capitalize weak banks. Alternatively, and more simply, the ECB is likely to follow the path of the U.S. and implement significant amounts of quantitative easing (i.e., provide liquidity to the financial system via sovereign debt purchases and guarantees).

Dealing with irresponsible and intoxicated deadbeat second cousins (or European countries) fishing for money is never a pleasurable experience. There are many ways to address the problem, but ignoring the issue will only make the situation worse. Fortunately, our European friends on the other side of the pond appear to be taking notice. As in the U.S., if government officials delay or ignore the immediate problems, the financial market cops (a.k.a., “bond vigilantes”) will force them into action. In the recent past, European officials have used a strategy of sober talking “tough love,” but signs that the ECB printing presses are now beginning to warm up are evident. Once the euros come flying off the presses to detoxify the debt binging banks, perhaps the ECB can print a few extra euros for my cousin Joe.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Economic Tug-of-War as Recovery Matures

Excerpt from No-Cost June 2011 Sidoxia Monthly Newsletter (Subscribe on right-side of page)

With the Rapture behind us, we can now focus less on the end of the world and more on the economic tug of war. As we approach the midpoint of 2011, equity markets were down -1.4% last month (S&P 500 index) and are virtually flat since February – trading within a narrow band of approximately +/- 5% over that period. Investors are filtering through data as we speak, reconciling record corporate profits and margins with decelerating economic and employment trends.

Here are some of the issues investors are digesting:

Profits Continue Chugging Along: There are many crosscurrents swirling around the economy, but corporations are sitting on fat profits and growing cash piles owing success to several factors:

Profits Continue Chugging Along: There are many crosscurrents swirling around the economy, but corporations are sitting on fat profits and growing cash piles owing success to several factors:

- International Expansion: A weaker dollar has made domestic goods and services more affordable to foreigners, resulting in stronger sales abroad. The expansion of middle classes in developing countries is leading to the broader purchasing power necessary to drive increasing American exports.

- Rising Productivity: Cheap labor, new equipment, and expanded technology adoption have resulted in annualized productivity increases of +2.9% and +1.6% in the 4th quarter and 1st quarter, respectively. Eventually, corporations will be forced to hire full-time employees in bulk, as bursting temporary worker staffs and stretched employee bases will hit output limitations.

- Deleveraging Helps Spending: As we enter the third year of the economic recovery, consumers, corporations, and financial institutions have become more responsible in curtailing their debt loads, which has led to more sustainable, albeit more moderate, spending levels. For instance, ever since mid-2008, when recessionary fundamentals worsened, consumer debt in the U.S. has fallen by more than $1 trillion.

![]() Fed Running on Empty: The QE2 (Quantitative Easing Part II) government security purchase program, designed to stimulate the economy by driving interest rates lower, is concluding at the end of this month. If the economy continues to stagnate, there’s a possibility that the tank may need to be re-filled with some QE3? Maintaining the 30-year fixed rate mortgage currently around 4.25%, and the 10-year Treasury note yielding around 3.05% will be a challenge after the program expires. Time will tell…

Fed Running on Empty: The QE2 (Quantitative Easing Part II) government security purchase program, designed to stimulate the economy by driving interest rates lower, is concluding at the end of this month. If the economy continues to stagnate, there’s a possibility that the tank may need to be re-filled with some QE3? Maintaining the 30-year fixed rate mortgage currently around 4.25%, and the 10-year Treasury note yielding around 3.05% will be a challenge after the program expires. Time will tell…

Slogging Through Mud: Although corporate profits are expanding smartly, economic momentum, as measured by real Gross Domestic Product (GDP) growth, is struggling like a vehicle spinning its wheels in mud. Annualized first quarter GDP growth registered in at a meager +1.8% as the economy weans itself off of fiscal stimulus and adjusts to more normalized spending levels. An elevated 9% unemployment rate and continued weak housing market is also putting a lid on consumer spending. Offsetting the negative impacts of the stimulative spending declines have been the increasing tax receipts achieved as a consequence of seven consecutive quarters of GDP growth.

Slogging Through Mud: Although corporate profits are expanding smartly, economic momentum, as measured by real Gross Domestic Product (GDP) growth, is struggling like a vehicle spinning its wheels in mud. Annualized first quarter GDP growth registered in at a meager +1.8% as the economy weans itself off of fiscal stimulus and adjusts to more normalized spending levels. An elevated 9% unemployment rate and continued weak housing market is also putting a lid on consumer spending. Offsetting the negative impacts of the stimulative spending declines have been the increasing tax receipts achieved as a consequence of seven consecutive quarters of GDP growth.

