Posts filed under ‘Fixed Income (Bonds)’

1994 Bond Repeat or 2013 Stock Defeat?

Interest rates are moving higher, bond prices are collapsing, and fear regarding a stock market plunge is palpable. Sound like a recent news headline or is this a description of a 1994 financial market story? For those with a foggy, double-decade-old memory, here is a summary of the 1994 economic environment:

- The economy registered its 34th month of expansion and the stock market was on a record 40-month advance

- The Federal Reserve embarked on its multi-hike, rate-tightening monetary policy

- The 10-year Treasury note exhibited an almost 2.5% jump in yields

- Inflation was low with a threat of rising inflation lurking in the background

- An upward sloping yield curve encouraged speculative bond carry-trade activity (borrow short, invest long)

- Globalization and technology sped up the pace of price volatility

Many of these listed items resemble factors experienced today, but bond losses in 1994 were much larger than the losses of 2013 – at least so far. At the time, Fortune magazine called the 1994 bond collapse the worst bond market loss in history, with losses estimated at upwards of $1.5 trillion. The rout started with what might have appeared as a harmless 0.25% increase in the Federal Funds rate (the rate that banks lend to each other) from 3% to 3.25% in February 1994. By the time 1994 came to a close, acting Federal Reserve Chairman Alan Greenspan had jacked up this main monetary tool by 2.5%.

Rising rates may have acted as the flame for bond losses, but extensive use of derivatives and leverage acted as the gasoline. For example, over-extended Eurobond positions bought on margin by famed hedge fund manager Michael Steinhardt of Steinhardt Partners lead to losses of about-30% (or approximately $1.5 billion). Renowned partner of Omega Partners, Leon Cooperman, took a similar beating. Cooperman’s $3 billion fund cratered -24% during the first half of 1994. Insurance company bond portfolios were hit hard too, as collective losses for the industry exceeded $20 billion, or more than the claims paid for Hurricane Andrew’s damage. Let’s not forget the largest casualty of this era – the public collapse of Orange County, California. Poor derivatives trades led to $1.7 billion in losses and ultimately forced the county into bankruptcy.

There are plenty of other examples, but suffice it to say, the pain felt by other bond investors was widespread as a massive number of margin calls caused a snowball of bond liquidations. The speed of the decline was intensified as bond holders began selling short and using derivatives to hedge their portfolios, accelerating price declines.

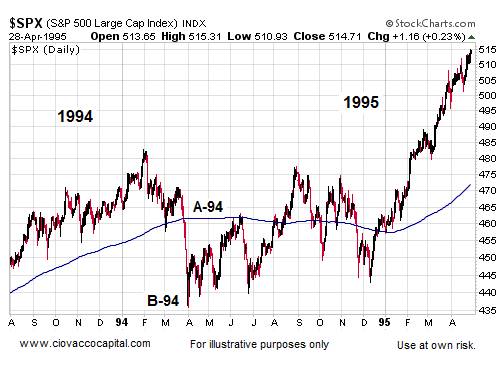

Just as the accommodative interest rate punch bowl was eventually removed by Greenspan, so too is Ben Bernanke (current Fed Chairman) threatening to do today. Even if Bernanke unleashes a cold-turkey tapering of the $85 billion per month in bond-purchases, massive losses in bond values won’t necessarily mean catastrophe for stock values. For evidence, one needs to look no further than this 1994-1995 chart of the stock market:

Source: Ciovaccocapital.com

Volatility for stocks definitely increased in 1994 with the S&P 500 index correcting about -10% early in the year. But as you can see, by the end of the year the market was off to the races, tripling in value over the next five years. Volatility has been the norm for the current bull market rally as well. Despite the more than doubling in stock prices since early 2009, we have experienced two -20% corrections and one -10% pullback.

What’s more, the onset of potential tapering is completely consistent with core economic principles. Capitalism is built on free trading markets, not artificial intervention. Extraordinary times required extraordinary measures, but the probabilities of a massive financial Armageddon have been severely diminished. As a result, the unprecedented scale of quantitative easing (QE) will eventually become more harmful than beneficial. The moral of the story is that volatility is always a normal occurrence in the equity markets, therefore any significant stock pullback associated with potential bond tapering (or fed fund rate hikes) shouldn’t be viewed as the end of the world, nor should a temporary weakening in stock prices be viewed as the end to the bull market in stocks.

Why have stocks historically provided higher returns than bonds? The short answer is that stocks are riskier than bonds. The price for these higher long-term returns is volatility, and if investors can’t handle volatility, then they shouldn’t be investing in stocks.

If you are an investor that thinks they can time the market, you wouldn’t be wasting your time reading this article. Rather, you’d be spending time on your personal island while drinking coconut drinks with umbrellas (see Market Timing Treadmill).

Although there are some distinct similarities between the economic backdrop of 1994 and 2013, there are quite a few differences also. For starters, the economy was growing at a much healthier clip then (+4.1% GDP growth), which stoked inflationary fears in the mind of Greenspan. Moreover, unemployment was quite low (5.5% by year-end vs. 7.6% today) and the Fed did not communicate forward looking Fed policy back then.

