Posts filed under ‘Education’

Wiping Your Financial Slate Clean

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 3, 2017). Subscribe on the right side of the page for the complete text.

The page on the calendar has turned, and we now have a new year, and will shortly have a new president, and new economic policies. Although there is nothing magical about starting a fresh, new year, the annual rites of passage also allow investors to start with a clean slate again and reflect on their personal financial situation. Before you reach a desired destination (i.e., retirement), it is always helpful to know where you have been and where are you currently. Achieving this goal requires filtering through a never-ending avalanche of real-time data flooding through our cell phones, computers, TVs, radios, and Facebook accounts. This may seem like a daunting challenge, but that’s where I come in!

Distinguishing the signals from the noise is tough and there was plenty of noise in 2016 – just like there is every year. Before the S&P 500 stock index registered a +9.5% return in 2016, fears of a China slowdown blanketed headlines last January (the S&P 500 fell -15% from its highs and small cap stocks dropped -26%), and the Brexit (British exit) referendum caused a brief 48-hour -6% hiccup in June. Oil was also in the news as prices hit a low of $26 a barrel early in the year, before more than doubling by year-end to $54 per barrel (still well below the high exceeding $100 in 2014). On the interest rate front, 10-Year Treasury rates bottomed at 1.34% in July, while trillions of dollars in global bonds were incomprehensibly paying negative interest rates. However, fears of inflation rocked bond prices lower (prices move inversely to yields) and pushed bond yields up to 2.45% today. Along these lines, the Federal Reserve has turned the tide on its near-0% interest rate policy as evidenced by its second rate hike in December.

Despite the abbreviated volatility caused by the aforementioned factors, it was the U.S. elections and surprise victory of President-elect Donald Trump that dominated the media airwaves for most of 2016, and is likely to continue as we enter 2017. In hindsight, the amazing Twitter-led, Trump triumph was confirmation of the sweeping global populism trend that has also replaced establishment leaders in the U.K., France, and Italy. There are many explanations for the pervasive rise in populism, but meager global economic growth, globalization, and automation via technology are all contributing factors.

The Trump Bump

Even though Trump has yet to accept the oath of Commander-in-Chief, recent investor optimism has been fueled by expectations of a Republican president passing numerous pro-growth policies and legislation through a Republican majority-controlled Congress. Here are some of the expected changes:

- Corporate/individual tax cuts and reform

- Healthcare reform (i.e., Obamacare)

- Proposed $1 trillion in infrastructure spending

- Repatriation tax holiday for multinational corporate profits

- Regulatory relief (e.g., Dodd-Frank banking and EPA environmental reform)

The chart below summarizes the major events of 2016, including the year-end “Trump Bump”:

While I too remain optimistic, I understand there is no free lunch as it relates to financial markets (see also Half Trump Full). While tax cuts, infrastructure spending, and regulatory relief should positively contribute to economic growth, these benefits will have to be weighed against the likely costs of higher inflation, debt, and deficits.

Over the 25+ years I have been investing, the nature of the stock market and economy hasn’t changed. The emotions of fear and greed rule the day just as much today as they did a century ago. What has changed today is the pace, quality, and sheer volume of news. In the end, my experience has taught me that 99% of what you read, see or hear at the office is irrelevant as it relates to your retirement and investments. What ultimately drives asset prices higher or lower are the four key factors of corporate profits, interest rates, valuations, and sentiment (contrarian indicator) . As you can see from the chart below, corporate profits are at record levels and forecast to accelerate in 2017 (up +11.9%). In addition, valuations remain very reasonable, given how low interest rates are (albeit less low), and skeptical investor sentiment augurs well in the short-run.

Source: FactSet

Regardless of your economic or political views, this year is bound to have plenty of ups and downs, as is always the case. With a clean slate and fresh turn to the calendar, now is a perfect time to organize your finances and position yourself for a better retirement and 2017.

Wade W. Slome, CFA, CFP®

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Searching for the Growth Stock Holy Grail

Remember Research in Motion (now Blackberry Limited – BBRY)? What about Krispy Kreme Doughnuts? How about Crocs (CROX)? Or maybe even Webvan, the online grocery delivery company that went bankrupt during the bursting of the dot-com bubble? These are all examples of once heralded growth companies that lost their mojo along their growth expansion ways.