Mixed Bag – Euro Confusion: Germany reported eye-popping first quarter GDP growth of +5.2%, the steepest year-over-year rise since reunification in 1990, yet lingering fiscal concerns surrounding the likes of Greece, Portugal, and Italy have intensified. Fitch, for example, recently cut its rating on Greece’s long-term sovereign debt three notches, from BB+ to B+ plus, and placed the country on “rating watch negative” status. These fears have pushed up two-year Greek bond yields to over 26%. Regarding the other countries mentioned, Standard & Poor’s, another credit rating agency, cut Italy’s A+ rating, while the European Union and International Monetary Fund agreed on a $116 billion bailout program for Portugal.

Mixed Bag – Euro Confusion: Germany reported eye-popping first quarter GDP growth of +5.2%, the steepest year-over-year rise since reunification in 1990, yet lingering fiscal concerns surrounding the likes of Greece, Portugal, and Italy have intensified. Fitch, for example, recently cut its rating on Greece’s long-term sovereign debt three notches, from BB+ to B+ plus, and placed the country on “rating watch negative” status. These fears have pushed up two-year Greek bond yields to over 26%. Regarding the other countries mentioned, Standard & Poor’s, another credit rating agency, cut Italy’s A+ rating, while the European Union and International Monetary Fund agreed on a $116 billion bailout program for Portugal.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Rebuilding after the Political & Economic Tsunami

Excerpt from Free April Sidoxia Monthly Newsletter (Subscribe on right-side of page)

The Start of the Arab Uprising

The Arab uprising grew its roots from an isolated and disgraced Tunisian fruit vendor (26- year-old Mohammed Bouazizi) who burned himself to death in protest of the persistent, deep-seeded corruption prevalent throughout the government (view excellent 60 Minutes story on Tunisia uprising). The horrific death ultimately led to the swift removal of Egypt’s 30-year President Hosni Mubarak, whose ejection was spurred by massive Facebook-organized protests. Technology has flattened the world and accelerated the sharing of powerful ideas, which has awoken Arab citizens to see the greener grass across other global democratic nations. Facebook, Twitter, and LinkedIn can be incredible black-holes of productivity destroyers (I know firsthand), but as recent events have proven, these social networking services, which handle about 1 billion users globally, can also serve valuable purposes.

As the flames of unrest have been fanned across the Middle East and Northern Africa, autocratic dictators haven’t had the luxury of idly sitting on their hands. Instead, these leaders have been pushed to relent to the citizens’ wishes by addressing previously taboo issues, such as human rights, corruption, and economic opportunity. These fresh events feel like new-found changes, but these major social tectonic shifts have been occurring throughout history, including our lifetimes (e.g., Tiananmen Square massacre and the fall of the Berlin Wall).

Good News or Bad News?

Recent headlines have created angst among the masses, and the uncertainty has investors asking a lot of questions. Besides radioactive concerns in both Japan and the Middle East (one actual, one figurative), the “worry list” of items continues to stack higher. Oil prices, inflation, the collapsing dollar, exploding deficits, a China bubble, foreclosures, unemployment, quantitative easing (QE2), mountainous debt, 2012 elections, and the end of the world among others, are worries crowding people’s brains. Incredibly, somehow the market still manages to grind higher. More specifically, the Dow Jones Industrial Average has climbed a very respectable +6.4% for 2011.

With the endless number of worries, how on earth could the major market indexes still advance, especially after a doubling in value from 24 months ago? For one, these political and economic shocks are nothing new. History has shown us that democratic, capitalistic markets ultimately move higher in the face of wars, assassinations, banking crises, currency crises, and various other stock market frauds and scandals. I’m willing to go out on a limb and say these worrisome events will continue this year, next year, and even over the next decade.

Most baby boomers living in the early 1980s remember when 30-year mortgage rates on homes reached 18.5%, inflation hit 14.8%, and the Federal Funds interest rate peaked near 20%. Boomers also survived Vietnam, Watergate, the Middle East oil embargo, Iranian hostage crisis, 1987 Black Monday, collapse of the S&L banks, the rise and fall of the Cold War, Gulf War I/II, yada, yada, yada. Despite all these cataclysmic events, from the last birth of the Baby Boomers (1964), the Dow Jones Industrial catapulted from about 890 to 12,320. This is no April Fool’s joke! The market has increased a whopping 14-fold (without dividends) in the face of all this gruesome news. You won’t find that story on the front-page of The Wall Street Journal.