It’s unclear if the recent 50 basis point ascent in 10-year Treasury rates was just an appetizer for what’s to come, but simple mathematics indicate there is really only one direction left for interest rates to go…higher. If history repeats itself, it will likely be bond investors choking on higher rates (not stock investors). For the sake of optimistic bond speculators, I hope Ben Bernanke knows the Heimlich maneuver. Studying history may help bond bulls avoid indigestion.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Bond-Choking Central Banks Expand Investment Menu

Central banks around the globe are choking on low-yielding bonds, and as result are now expanding their investment menu beyond Treasuries into equities. Expansionary monetary policies purchasing short-term, low-rate bonds means that central banks have been gobbling up securities on their balance sheets that are earning next to nothing. To counteract the bond-induced indigestion of the central banks, many of them are considering increasing their equity purchasing strategies. How can you blame them? With the 10-year U.S. Treasury notes yielding 1.66%; 10-year German bonds eking out 1.21%; and 10-year Japanese Government Bonds (JGBs) paying a paltry 0.59%, it’s no wonder central banks are looking for better alternatives.

More specifically, the Bank of Japan (BOJ) is planning to pump $1.4 trillion into its economy over the next two years to encourage some inflation through open-ended asset purchases. Earlier this month, the BOJ said it has a goal of more than doubling equity related exchange traded funds (ETFs) by the end of 2014. According to Business Insider, the BOJ is currently holding $14.1 billion in equity ETFs with an objective to reach $35.3 billion in 2014.

I can only imagine how stock market bears feel about this developing trend when they have already blamed central banks’ quantitative easing initiatives as the artificial support mechanism for stock prices (see also The Central Bank Dog Ate my Homework).

While expanded equity purchases could break the backs of bond bulls and stock naysayers, some smart people agree that this strategy makes sense. Take Jim O’Neill, the chairman of Goldman Sachs Asset Management, who is retiring next week. Here’s what he has to say about expanded central bank stock purchases:

“Frankly, it makes a huge amount of sense in a world of floating exchange rates and such incredible opportunity, why should central banks keep so much money in very short term, liquid things when they’re not going to ever need it? To help their future returns for their citizens, why would they not invest in equity?”

How big is this shift towards equities? The Royal Bank of Scotland conducted a survey of 60 central banks that have about $6.7 trillion in reserves. There were 13% of the central banks already invested in equities, and almost 25% of them said they are or will be invested in equities within the next five years.

While I may agree that stocks generally are a more attractive asset class than bubblicious bonds right now, I may draw the line once the Fed starts buying houses, gasoline, and groceries for all Americans. Until then, dividend yields remain higher than Treasury yields, and the earnings yields (earnings/price) on stocks will remain more attractive than bond yields. Once stocks gain more in price and/or bonds sell off significantly, it will be a more appropriate time to reassess the investment opportunity set. A further stock rise or bond selloff are both possible scenarios, but until then, central banks will continue to look to place its money where it is treated best.

The central bank menu has been largely limited to low-yielding, overpriced government bonds, but the appetite for new menu items has heightened. Stocks may be an enticing new option for central banks, but let’s hope they delay buying houses, gasoline, and groceries.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Beware: El-Erian & Gross Selling Buicks…Not Chevys

As my grandmother always told me, “Be careful where you get your advice!” Or as renowned Wall Street trader Gerald Loeb once said, “The Buick salesman is not going to tell you a Chevrolet will fit your needs.” In other words, when it comes to investment advice, it is important to realize that opinions and recommendations are often biased and steeped with inherent conflicts of interest. Having worked in the financial industry over several decades, I have effectively seen it all.

However, one unique aspect I have grown accustomed to is the nauseating and fatiguing over-exposure of PIMCO’s dynamic bond duo, CEO Mohamed El-Erian and founder Bill Gross. Over the last four years and 13 consecutive quarters of GDP growth (likely 14 after Q4 revisions), I and fellow CNBC viewers have been forced to endure the incessant talk of the “New Normal” of weak economic growth to infinity. Actual results have turned out quite differently than the duet’s cryptic and verbose predictions, which have piled up over their seemingly non-stop media interview schedule. Despite the doomsday rhetoric from the bond brothers, El-Erian and Gross have witnessed a more than doubling in equity prices, which has soundly trounced the performance of bonds over the last four years.

After being mistaken for such a long period, certainly the PIMCO marketing machine would revise their pessimistic outlook, right? Wrong. In true biased fashion, El-Erian cannot admit defeat. Just this week, El-Erian argues stocks are artificially high due to excessive liquidity pumped into the financial system by central banks (see video below). I’m the first one to admit Federal Reserve Chairman Ben Bernanke is explicitly doing his best to force investors into risky assets, but doesn’t generational low interest rates help bond prices too? Apparently that mathematical fact has escaped El-Erian’s bond script.

Source: Yahoo! Finance (Daily Ticker)

El-Erian’s buddy, Bill Gross, can’t help himself from jumping on the stock rain parade either. Just six weeks ago Gross followed the bond-pumping playbook by making another dour prediction that the market would rise less than 5% in 2013. Unfortunately for Gross, his crystal ball has also been a little cloudy of late, with the S&P 500 index already up more than +6.5% this year. Since doomsday outlooks are what keeps the $2 trillion PIMCO machined primed, it’s no surprise we hear about the never-ending gloom. For those keeping score at home, let’s please not forget Bill Gross’s infamously wrong Dow 5,000 prediction (see article).