Not every stock can grow to the $80+ billion market cap stratosphere like Apple Inc. (AAPL), Starbucks Corp. (SBUX), and Wal-Mart Stores (WMT), so finding companies with the right mixture of growth characteristics can be challenging. Objective stock market observers can disagree on the ingredients of a successful growth stock recipe, but generally speaking, the real explosive appreciation in stock prices come from those companies that can compound earnings growth over longer periods of time.

But how can one discover the Holy Grail of compounding earnings? At Sidoxia Capital Management, there are a handful of key factors we look for in successful growth companies. In the hyper-competitive global marketplace, these are crucial questions we want adequately answered before we invest our clients’ money:

- Does the company sell a product or service that cuts costs?

- Does the company offer a product or service with unique entertainment value?

- Does the company offer a superior product or service compared to its competitors?

Even if a target investment can affirmatively answer two or three of these questions, often the most important question is the following:

- Does the company have a sustainable competitive advantage in providing a product or service?

If the company does not have some type of durable competitive advantage, then some other company can just copy the product or service, and sell it at a lower price. This sadly leads to margin and P/E (Price-Earnings) multiple compression – both negative outcomes.

The aforementioned factors are not the end-all, be-all for successful growth stocks, but rather the minimum price of admission. Even if the previous criteria boxes are sufficiently checked off, the company being researched must still be fairly or attractively priced. For example, it doesn’t take a genius to figure out Apple is a successful company with unique advantages. More specifically, the company has $240 billion in cash, $50 billion in profits, and $215 billion in revenue. The real question becomes, is the stock fairly or attractively priced?

Although Apple appears attractively valued at current prices, in many other instances that is not the case. Often, great companies have been discovered by a large swath of investors, and therefore trade at significant premiums, which increases the risk profile or reduces the upside potential of the investment.

Sucking the Last Puff

If a company’s product or service isn’t superior, cut costs, or entertain at a reasonable/attractive valuation, then investing is like taking the last puff or drag out of a cigarette butt. Some value investors are good at this craft, but often these managers get caught into so-called “value traps” – ask Bill Ackman about Valeant Pharmaceuticals (VRX). Many value investors thought they found a bargain when they bought Valeant shares after it fell -80% in price. The stock subsequently has fallen another -50%…ouch!.

It’s worth noting that growth can come from many different areas. Even mature industries can produce periods of cyclical growth, however identifying cyclical winners is challenging. The art for the investment manager is determining whether growth in a target investment is sustainable. In many instances, companies temporarily benefit from a rising tide that lifts all boats, before the tide goes out and sinks fundamentals down to lower levels.

Growth investing can be a dangerous hobby for short-term traders because the price volatility stemming from ever-changing earnings growth expectations creates excessive trading, taxes, and transaction costs. However, for long-term investors, the great growth manager, T. Rowe Price, summed it up best here:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

Growth investing is both a science and an art, but does not require a degree in rocket science. If you can focus on the important growth criteria, and combine it with a long-term disciplined valuation process, you will be well on your way to discovering the growth stock Holy Grail.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in VRX, BBRY, SBUX, WMT, CROX, Krispy Kreme, Webvan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Time Arbitrage: Investing vs. Speculation

The clock is ticking, and for many investors that makes the allure of short-term speculation more appealing than long-term investing. Of course the definition of “long-term” is open for interpretation. For some traders, long-term can mean a week, a day, or an hour. Fortunately, for those that understand the benefits of time arbitrage, the existence of short-term speculators creates volatility, and with volatility comes opportunity for long-term investors.

What is time arbitrage? The concept is not new and has been addressed by the likes of Louis Lowenstein, Ralph Wanger, Bill Miller, and Christopher Mayer. Essentially, time arbitrage is exploiting the benefits of moving against the herd and buying assets that are temporarily out of favor because of short-term fears, despite healthy long-term fundamentals. The reverse holds true as well. Short-term euphoria never lasts forever, and experienced investors understand that continually following the herd will eventually lead you to the slaughterhouse. Thinking independently, and going against the grain is ultimately what leads to long-term profits.

Successfully executing time arbitrage is easier said than done, but if you have a systematic, disciplined process in place that assists you in identifying panic and euphoria points, then you are well on your way to a lucrative investment career.

Winning via Long-Term Investing

Legg Mason has a relevant graphical representation of time arbitrage:

Source: Legg Mason Funds Management

The first key point to realize from the chart is that in the short-run, it is very difficult to distinguish between gambling/speculating and true investing. In the short-run (left side of graph), speculators can make nearly as much profits as long-term investors. As famed long-term investor Benjamin Graham astutely states:

“In the short-run, the market is a voting machine. In the long-run, it’s a weighing machine.”