Lost Decade Goes on Sale

The gains over the last four and half decades have been substantial, but much more is said about the recent “Lost Decade.” Although it has generally been a lousy decade for most investors in the stock market, eventually the stock market follows the direction of profits. What the popular press negates to mention is that S&P 500 operating earnings have more than doubled from about $47 in 1999 to an estimated $97 in 2011. Over the same period, the price of the market has been chopped by more than half (i.e., the Price – Earnings multiple has been cut from 29x to 13.5x). With stocks selling at greater than -50% off from 1999, no wonder smart investors like Warren Buffett are buying America – Buffett just spent $9 billion in cash on buying Lubrizol Corp (LZ). Retail investors absolutely loved stocks in 2000 at the peak, believing there was virtually no risk. Now the tables have been turned and while stock prices are trading at a -50% discount, retail investors are intensely skeptical and nervous about the prospects for stocks. Shoppers don’t usually wait for prices to go up 30% and then say, “Oh goody, prices are much higher now, so I think I will buy!” but that is what they are saying now.

I don’t want to oversell my enthusiasm, because the deals were dramatically better in March of 2009. Hindsight is 20-20, but at the nadir of the stock market, stock prices traded at bargain basement levels of 7x times 2011 earnings. We may not see opportunities like that again in our lifetime, so sitting in cash may not be the most advisable positioning.

Although I would argue every investor should have some exposure to equities, an investor’s time horizon, objectives, constraints and risk tolerance should be the key determinants of whether your investment portfolio should have 5% equity exposure or 95% exposure.

So while the economic and political dominoes may appear to be tumbling based on the news du jour, don’t let the headlines and the so-called media pundits scare you into paralysis. Bad news and tragedy will continue, but fortunately when it comes to prosperity, history is on our side. As you attempt to organize and pickup the financial pieces of the last few years, make sure you have a disciplined, long-term investment plan that adapts to changing market and personal conditions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in LZ, Facebook, Twitter, LinkedIn, BRKA/B, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Spreading the Seeds of Democracy

Excerpt from Free March Sidoxia Monthly Newsletter (Subscribe on right-side of page)

As we bathe ourselves in petroleum products, it is moments like these that highlight our deeply engrained addiction to oil. The flames of fundamental human rights, freedom, and democracy are spreading like wildfire throughout the Middle East and North Africa, and as a result, the cost of living and doing business has gone up. What started as a random plea by a Tunisian fruit merchant in response to insidious corruption (26 year old Mohammed Bouazizi burned himself to death in revolt to continuous crooked government bribes) has resulted in a broad wave of protesters removing two authoritarian, autocratic Arab leaders. Egyptian President Hosni Mubarak and Tunisian President Zine al-Abidine Ben Ali have been swiftly cast out by energized protesters, and other repressive leaders are likely bound to topple as well.

Who’s next and when? You’ll have to stay tuned, but Colonel Muammar Gaddafi, the Libyan leader, is on the short list. Leaders in Yemen, Bahrain, Jordan, and Algeria are among the other countries that are feeling the heat too. Even though Egypt, Libya, Tunisia, and other aforementioned countries remain relative oil lightweights, fear over a political contagion spreading to more substantive countries like Saudi Arabia has gotten speculators frothing at the mouth, which pushed oil prices above $100 per barrel and gasoline prices to an average of $3.37 per gallon (about $3.60 in California according to AAA motor club).

Source: FT.com - The U.S. population is a fraction of the size of China and India, but we continue guzzling dramatically more crude.

While the bloodshed on the streets has created fodder for great sensationalist headlines for the media outlets, the fact of the matter is that the spread of democracy is nothing new, and the innate desire for basic human rights has never died. Going back to 1900 the world housed about 10 practicing democracies, and today there are arguably more than 100 democratic (and quasi-democratic) countries (see blue line in chart below).

Source: The Financial Times.com

In the U.S., our standard of living has exploded for more than a generation. The internet – and applications like Facebook and Twitter – have flattened the planet and connected the rest of the world to the pleasures available to free, transparent, and open societies. As we have experienced firsthand in Iraq, however, regime changes and moves towards democracy can be messy and costly. Ultimately, the native populations must spearhead the drive toward democratic, political change. Regime change solely rammed through by the U.S. will only create temporary change, and with our fiscal wallets empty, we frankly cannot afford it (see Global Babysitter).