PIMCO Smoke & Mirrors: Stock Funds with NO Stocks

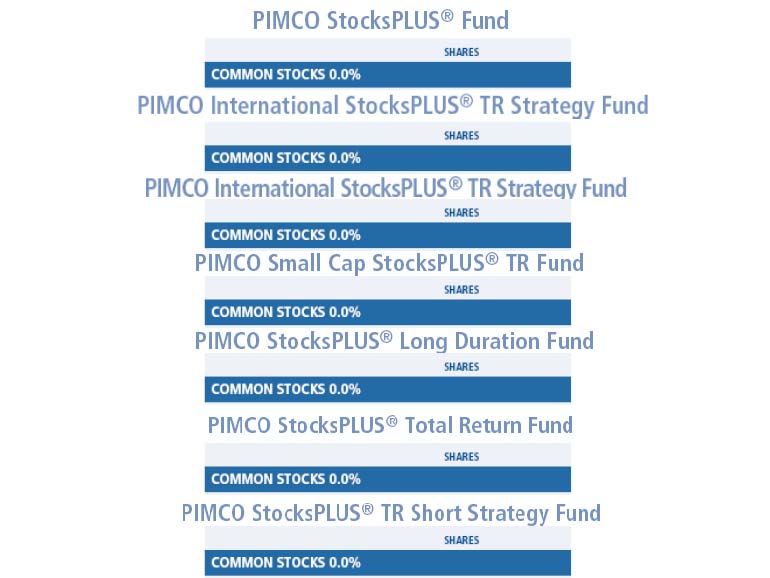

Just when I thought I had seen it all, I came across PIMCO’s Equity-Related funds. Never in my career have I seen “equity” mutual funds that invest solely in “bonds.” Well, apparently PIMCO has somehow creatively figured out how to create stock funds without investing in stocks. I guess that is one strategy for a bond-centric company of getting into the equity fund market? This is either ingenious or bordering on the line of criminal. I fall into the latter camp. How the SEC allows the world’s largest bond company to deceivingly market billions in bond-filled stock funds to individual investors is beyond me. After innocent people got fleeced by unscrupulous mortgage brokers and greedy lenders, in this Dodd-Frank day and age, I can’t help but wonder how PIMCO is able to solicit a StockPlus Fund that has 0% invested in common stocks. You can judge for yourself by reviewing their equity-related funds on their website (see also chart below):

PIMCO Equity-Related Funds with No Equity

PIMCO Active Equity Funds Struggle

With more than 99% of PIMCO’s $2 trillion in assets under management locked into bonds, company executives have made a half-hearted effort of getting into the equity markets, even though they’ve enjoyed high-fiving each other during the three-decade-long bond bull market (see Downhill Marathon Machine). In hopes of diversifying their bond-heavy revenue stream, in 2009 they hired the head of the high-profile $700 billion, government TARP program (Neil Kashkari). Subsequently, PIMCO opened its first set of actively managed funds in 2010. Regrettably for PIMCO, the sledding has been quite tough. In 2012, all six actively managed equity funds lagged their benchmarks. Moreover, just a few weeks ago, Kashkari their rock star hire decided to quit and pursue a return to politics.

Mohamed El-Erian and Bill Gross have never been camera shy or bashful about bashing stocks. PIMCO has virtually all their bond eggs in one basket and their leaderless equity division is struggling. What’s more, like some car salesmen, they have had a creative way of describing the facts. If it’s a Chevy or unbiased advice you’re looking for, I recommend you steer clear from Buick salesmen and PIMCO headquarters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in PIMCO funds, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rates Dance their Way to a Floor

The globe is awash in debt, deficits are exploding, and the Euro is about to collapse…right? Well, then why in the heck are six countries out of the G-7 seeing their 10-year sovereign debt trade at 2.5% or lower on a consistent downward long-term trajectory? What’s more, three of the six countries witnessing their rates plummet are from Europe, despite pundits continually calling for the demise of the eurozone.

Here is a snapshot of 10-year sovereign debt yields for the majority of the G-7 countries over the last few decades:

Source: TradingEconomics.com

The sole G-7 member missing from the bond yield charts above? Italy. Although Italy’s deficits are not massive (Italy actually has a smaller deficit than U.S. as % of GDP: 3.9% in 2011), its Debt/GDP ratio has been large and rising (see chart below):

Source: TradingEconomics.com

As the globe has plodded through the financial crisis of 2008-2009, investors have flocked to the perceived stability of these larger developed countries’ bonds, even if they are merely better homes in a bad neighborhood right now. PIMCO likes to call these popular sovereign bonds, “cleaner dirty shirts.” Buying sovereign debt from these less dirty shirt countries, without sensitivity to price or yield, has been a lucrative trade that has worked consistently for quite some time. Now, however, with sovereign bond yields rapidly approaching 0%, it becomes mathematically impossible to fall lower than the bottom rate floor that developed countries are standing on.

Bond bears have been wrong about the timing of the inevitable bond price reversal, myself included, but the bulls are skating on thinner and thinner ice as rates continue moving lower. The bears may prolong their bragging rights if interest rates continue downward, or persist at these lower levels for extended periods of time. Eventually the “buy the dips” mentality dies, as we so poignantly experienced in 2000 when the technology dips turned into outright collapse.

The Flies in the Bond Binging Ointment

As long as equities remain in a trading range, the “risk-off” bond binging arguments will continue holding water. If corporate earnings remain elevated and stock buybacks carry on, the pain of deflating real returns will eventually become too unbearable for investors. As the insidious rising prices of energy, healthcare, food, leisure, and general costs keep eating away everyone’s purchasing power, even the skeptics will become more impatient with the paltry returns they are currently earning. Earning negative real returns in Treasuries, CDs, money market accounts, and other conservative investments, is not going to help millions of Americans meet their future financial goals. Due to the laundry list of global economic concerns, large swaths of investors are still running and hiding, but this is not a sustainable strategy longer term. The danger from these so-called “safe,” low-yielding asset classes is actually riskier than the perceived risk, in my view.