Or in other words, speculative strategies can periodically outperform in the short run (above the horizontal mean return line), while thoughtful long-term investing can underperform. Like a gambler/speculator dumping money into a slot machine in Las Vegas, the gambler may win in the short-run, but over the long-run, the “house” always wins.

Financial Institutions are notorious for throwing up strategies on the wall like strands of spaghetti. If some short-term outperforming products randomly stick, then financial institutions often market the bejesus out of the funds to unsuspecting investors, until the strategies eventually fall off the wall.

Beware o’ Short-Termism

I believe Jack Gray of Grantham, Mayo, Van Otterloo got it right when he said, “Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth.” What’s led to the excessive short-termism in the financial markets (see Short-Termism article)? For starters, technology and information are spreading faster than ever with the proliferation of the internet, creating a sense of urgency (often a false sense) to react or trade on that information. With 3 billion people online and 5 billion people operating mobile phones globally, no wonder investors are getting overwhelmed with a massive amount of short-term data.

Next, trading costs have also declined dramatically in recent decades to the point where brokerage firms are offering free trades on various products. Lower trading costs mean less friction, which often leads to excessive and pointless, profit-reducing trading in reaction to meaningless news (i.e., “noise”). Lastly, the genesis of ETFs (exchange traded funds) has induced a speculative fervor, among those investors dreaming to participate in the latest hot trend. Usually, by the time an ETF has been created, any exploitable trend has already been exploited. In other words, the low-hanging profit fruits have already been picked, making long-term excess returns tougher to achieve.

There is rarely a scarcity of short-term fears. Currently, concerns vary between Federal Reserve monetary policy, political legislation, Middle East terrorism, foreign exchange rates, inflation, and other fear-induced issues du jour. Markets may be overbought in the short-run, and/or an unforeseen issue may derail the current bull market advance. However, for investors who can put on their long-term thinking caps and understand the concept of time arbitrage, opportunistically buying oversold ideas and selling over-hyped ones should lead to significant profits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Waiting for the Fat Pitch

Fall is here and the leaves are beginning to change, which means it’s baseball playoffs time and the World Series is quickly approaching. Investing in some respects is similar to baseball because they both require discipline and patience. One investing legend who embodies those characteristics is Warren Buffett, and he has repeatedly spoken about Ted Williams and waiting for the “fat pitch.”

John Huber, over at BHI, did a great job summarizing Ted Williams’ hitting philosophy here:

“Ted Williams was famous for “waiting for the fat pitch”. He would only look to swing at pitches in the part of the strike zone where he knew he had a higher probability of getting a hit. There were parts of his strike zone where he batted .230 and there were other parts of the strike zone where he batted .400. He knew that if he waited for a pitch over the heart of the plate and didn’t swing at pitches in the .230 part of the strike zone—even though they were strikes—he would improve his odds of getting a hit and increase his overall batting average.”

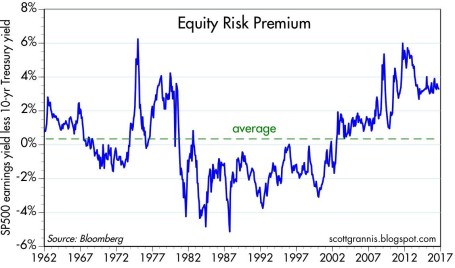

This lesson of patience and discipline is critical for your investment portfolio. Too many people speculate by chasing a hot tip or good stock story, or on the flip side, panic by selling based upon transitory negative news headlines. Today, we see risk aversion happening on steroids. Consider there is over $8 trillion sitting in savings accounts earning effectively nothing – the equivalent of stuffing money under the mattress (see also Invest or Die). In other words, investors are paying extremely high prices (chasing) for safer (less volatile) securities – bonds and cash, while equities are yielding a much higher rate as measured by the earnings yield of the S&P 500 (S&P operating profits / index value). Scott Grannis at Calafia Beach Pundit calls this dynamic the equity risk premium (chart below).

Source: Scott Grannis

As you can see from the chart, ever since the financial crisis occurred, stocks have been compensating investors at significantly higher levels (almost 4% currently) than the yields on 10-Year Treasury Notes, a phenomenon not experienced for the previous three decades.

When will this equity premium revert back towards the mean? There are number of factors that could correct this disparity.

1). The economy enters recession and profits decline to a point at which bonds offer a more compelling risk-reward ratio than stocks.