Embracing Alternatives

We didn’t run out of stones in the Stone Age, and we did not run out of steel in the Industrial Revolution. When it comes to oil, the same principle applies. As globalization accelerates the expansion of democratic, emerging middle classes around the world, other oil-rich countries, like Saudi Arabia, understand the havoc that $100-$125 dollar a barrel has on demand destruction. Just like a drug dealer does not want to scare its addicted users, so too oil producers do not want to price consumers out of the market with high prices. Oil may be the lubricant for global commerce, but unlike the empty promises offered by the Jimmy Carter era in the 1970s, technology advancements in the alternative energy industry have reached critical mass. If you don’t believe me, just take a gander at the $17 billion the Chinese are pouring into electric vehicle technology (see Electrifying Profits), or the 20% total energy mandate from renewable sources being instituted in Europe by 2020. Even if we choose to watch from the sidelines and pick our noses, our foreign competitors will wave with delight as they embrace alternative energy resources and race past us. Even if political turmoil temporarily worsens in the Middle East, any additional oil price increases will only make alternative energy resources more economical, and thereby accelerate adoption and make disciples of alternative energy less dependent on some of these oil-rich, corrupt regimes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Foreign Frights & Debt Doubts

Excerpts from Sidoxia monthly newsletter (Subscribe on right side of page)

Over the last few years the globalized nature of the financial crisis has forced a diverse set of world leaders to deal with obscure international flare-ups in countries ranging from Iceland to Dubai, and Greece to Tunisia. The crisis du jour is the popular revolt in Egypt against 30-year president Hosni Mubarak and his autocratic, authoritarian government. The situation for the U.S. becomes a little sticky because Egypt, although creating a GDP (Gross Domestic Product) of less than the state of Illinois, is still the largest Arab country by population (approximately 82 million – even larger than Iran); a staunch ally with the U.S. in keeping peace with Israel; has contributed important intelligence to our country’s war on terror; and has been a responsible partner in controlling commerce through the all-important Suez Canal. The problem with Egypt and Mubarak’s regime is that the Egyptian economy is in relative shambles (they do not have oil reserves like their neighbors), unemployment is through the roof, and the government has been slow to push democratic advancements forward for the Egyptian people.

As emerging market “haves” increasingly join the ranks of the middle class, the people representing the “have-nots” of Yemen, Jordan, Algeria, Tunisia, Egypt, and others are thirsting for a cocktail of democracy and a higher standard of living, like some of their wealthier neighbors. These autocratic, authoritarian regimes can do their best to slow or delay the democratizations of their countries, but they cannot put the genie back in the bottle. Information is flowing faster than ever, and societies previously kept in the dark are now seeing the light of democracy.

Like any volatile government situation, there are threats and opportunities, depending on whether Mubarak stays in power, and if not, the nature of the new leadership. If an extremist government fills the leadership void, the U.S. may wish to rewind the clock and put the slow-moving reformist, Mubarak, back in power.

The short-term impact of the popular revolt may create additional volatility in the markets, but in the long-run, if the turmoil introduces more open, transparent, less corrupt, and democratic ideals to the new agenda, then the world will become a better place.

Bitter Debt Pill Tough to Swallow

There is never a shortage of issues to worry about, and from an economic standpoint, the suffocating amount of debt our country is dealing with is at the top of the concern list. The 2008-2009 financial crisis hole that we are still climbing our way out of is a friendly reminder of what happens to countries adopting irresponsible fiscal policies. The choking amount of debt the U.S. is swallowing remains a central issue for the current administration and will be a core topic to be debated through the 2012 Presidential election cycle.

How serious is the issue? The problem is serious enough the Congressional Budget Office (CBO) just raised its budget deficit forecast for fiscal 2011 to hit a record $1.5 trillion (9.8% of GDP), a level higher than $1.3 trillion in fiscal 2010. The blame for the new record can be largely attributed to the recent extension of the $858 billion in Bush tax-cuts and other benefits/breaks. Kicking the can down the road recently led Moody’s Investors Services of threatening the U.S. with a downgrade of its triple-A rated debt.

Source: The Peterson Institute

The President addressed some of our fiscal problems in his State of the Union Address recently (e.g., proposing a freeze on discretionary spending), but the rubber really hits the road when he comes out with his budget proposal later this month. How serious is he about reducing our hemorrhaging deficits? We’ll soon find out when the individual budget line-items are distributed for everyone to see. Shortly thereafter, around the end of March, the debt ceiling impasse will become a game of political “chicken.” Each side, Democrats and Republicans, will attempt to withdraw concessions from the other party, in exchange for a vote that will prevent a disastrous default of our government’s debt payments. Basically, our government is effectively looking to expand its credit card credit line, because our government credit limit is maxed out.

The situation isn’t hopeless if our politicians can show leadership by making difficult, unpopular fiscal decisions, but if America ignores our painful debt problems and does not take its bitter medicine, then prepare for an economy on the verge of keeling over.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

From Bearded Monks to Greek Decline

Photo source: vatopaidi.wordpress.com

Noted author Michael Lewis has sold millions of books and written on topics ranging from professional baseball to Wall Street and Iceland to Silicon Valley. Now, he has decided to tackle the gripping but nebulous Greek financial crisis through the eyes and bearded mouths of Greek monks in a recently released article from Vanity Fair.