With that said, I’ve consistently held there are a subset of investors, including a significant number of my Sidoxia Capital Management clients, who are in the later stage of retirement and have a rational need for capital preservation and income generating assets (albeit low yielding). For this investor segment, portfolio construction is not executed due to an opportunistic urge of chasing potential outsized rates of return, but more-so out of necessity. Shorter time horizons eliminate the prudence of additional equity exposure because of the extra associated volatility. Unfortunately, many of the 76 million Baby Boomers will statistically live another 20 – 30 years based on actuarial life expectations and under-save, so the risks of being too conservative can dramatically outweigh the risks of increasing equity exposure. This is all stated in the context of stocks paying a higher yield than long-term Treasuries – the first time in a generation.

Short-term risks and uncertainties remain high, with Greek election outcomes unknown; a U.S. Presidential election in flux; and an impending domestic fiscal cliff that needs to be addressed. But with interest rates accelerating towards 0% and investors’ fright-filled buying of pricey, low-yielding asset classes, many of these risks are already factored into current valuations. As it turns out, the pain of panic can be more detrimental than being stuck in over-priced assets, driven by rates dancing near an absolute floor.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Rule of 20 Can Make You Plenty

There is an endless debate over whether the equity markets are overvalued or undervalued, and at some point the discussion eventually transitions to what the market’s appropriate P/E (Price-Earnings) level should be. There are several standard definitions used for P/Es, but typically a 12-month trailing earnings, 12-month forward earnings (using earnings forecasts), and multi-year average earnings (e.g., Shiller 10-year inflation adjusted P/E – see Foggy P/E Rearview Mirror) are used in the calculations. Don Hays at Hays Advisory (www.haysadvisory.com) provides an excellent 30+ year view of the historical P/E ratio on a forward basis (see chart below).

Blue Line: Forward PE - Red Line: Implied Equilibrium PE (Hays Advisory)

If you listen to Peter Lynch, investor extraordinaire, his “Rule of 20” states a market equilibrium P/E ratio should equal 20 minus the inflation rate. This rule would imply an equilibrium P/E ratio of approximately 18x times earnings when the current 2011 P/E multiple implies a value slightly above 11x times earnings. The bears may claim victory if the earnings denominator collapses, but if earnings, on the contrary, continue coming in better than expected, then the sun might break through the clouds in the form of significant price appreciation.

Just because prices have been chopped in half, doesn’t mean they can’t go lower. From 1966 – 1982 the Dow Jones Industrial index traded at around 800 and P/E multiples contracted to single digits. That rubber band eventually snapped and the index catapulted 17-fold from about 800 to almost 14,000 in 25 years. Even though equities have struggled at the start of this century, a few things have changed from the market lows of 30 years ago. For starters, we have not hit an inflation rate of 13% or a Federal Funds rate of 20% (~3.5% and 0% today, respectively), so we have some headroom before the single digit P/E apocalypse descends upon us.

Fed Model Implies Equity Throttle

Hays Advisory exhibits another key valuation measurement of the equity market (the so-called “Fed Model”), which compares the Treasury yield of the 10-year Note with the earnings yield of stocks (see chart below).

Blue Line: 10-Yr Treasury - Red Line: Forward PE (Hays Advisory)

Regardless of your perspective, the divergence will eventually take care of it in one of three ways:

1.) Bond prices collapse, and Treasury yields spike up to catch up with equity yields.

2.) Forward earnings collapse (e.g., global recession/depression), and equity yields plummet down to the low Treasury yield levels.

AND/OR

3.) Stock prices catapult higher (lower earnings yield) to converge.

At the end of the day, money goes where it is treated best, and at least today, bonds are expected to treat investors substantially worse than the unfaithful treatment of Demi Moore by Ashton Kutcher. The Super Committee may not have its act together, and Europe is a mess, but the significant earnings yield of the equity markets are factoring in a great deal of pessimism.

The holidays are rapidly approaching. If for some reason the auspice of gifts is looking scarce, then review the Fed Model and Rule of 20, these techniques may make you plenty.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Your Portfolio’s Silent Killer

Shhh, if you listen closely enough, you may hear the sound of your portfolio disintegrating away due to the quiet killer…inflation. Inflation is especially worrisome with what we’ve seen happening with commodity prices and the drastic fiscal challenges our country faces. Quantitative Easing (read Flying to the Moon) has only added fuel to the inflation fear flames.

Whether you’re a conspiracy theorist who believes the government inflation data is cooked, or you are a Baby Boomer just looking to secure your retirement, it doesn’t take a genius to figure out that movies, pair of jeans, a tank of gas, concert tickets, or healthcare premiums are all going up in price (See also Bacon and Oreo Future).

Inflation starting to heat up. Source: IMF/Bloomberg via Financial Times

Companies are currently churning out quarterly results in volume and seeing the impact from commodity prices, whether you are McDonald’s Corp. (MCD) facing rising beef prices or luxury handbag maker Coach Inc. (COH) dealing with escalating leather costs, margins are getting crimped. Investors, especially those on fixed income streams, are experiencing the same pain as these corporations, but the problem is much worse. Unlike a market share leading company that can pass on price increases onto its customers, an investor with piles of cash, and low yielding CDs (Certificates of Deposit), and bonds runs the risk of getting eaten alive. Baby Boomers are beginning to reach retirement age in mass volume. Life spans are extending, and this demographic pool of individuals will become ever-large consumers of costlier and costlier healthcare services. If investments are not prudently managed, Baby Boomers will see their nest eggs evaporate, and be forced to work as Wal-Mart (WMT) greeters into their 80s…not that there’s anything wrong with that.