At the heart of the story is a Christian monastery (Vatopaidi), located on a northeastern peninsula of Greece. This ten-century old sanctuary has helped expose the tenuous state of the Greek economy, which is estimated to be sitting on $1.2 trillion in debt (representing $.25 million per working Greek adult) – a massive number considering the relatively petite size of the country. Beyond interviewing the Vatopaidi monks, Lewis trolled through the country interviewing various politicians, businessmen, government officials, and natives in order to make sense of this Mediterranean mess.

The Scandal Genesis

Starting in 2008, news filtered out that Vatopaidi had somehow acquired a practically worthless lake and swapped it for 73 different government properties, including a 2004 Olympics center. The Vatopaidi monastery effectively created an estimated $1 billion+ commercial real estate portfolio from nothing, thanks to one of the key Vatopaidi monks negotiating a fishy, behind-the-door government exchange scheme. This scandal, among other issues, ultimately lead to the collapse of the prior Greek ruling party and sent Prime Minister Kostas Karamanlis packing his bags.

The Greek crisis did not happen overnight, but rather decades. A casual observer may mistake the caustic Greek media headlines as proof to blame Greece as the reason behind the global financial meltdown, Rather, the challenges faced by this island-based country are more symptomatic of the weak global credit standards and the undisciplined disregard for excessive debt levels. Even with an embarrassingly high debt/GDP ratio (Gross Domestic Product) of about 130%, Greece’s desperate financial situation is a relatively minor blemish in the whole global scheme of things. More specifically, the $300 billion or so in Greek GDP represents the equivalent of a pubescent pimple on the face of a $60 plus trillion global economy.

The Greek Concern

The Vatopaidi scandal is still being investigated, but how did this broader debt-induced, Greek fiscal catastrophe occur?

Lax tax collection, absence of legal enforcement, and simple corruption are a few of the contributing reasons. Lewis describes the situation as follows:

“Everyone is pretty sure everyone is cheating on his taxes, or bribing politicians, or taking bribes, or lying about the value of his real estate. And this total absence of faith in one another is self-reinforcing. The epidemic of lying and cheating and stealing makes any sort of civic life impossible; the collapse of civic life only encourages more lying, cheating, and stealing.”

A tax collector and real estate agent from the article had this to say:

“If the law was enforced, every doctor in Greece would be in jail.” AND

“Every single member of the Greek Parliament is lying to evade taxes.”

The Greek government also did an incredible job of distorting the reported economic data and swept reality under the rug:

“How in the hell is it possible for a member of the euro area to say the deficit was 3 percent of G.D.P. when it was really 15 percent?” a senior I.M.F. (International Monetary Fund) representative asked.

The Greek debacle was not an isolated incident. The significant dislocations occurring around the earth’s small and dark corners have directly impacted our lives here in the U.S. Take for example Iceland, the country that New York Times columnist Thomas Friedman called a converted “hedge fund with glaciers.” Not only did this historically tiny fishing island do dynamic damage to its southern neighbors in Europe, but damage from its collapsing banks extended all the way to busted condominium developments in Beverly Hills, California. Or consider Dubai and the multi-billion dollar debt restructuring at Nakheel Development that held the world breathless as people around the world watched in trepidation.

These examples, coupled with the Greek financial crisis highlight how widespread the collateral damage of cheap credit proliferated. The cost of money is still dangerously low, as governments around the globe attempt to stimulate demand, however the regulators and banking industry must remain vigilant in maintaining loan and capital deployment discipline. The hot debates over financial regulatory reform in the U.S., along with the recent Basel III banking requirement discussions are evidence of the need to restore balance and stability to the global financial playing field.

The global financial crisis has spooked billions of people around the world. Like a mysterious boogeyman, the crisis has turned cheap and easy credit into the public’s worst nightmare. The mysticism and general opacity surrounding the inner-workings of Wall Street and global financial markets attacks at investors’ inherent emotional vulnerabilities. Michael Lewis has once again helped turn what on the exterior seems extremely complex and confusing and boiled the essence of the problem down into terms the masses can digest and put into perspective.

Bearded monks loading up on government-swapped commercial real estate may have provided valuable lessons and insights into the global financial crisis, however now I can hardly wait for Michael Lewis’s next topic…perhaps balding nuns in South African gold mines?

Read the whole Vanity Fair article written by Michael Lewis

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

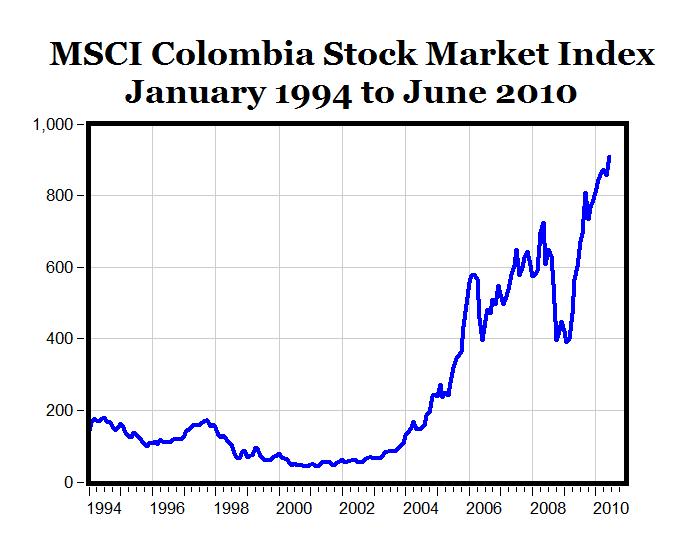

Colombia: The Hidden Latin American Gem

Judging by the all the volatility in the markets and the gloomy headlines blanketing business periodicals, one would think the global walls of capitalism and democracy were crumbling into oblivion. That’s why it’s a nice diversion to discover a diamond in the rough, shining through the darkness in the form of the Colombian stock market. How special is this South American gem? An +1,845% return over 10 years sounds pretty exceptional to me. Those are the results that Professor Dr. Mark J. Perry from the University of Michigan calculated in a posting he recently wrote about the MSCI Colombia stock market index in his blog, Carpe Diem.

Source: Carpe Diem

Fueling the surge in the equity markets has been a right-leaning, free market government with a hawkish defense stance, led by President Álvaro Uribe for the last eight years. The voters voted to continue Uribe’s mandate by voting in his former defense minister, Juan Manuel Santos, who promises to keep the disruptive guerilla forces operating under Revolutionary Armed Forces of Colombia (FARC) in check.

Colombia has been a close ally of the United States, thanks to their support of a joint crackdown on drug smuggling into the U.S. In return for their support, Colombia has received a nice fat $600 million check from the U.S. each year. What would even make our relationship tighter is an approval stamp placed on an awaiting U.S.-Colombia free trade agreement, which Congress has inexplicably kept on the backburner.

The U.S. and Colombia also agree on something else…their mutual disdain for Venezuelan leader, Hugo Chavez. Mr. Chavez poses a threat to the region, but Santos and the wave of free market leaders in the territory are more likely to wreak havoc on the Venezuelan leader according to Investor’s Business Daily:

“But Santos is probably most dangerous for Chavez, because Colombia’s rags-to-riches success story is so dramatic — showing that any beat-up nation can drag itself out of misery through markets — and because Venezuela and Colombia are such close neighbors. Word gets out about how well things are going in Colombia and it spreads fast in Venezuela. Santos need never fire a shot at Venezuela to slay Chavez’s revolution because the power of the markets will do it for him.”

Colombia’s Gross Domestic Product (GDP) is not overly large relative to some more developed neighbors, but the World Bank estimated the country’s 2008 GDP at $244 billion, almost triple the figure from five years earlier. The explosive economic growth explains how this market was the highest returning market in the world over the last decade, even eclipsing white hot markets like China, Russia, Brazil, Peru, India, and Turkey, among many others.

How does one invest in this Colombian gem? One way to gain exposure is through an exchange traded fund (ETF): Global X/InterBolsa FTSE Colombia 20 ETF (GXG). This particular ETF is concentrated into 20 positions, with heavy weightings in financial, energy, and industrial stocks. So, as you continue to read about the so-called inevitable “double-dip” recession and collapse of the U.S. dollar as the global reserve currency, please do not forget there are some brilliant free market economies, like Colombia, that are growing brilliantly and producing sparkling returns.

Read Professor Perry’s complete article on the Colombia market

Read the WSJ article written on the subject

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GXG, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Blowing the Perfect Investment Game

Photo source: Boston.com

Armando Galarraga, pitcher from the Detroit Tigers baseball team, became a victim of a blown call by umpire Jim Joyce, resulting in a lifetime opportunity being ripped from his clutches. Not only did the error in judgment cost Galarraga a perfect game – a feat only achieved by 20 pitchers over the last 130 years – but the blunder also cost him a no-hitter. Perfect games are difficult to come by in the investment world too, but for those ambitious investors reaching for the finance Hall of Fame, I strongly believe a healthy dosage of international and emerging markets is required to achieve perfection (or significant outperformance).