Every day investors are bombarded with a hundred different scary headlines on why the economy will collapse or the world will end. Most of these sensationalist scare tactics distort the truth and overstate reality. What is understated is what Charles Ellis (see Winning the Loser’s Game) calls a “corrosive power”:

“Over the long run, inflation is the major problem for investors, not the attention-getting daily or cyclical changes in securities prices that most investors fret about. The corrosive power of inflation is truly daunting: At 3 percent inflation – which most people accept as ‘normal’ – the purchasing power of your money is cut in half in 24 years. At 5 percent inflation, the purchasing power of your money is cut in half in less than 15 years – and cut in half again in 15 years to just one-quarter.”

In order to bolster his case, Ellis cites the following period:

“From 1977 to 1982, the inflation-adjusted Dow Jones Industrial Average took a five-year loss of 63 percent…In the 15 years from the late 1960s to the early 1980s the unweighted stock market, adjusted for inflation, plunged by about 80 percent. As a result, the decade of the 1970s was actually worse for investors than the decade of the 1930s.”

Solutions – How to Beat Inflation

Although the gold bugs would have you believe it, we are not resigned to live in a world with worthless money, which only has a useful purpose as toilet paper. There are ways to protect your portfolio, if you are properly invested. Here are some strategies to consider:

- TIPS (Treasury Inflation Protection Securities): These government-guaranteed tools are a useful way to protect yourself against rising inflation (see Drowning TIPS).

- Equities (including real estate): Bond issuers do not generally call up there investors and say, “You are such a great investor, so we have decided to increase your interest payments.” However, many publicly traded stocks do exactly that. Wal-Mart Stores (WMT) is an example of such a company that has increased its dividend for 37 consecutive years. As alluded to earlier, stocks are unique in that they allow inflationary pressures placed on operating profits to be relieved somewhat by the ability to pass on price increases to customers.

- Commodities: Whether you are talking about petroleum products, precious metals (those with a commercial purpose), or agricultural goods, commodities in general act as a great inflationary hedge. Another reason that commodities broadly perform better in an inflationary environment is because the U.S. dollar can often depreciate, which commonly increases the value of commodities.

- Short Duration Bonds: Rising rates are usually tied to escalating inflation, therefore investors would be best served by reducing maturity length and increasing coupon.

There are other ways of battling the inflation problem, but number one is saving and investing across a broadly diversified portfolio. If you want to secure and grow your nest egg, you need to use the silent power of compounding (see Penny Saved is Billion Earned) to combat the silent killer of inflation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, WMT, TIP, equities, commodities, and short duration bonds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Winning Coaches Telling Players to Quit

How would you feel if your coach told you not only are you going to lose, but you should quit and join the other team? Effectively, that is what Loomis Sayles bond legend Dan Fuss (read Fuss Making a Fuss), and fellow colleagues Margie Patel (Wells Fargo Advantage Funds), and Anthony Crescenzi (PIMCO) had to say about the chances of bonds winning at the recent Advisors’ Money Show.

This is what Fuss said regarding “statistically cheap” equities:

“I’ve never seen it this good in half a century.”

Patel went on to add:

“By any measure you want to look at, free cash flow, dividend yield, P/E ratio – stocks look relatively cheap for the level of interest rates.” Stock offer a “once-in-a-decade opportunity to buy and make some real capital appreciation.”

Crescenzi included the following comments about stocks:

“Valuations are not risky…P/E ratios have been fine for a decade, in part because of the two shocks that drove investors away from equities and compressed P/E ratios.”

Bonds Dynasty Coming to End

The bond team has been winning for three decades (see Bubblicious Bonds), but its players are getting tired and old. Crescenzi concedes the “30-year journey on rates is near its ending point” and that “we are at the end of the duration tailwind.” Even though it is fairly apparent to some that the golden bond era is coming to a close, there are ways for the bond team to draft new players to manage duration (interest rate/price sensitivity) and protect oneself against inflation (read Drowning TIPS).

Equities on the other hand have had a massive losing streak relative to bonds, especially over the last decade. The equity team had over-priced player positions that exceeded their salary cap and the old market leaders became tired and old. Nothing energizes a new team better than new blood and new talent at a much more attractive price, which leaves room in the salary cap to get the quality players to win. There is always a possibility that bonds will outperform in the short-run despite sky-high prices, and the introduction of any material, detrimental exogenous variable (large country bailout, terrorist attack, etc.) could extend bonds’ outperformance. Regardless, investors will find it difficult to dispute the relative attractiveness of equities relative to prices a decade ago (read Marathon Investing: Genesis of Cheap Stocks).

As I have repeated in the past, bonds and cash are essential in any portfolio, but excessively gorging on a buffet of bonds for breakfast, lunch, and dinner can be hazardous for your long-term financial health. Maximizing the bang for your investment buck means not neglecting volatile equity opportunities due to disproportionate conservatism and scary economic media headlines.

There are bond coaches and teams that believe the winning streak will continue despite the 30-year duration of victories. Fear, especially in this environment, is often used as a tactic to sell bonds. Conflicts of interest may cloud the advice of these bond coaches, but the successful experienced coaches like Dan Fuss, Margie Patel, Anthony Crescenzi are the ones to listen to – even if they tell you to quit their team and join a different one.

Read Full Advisor Perspectives Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including TIP), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

QE2 Drowning TIPS Yields Below Water

The holiday season is creeping up on us, and the only question building up more anticipation than what gift kids are going to get from Santa Claus is what investors are going to get from Federal Reserve Chairman Ben Bernanke – in the form of QE2 (Quantitative Easing Part II)? The inevitable QE2 program is an effort designed by the Fed to keep interest rates low and reduce the threat of deflation. In addition, QE2 is structured to stimulate the meager 0.8% core inflation experienced over the last 12 months (Bloomberg) to a Goldilocks level – not too hot and not too cold. Some pundits suggest the Fed should target a 2% inflation rate. QE2 asset purchase estimates are all over the map, but I can safely guess somewhere between a few hundred billion and $2 trillion (very brave of me).

Treasuries Weigh Down TIPS Yields

Ever since QE1 expired in the March timeframe, speculation began about the next potential slug of Treasuries and mortgage backed securities to be purchased by the Fed. As a consequence, this speculation became a contributing factor to 10-Year Treasury yields plummeting from around 4.0% to around 2.5%. Simultaneously, 5-Year TIPS (Treasury Inflation Protection Securities) yields have moved to negative territory.

Scott Grannis at Calafia Beach Pundit has a great chart showing the relationship between nominal Treasury yields, real TIPS yields, and expected inflation for 10-year maturities. As you can see below, over the last ten years there has been a tight correlation between the 10-year Treasury bond versus TIPS, with the former 10-year declining yield acting as a weight drowning the latter TIPS yield:

Source: scottgrannis.blogspot.com

Worth noting, absent the brief period in late-2008 and early-2009, inflation expectations have been remarkably stable in that 1.5% – 2.5% range.

Negative Yields…Who Cares?!

Unprecedented times have created an unprecedented appetite for bonds (see Bubblicious Bonds), and as a result, we just witnessed a historic $10 billion TIPS auction this week producing an eye-catching negative -0.55% yield. Sensationalist commentators characterize the negative yield dynamic as a money losing proposition, whereby investors are forced to pay the government. This assertion is quite a distortion and not quite true – we will review the mechanics of TIPS later.

- Source: scottgrannis.blogspot.com

If we’re not back to a panic filled environment of soup kitchen lines and bank runs, then why are TIPS paying a negative yield?

- QE2: As mentioned above, investor expectations are that Uncle Sam will come to the rescue and deliver lower interest rates (higher prices) through purchases of Treasuries and mortgage-backed securities.

- Rising Inflation Expectations: As fears surrounding future inflation increase, the price of TIPS will rise, and yields will fall.

- Sluggish Economy: Lackluster growth and fear of double dips have pressured rates lower as debates still linger about whether or not the U.S. will follow Japan (see Lost Decade).

Nuts & Bolts of TIPS

TIPS maturities come in terms of 5 years, 10 years and 30 years. Per the Treasury, 5-year TIPS are auctioned in April and October; 10-year TIPS in January, March, May (beginning in 2011), July, September, and November; and 30-year TIPS in February and August.

This table from Barclays Capital below does an excellent job of conceptually displaying the differences between vanilla Treasuries and TIPS.

Some Observations:

1) As you can see, the principal value of the TIPS security adjusts with inflation (Consumer Price Index). The price of the TIPS security, which we cannot see in the example, adjusts upwards (or downwards) with inflation expectations.

2) The TIPS security pays a lower coupon (3.5% vs. 5.0%), but you can see that under a 4% annual inflation assumption (principal value adjusts from $10,000 in Year 0 to $10,400 in Year 1), the ending value of the TIPS comes up significantly higher ($19,172 vs. $15,000).

3) The break-even inflation expectation rate is 1.5% (derived from 5% coupon minus 3.5% coupon). If you think inflation will average more than 1.5%, then buy the TIPS security. If you think inflation will average less than 1.5%, then buy the 10-year Treasury.

TIPS Advantages

- Inflation Protection: At the risk of stating the obvious, if you expect long-term inflation to average substantially more than about 2% (current inflation expectations), then TIPS are a great way of protecting your purchasing power.

- Deflation Protection: Perhaps TIPS should be called DIPS (Deflation Income Protection Securities)? What some investors do not realize is that even if our country were to spiral into long-term deflationary crisis, TIPS investors are guaranteed the original amount of principal. Yes, that’s right…guaranteed. Interest payments could conceivably decline to zero and the principal value could temporarily fall below par, but the government guarantees the original principal regardless of the scenario.

- No Credit or Default Risk: The advantage of the government owning its own printing press is that there is very little risk of default, so preservation of capital is not much of a risk.

TIPS Disadvantages

- Interest Rate Risk: It’s great to be indexed to inflation, but because TIPS include long-range maturities, investors face a significant amount of interest rate risk if the TIPS are not held until maturity. TIPS will likely outperform Treasuries under a rising rate scenario, but will be impacted nonetheless.

- CPI Risk: Even if you are not a conspiracy theorist who believes government CPI figures are artificially depressed, it is still quite possible your personal baskets of purchases do not perfectly align with the arbitrary CPI basket of goods.

- Negative Deflation Adjustments: Although a TIPS investor has an embedded “deflation floor” equivalent to original principal value, interest payments will be negatively impacted by declines in principal value during deflationary periods. Also, previously issued TIPS with accumulated principal values from inflationary adjustments run larger principal loss risks as compared to newly issued TIPS.