The Fab Five

The oft quoted view that the U.S. was the dominant economic powerhouse in the 20th century (after Britain controlled the 19th century) led me to analyze five emerging growth markets outside of the U.S. There are some clear leaders in pursuit of 21st century economic supremacy, however nothing in the global pecking order is guaranteed. What I do know is that me and my clients will be relying on the financial tailwinds of growth coming from these international markets to provide excess return potential to my portfolios (albeit at the cost of shorter-term volatility). Even retired individuals, or those with shorter time horizons, should consider small bite sizes of these emerging markets in their portfolios, if merely for some of the diversification benefits (see diversification article).

Pundits and media types endlessly write and talk about the “lost decade,” the demise of “buy and hold,” and/or the “death of equities.” Well, as you can see, the lost decade through the first half of 2010 turned out to be a significantly lucrative period for investors with the stomach and courage to invest outside the familiar comfort zone of the United States (see chart below).

Specifically, here is the international outperformance achieved in the sample of international markets as compared to the United States (S&P 500 Index):

- Brazil +266.22% (EWZ tracking Bovespa Index)

- India +266.16% (Bombay Stock Exchange – BSE)

- Australia +68.16% (ASX 200 Index)

- China +68.06% (Shanghai Index)

- Hong Kong +39.74% (Hang Seng Index)

- United States -128.19% Average Underperformance versus five other geographic indexes.

An added kicker for investment consideration is valuation. According to The Financial Times market data section, all these international markets, with the exception of India, trade at a discount to the S&P 500 on a Price/Earnings ratio basis (P/E).

Victim of Our Own Success

Graph source: The New York Times

In many respects, our country has continued to thrive in spite of some of our political and economic shortcomings. As you can see from the chart below (NY Times article) our country’s market share of the world’s Gross Domestic Product (GDP) has been steadily been declining since World War II (and we’ve still done OK). With U.S. GDP exceeding $14 trillion, our sheer size makes it much more difficult to grow relative to our smaller, more nimble international brethren. Given our top economic position in the world, Warren Buffett succinctly identified the force working against size when he said, “Gravity always wins.” I would expect gravitational influences to continue to weigh us down in the future, but our declining share should not be considered a detrimental trend. Globalization needs to be embraced by policymakers so we can take advantage of these faster growing countries as opportunistic export markets. We Americans can improve our standard of living while riding the coattails of our speedy neighbors. Do yourself a favor and include a healthy chunk of higher growth markets into your portfolio – it’s important you do not blow your own investment game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including BKF, FXI, EWZ), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Google vs. China: Running Away from 660 Million Eyeballs?

Wait, let me get this straight. Google, the $185 billion behemoth that wants to take over the world is seriously considering turning its back on a rapidly growing cluster of 660 million eyeballs (330 million Chinese internet users according to BusinessWeek)? After hitting their head on an obscenely high market share in the U.S. (67% search share based on Nielsen data) and looking for new geographies to expand, I’m supposed to believe Google will walk away from the third largest economy on this planet (see China: Trade of the Century)? The explanation given for Google’s capitulation is discontent related to unknown hackers and censorship concerns. If that’s not enough, this alleged saint-like posturing comes after Google sold its censorship soul for years, before seeing the free speech light. Although the company’s mission is to “do no evil,” Google had no qualms aggressively poaching Microsoft (MSFT) miracle maker, Kai-Fu Lee, to kick-start their Chinese presence. If free speech is truly at the root of the Google’s unease, then why wait four whole years and a hack-attack before laying down an ultimatum on the Chinese government?

I Smell a Rat

In a blog post written by Google’s Chief Legal Officer, David Drummond, the company explains how their iron curtain digital defense was bent but not broken:

“We have evidence to suggest that a primary goal of the attackers was accessing the Gmail accounts of Chinese human rights activists. Based on our investigation to date we believe their attack did not achieve that objective. Only two Gmail accounts appear to have been accessed, and that activity was limited to account information (such as the date the account was created) and subject line, rather than the content of emails themselves.”

I’m no exterminator, but I smell a rat. All this feels a lot more like politics and business tactics then it does an altruistic display of free-speech martyrdom. The Chinese government and Google executives know what is at risk, as they both play a high stakes game of “chicken.”

Google goes onto say:

“As part of our investigation we have discovered that at least twenty other large companies from a wide range of businesses–including the Internet, finance, technology, media and chemical sectors–have been similarly targeted.”