Although 5-year TIPS yields may have dunked below water into negative territory, the headline bark is much worse than the bite. There has been a massive rally in bond prices in front of the QE2 bond binge by the Fed. Nevertheless, inflation expectations have remained fairly stable and TIPS still provide defensive characteristics under both a future inflationary or deflationary scenario. If the Fed is indeed successful in manufacturing a reasonable Goldilocks range of inflation then TIPS yields should once again be able to come up for air.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including TIP), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

PIMCO – The Downhill Marathon Machine

How would you like to run a marathon? How about a marathon that is prearranged all downhill? How about a downhill marathon with the wind at your back? How about a downhill marathon with the wind at your back in a wheelchair? Effectively, that is what a 30-year bull market has meant for PIMCO (Pacific Investment Management Co.) and the “New Normal” brothers (Co-Chairman Bill Gross and Mohamed El-Erian) who are commanding the bond behemoth (read also New Normal is Old Normal). Bill Gross can appreciate a thing or two about running marathons since he once ran six marathons in six consecutive days.

This perseverance also assisted Gross in co-founding PIMCO in 1971 with $12 million in assets under management. Since then, the company has managed to add five more zeroes to that figure (today assets exceed $1.2 trillion). In the first 10 years of the company’s existence, as interest rates were climbing, PIMCO managed to layer on a relatively thin amount of assets (approximately $1 billion). But with the tailwind of declining rates throughout the 1980s, PIMCO’s growth began to accelerate, thereby facilitating the addition of more than $25 billion in assets during the decade.

The PIMCO Machine

For the time-being, PIMCO can do no wrong. As the endless list of media commentators and journalists bow to kiss the feet of the immortal bond kings, the blinded reporters seem to forget the old time-tested Wall Street maxim:

“Never confuse genius with a bull market.”

The gargantuan multi-decade move in interest rates, the fuel used to drive bond prices to the moon, might have something to do with the company’s success too? PIMCO is not exactly selling ice to the Eskimos – many investors are scooping up PIMCO’s bond products as they wait in their bunkers for Armageddon to arrive. Thanks to former Federal Reserve Chairman Paul Volcker (appointed in 1979), the runaway inflation of the early 1980s was tamed by hikes he made in the key benchmark Federal Funds Rate (the targeted rate that banks lend to each other). From a peak of around 20% in 1980-1981 the Fed Funds rate has plummeted to effectively 0% today with the most recent assistance coming from current Fed Chairman Ben Bernanke.

Although these west-coast beach loving bond gurus are not the sole beneficiary in this “bond bubble” (see Bubblicious Bonds story), PIMCO has separated itself from the competition with its shrewd world-class marketing capabilities. A day can hardly go by without seeing one of the bond brothers on CNBC or Bloomberg, spouting on about interest rates, inflation, and global bond markets. As PIMCO has been stepping on fruit in the process of collecting the low-hanging fruit, the firm has not been shy about talking its own book. Subtlety is not a strength of El-Erian – here’s what he had to pimp to the USA Today a few months ago as bond prices were continuing to inflate: “Simply put, investors should own less equities, more bonds, more global investments, more cash and more dry ammunition.”

If selling a tide of fear resulted in a continual funnel of new customers into your net, wouldn’t you do the same thing? Fearing people into bonds is something El-Erian is good at: “In the New Normal you are more worried about the return of your capital, not return on your capital.” Beyond alarm, accuracy is a trivial matter, as long as you can scare people into your doomsday way of thinking. The fact Bill Gross’s infamous Dow 5,000 call never came close to fruition is not a concern – even if the forecast overlapped with the worst crisis in seven decades.

Mohamed Speak

Mohamed El-Erian is a fresher face to the PIMCO scene and will be tougher to pin down on his forecasts. He arrived at the company in early 2008 after shuffling over from Harvard’s endowment fund. El-Erian has a gift for cryptically speaking in an enigmatic language that could only make former Federal Reserve Chairman Alan Greenspan proud. Like many economists, El-Erian laces his commentary with many caveats, hedges, and generalities – concrete predictions are not a strength of his. Here are a few of my favorite El-Erian obscurities:

- “ongoing paradigm shift”

- “endogenous liquidity”

- “tail hedging”

- “deglobalization”

- “post-realignment”

- “socialization losses”

Excuse me while I grab my shovel – stuff is starting to pile up here.

Don’t get me wrong…plenty of my client portfolios hold bonds, with some senior retiree portfolios carrying upwards of 80% in fixed income securities. This positioning is more a function of necessity rather than preference, and requires much more creative hand-holding in managing interest-rate risk (duration), yield, and credit risk. At the margin, unloved equities, including high dividend paying Blue Chip stocks, provide a much better risk-adjusted return for those investors that have the risk tolerance and time-horizon threshold to absorb higher volatility.

PIMCO has traveled along a long prosperous road over the last 30 years with the benefit of a historic decline in interest rates. While PIMCO may have coasted downhill in a wheelchair for the last few decades, this behemoth may be forced to crawl uphill on its hands and knees for the next few decades, as interest rates inevitably rise. Now that is a “New Normal” scenario Bill Gross and Mohamed El-Erian have not forecasted.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in PIMCO/Allianz, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Next Looming Bailout…Muni Bonds

Source: Photobucket

Government politicians and voters have made it clear they do not want to bail out “fat-cat” bankers in the private sector, but what about bailing out “fat-cat” state pensioners in the public sector? States and cities across the country are increasingly under economic strain with deficits widening and debt-loads stacking up. California’s statewide budget problems have been well publicized, but you are now also hearing about more scandalous financial problems at the city level (read about the multi-million dollar malfeasance in the city of Bell).