I’m confused. These unknown hackers attacked 20 different companies and only unsuccessfully cracked two Gmail accounts. The evidence sounds pretty harmless on the surface, if this language is representative of reality. Maybe I’m wrong, and a foiled cyber-attack is reason enough to cease operations in a country inhabiting a potential 1.3 billion customers.

Sure China represents a relatively small portion of Google’s revenues (estimated at less than $1 billion and a single digit percentage of revenues), but Google would be insane to walk away from this massive long-term growth market, even if Baidu (BIDU) is currently eating their lunch. Although Google has a smaller #2 position in China, it still has a respectable 35.6% search market share (according to BusinessWeek).

Not Just About Search – Cell Phones Too

Even if they claimed they were throwing in the white towel on their Chinese search business, I don’t think they really want to flush their newly minted cell phone prospects down the toilet. Even if 275 million or so cell phone users in the U.S. is fertile ground for Google to target their new Android-based phones, I’m guessing they have penciled out the gigantic mobile potential of the rapidly expanding 700 million+ Chinese mobile phone user market.

While I can’t take the scenario of Google ceasing China operations off the table, I consider the chance of Google shutting its doors in China significantly less than 50%. While the bold Google statement of feasibility review regarding their Chinese business existence has gained a lot of attention, I think calmer heads will eventually prevail and Google will resume their targeting of 660 million Chinese eyeballs. Who knows, the high stake game of “chicken” may even benefit their bottom-line as they win the hearts and minds of more future free-speech users.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own GOOG shares and China based exchange traded funds at the time of this article’s publishing, but did not have a direct position in MSFT and BIDU shares. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Mobius: The Kojak of Emerging Markets

Kojak substituting lollipops for nicotine.

Lieutenant Theo Kojak, played by Telly Savalas in the 1970s television series Kojak, is a bald, hard-nosed New York City police detective who hunts down criminals. Mark Mobius, executive chairman of Templeton Asset Management, is a bald, hard-nosed investment manager devoted to hunting down winning stocks in emerging markets. Expanding on his numerous authored books, Mobius recently decided to write his own blog expanding on his global travels and reporting back his investment findings.

Recently Mobius fielded some questions from his readers, covering emerging markets from China and Brazil to “Frontier” markets like Sri Lanka and Serbia (see also Trade of the Century). Here are a few of the exchanges:

In which countries, regions or sectors are you finding the best values?

“We are finding opportunities in almost all emerging markets. Our ground-up research process locates opportunities in countries where the political or economic outlooks may not, at first appearance, look good. Nevertheless, we generally favor China and Brazil, but also have large positions in Russia, India and Turkey. In terms of sectors, we believe commodity stocks look good because we expect the global demand for commodities to continue its long-term growth. We also favor consumer stocks. With rising per-capita income and strong demand for consumer goods and services in many emerging markets, we believe the earnings growth outlook for these stocks is positive.”

It appears that the financial market has changed, in that one needs to be more skeptical and cautious when investing than in the past. Alan Greenspan said that last year’s crash was unforeseen, and given the uncertainty of the markets and global financing, the big crash could happen again. What say you?

“Actually some analysts did see the crash coming in view of Greenspan’s loose monetary policies. The nature of markets is that there will always be booms and crashes since people tend to get either too optimistic or too pessimistic. The good news is that on average, bull markets have lasted longer than bear markets, and bull markets have gone up in percentage terms more than bear markets have gone down. In terms of other risks, I believe there is still a danger of the unregulated derivatives market.

Do you think Sri Lanka will turn around?

“We believe that Sri Lanka is fundamentally a rich country and that the challenges revolve around how the true potential in tourism, agriculture and industry can be effectively met. We have been investing in Sri Lanka for many years. For us, the biggest challenge in the public market is liquidity. Trading turnover is rather low although we have found some investment bargains.”

Belgrade’s Stock Exchange suffered heavy losses in the 2008 meltdown, with the Belex index falling sharply. I am from Serbia, and so I was thrilled to find out that Franklin Templeton is investing in Serbia.

“Yes, we are interested in the Serbian market and we are now looking at opportunities there. Of course, when markets are down, it is the best time to start looking and Belgrade is definitely on our list. We have already invested in a company in Serbia and look forward to looking more closely at that market.”

Mark Mobius - Not Moby

While Telly Savalas discovered fame 30 years ago from his Kojak role, Mr. Mobius has spent more than 30 years in the emerging markets chasing successful investments. Franklin Templeton Investors should remain happy if Mobius’ picks continue to shine, like his bald, polished crown.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (EEM, FXI, BKF). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}