Why Worry?

Well if a 2010 $1.3 trillion federal deficit is not enough to tickle your fancy, then how does another $137 billion in state deficits over fiscal 2011 and 2012 sound to you (National Governors Association)? Unfortunately, the states have made no meaningful structural improvements. If you layer on general economic “double dip” recession fears with excess pension liabilities, then you have a recipe for a major unresolved financial predicament.

Despite the dire financial state of the states, municipal bond prices have generally survived the 2008-2009 financial crisis unscathed. With unacceptably poor state budget risks, muni bond prices have continued to rise in 2010. The downside…new investors must accept a pitiful yield of 2.75% on 10-year municipal debt, according to Financial Advisor Magazine.

One investor who is not buying into the strength of the tax-free municipal bond market is famed investor and CEO of Berkshire Hathaway (BRKA/BRKB), Warren Buffett. Here is what he wrote about munis in his legendary annual shareholder letter last year:

“Insuring tax-exempts, therefore, has the look today of a dangerous business…Local governments are going to face far tougher fiscal problems in the future than they have to date.”

Buffett has this to say about rating muni bonds:

“I mean, if the federal government will step in to help them [municipalities], they’re triple-A. If the federal government won’t step in to help them, who knows what they are?”

Safety Net Disappears

Source: Photobucket

Like a high wire artist dangling high in the air without a safety net below, the states are currently borrowing money with little to no protection from the bond insurance providers. The shakeout of the subprime debt defaults has battered the insurers from many perspectives, leaving a much smaller market in the wake of the financial crisis. In 2007 about 50% of new municipal bonds were issued with bond insurance, while today only approximately 7% carry it (UBS Wealth Management Research). With decreased insurance coverage, the silver lining for muni investors is the necessity for them to perform more comprehensive research on their bond holdings.

Defaults on the Rise

On the whole, less insurance will result in more defaults. Although defaults are expected to decline in 2010, non-payments totaled $6.9 billion in 2009, up from $526 million in 2007 (Distressed Debt Securities). Even though the numbers sounds large, the recent default rate only represents a 0.25% default rate on the hefty $2.8 trillion market. That muni default rate compares to a more intimidating corporate bond default rate of 11% in 2009.

Bigger Bark Than Bite?

James T. Colby, senior municipal strategist at Van Eck Global, understands the severity of the states’ budget crisis but he believes a lot of the doomsday headlines are bogus. Riva Atlas, writer for Financial Advisor Magazine, summarizes Colby’s thoughts:

“Even those states in the worst straits like California and Illinois have provisions in their constitutions or statutes requiring them to pay their debts. In California, the state’s constitution says bondholders come second only to the school system, so the state would have to empty its jails before it stopped paying its teachers.”

Certainly municipalities could raise taxes to compensate for any budget shortfalls, but we all know most politicians are reluctant to raise taxes, because guess what? Tax increases may result in fewer votes – the main motivator driving most politicians.

If the states decide to not raise taxes, they still have other ways to weasel out of obligations. For starters, they can just stick it to the insurance company (if coverage exists). If that option is not available, the municipalities can look to the federal government for a bailout. Irresponsible actions have their consequences, and like consumers walking away from payments on their mortgages, municipalities will effectively be preventing themselves from future access to borrowing. Either way, the bark is less than the bite for investors since the insurance company or federal government will be making them whole.

BABs and Taxes Add Fuel to the Fire

A glut of Build America Bonds (BABs) issued by municipalities, driven by demand from yield hungry pension funds, along with expected tax hikes for the wealthy have created a scarcity of tax-free munis.

In the first half of 2010 BABs accounted for more than 25% of municipal bonds issued, which was a significant contributing factor to the robust muni market. The BABs tailwinds aiding muni prices won’t last forever, as the bond issuance program is expected to expire at the end of 2010.

On the tax front, the wealthy are likely to see higher federal tax rates in the future – upwards of 36% – 40%. If you include the double tax-exempt benefits in states like New York and California, the relative attractiveness becomes even that much better. Combined, these factors have elevated muni prices.

Despite higher defaults, scarier headlines, and the lack of insurance, the municipal bond market remains robust. General interest rate declines caused by macroeconomic fears have caused investors to flock to the perceived “safe haven” status of Treasuries and Munis, but as we have all witnessed, the fickle pendulum of emotions never sits still for long.

Managing the Munis

As is evident from the municipal bond discussion, states and cities across the country have been plagued by the same deficit and debt issues as the country faces on a federal level. Tough structural expense issues, and revenue generating tax policies need to be scrutinized in order to prevent federal taxpayer bailouts of municipalities across the country.

From a municipal bond investor perspective, it’s best to focus on general obligation bonds (GOs) because those bonds are backed by the taxing authority of the municipal government. On the flip side, it’s best to stray away from revenue bonds or privately issued municipals because revenue streams from these bond channels are not guaranteed by the municipality, meaning the risk of default is larger.

While Congress sorts out financial regulatory reform with respect to banking bailouts and “too big to fail” corporations, our federal government should not lose sight of the widespread municipality problems our country faces today. If not, get ready to pull out the checkbook to pay for another taxpayer-led bailout…

Read the Complete Financial Advisor Magazine Article: The Muni Minefield

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including CMF), but at the time of publishing SCM had no direct position in BRKA/B or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}