2). Interest rates rise (bond prices decline) to a point at which bonds offer a more compelling risk-reward ratio than stocks.

3). Investors bid stocks significantly higher to a point at which bonds offer a more compelling risk-reward ratio than stocks.

Most people are worried about scenario #1, but there is plenty objective data that splashes cold water on that view. Consider the unemployment rate has been chopped in half since 2009 with about 15 million jobs added; corporate profits are at/near record highs; auto sales are at/near record highs; home sales continue on an improving trajectory; and the yield curve remains positive, among other factors. If you absorb that information, it clearly doesn’t resemble a recessionary environment, but that doesn’t prevent people from worrying.

Regarding scenario #2, rising rates are an eventuality, but an absence of meaningful inflation, coupled with sluggish global growth are likely to keep a lid on interest rates for some time. Any casual observer would realize that interest rates have been on a downward trend for more than 35 years (see also Fall is Here: Change is Near). Even with a potential second rate increase in a decade initiated by the Fed this upcoming December, the long-term downward trend in rates will likely remain intact.

While the media likes to focus on the half-glass full scenarios (#1 & #2), very little time has been expended on the possibility of scenario #3, which contemplates a rise in stock prices to erase the discount in stock prices relative to bond prices (i.e., elevated equity risk premium).

While many people are ignoring the probability of scenario #3 occurring, like a disciplined hitter in baseball, successful investing requires patience while you wait for your fat investment pitch.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Sweating Your Way to Investment Success

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style. Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the international geopolitics and presidential elections. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

EBITDA: Sniffing Out the Truth

Financial analysts are constantly seeking the Holy Grail when it comes to financial metrics, and to some financial number crunchers, EBITDA (Earnings Before Interest Taxes Depreciation and Amortization – pronounced “eebit-dah”) fits the bill. On the flip side, Warren Buffett’s right hand man Charlie Munger advises investors to replace EBITDA with the words “bullsh*t earnings” every time you encounter this earnings metric. We’ll explore the good, bad, and ugly attributes of this somewhat controversial financial metric.

The Genesis of EBITDA

The origin of the EBITDA measure can be traced back many years, and rose in popularity during the technology boom of the 1990s. “New Economy” companies were producing very little income, so investment bankers became creative in how they defined profits. Under the guise of comparability, a company with debt (Company X) that was paying high interest expenses could not be compared on an operational profit basis with a closely related company that operated with NO debt (Company Z). In other words, two identical companies could be selling the same number of widgets at the same prices and have the same cost structure and operating income, but the company with debt on their balance sheet would have a different (lower) net income. The investment banker and company X’s answer to this apparent conundrum was to simply compare the operating earnings or EBIT (Earnings Before Interest and Taxes) of each company (X and Z), rather than the disparate net incomes.

The Advantages of EBITDA

Although there is no silver bullet metric in financial statement analysis, nevertheless there are numerous benefits to using EBITDA. Here are a few:

- Operational Comparability: As implied above, EBITDA allows comparability across a wide swath of companies. Accounting standards provide leniency in the application of financial statements, therefore using EBITDA allows apples-to-apples comparisons and relieves accounting discrepancies on items such as depreciation, tax rates, and financing choice.

- Cash Flow Proxy:Since the income statement traditionally is the financial statement of choice, EBITDA can be easily derived from this statement and provides a simple proxy for cash generation in the absence of other data.

- Debt Coverage Ratios:In many lender contracts, certain debt provisions require specific levels of income cushion above the required interest expense payments. Evaluating EBITDA coverage ratios across companies assists analysts in determining which businesses are more likely to default on their debt obligations.

The Disadvantages of EBITDA

While EBITDA offers some benefits in comparing a broader set of companies across industries, the metric also carries some drawbacks.

- Overstates Income: To Charlie Munger’s point about the B.S. factor, EBITDA distorts reality by measuring income before a bunch of expenses. From an equity holder’s standpoint, in most instances, investors are most concerned about the level of income and cash flow available AFTERaccounting for all expenses, including interest expense, depreciation expense, and income tax expense.

- Neglects Working Capital Requirements: EBITDA may actually be a decent proxy for cash flows for many companies, however this profit measure does not account for the working capital needs of a business. For example, companies reporting high EBITDA figures may actually have dramatically lower cash flows once working capital requirements (i.e., inventories, receivables, payables) are tabulated.

- Poor for Valuation: Investment bankers push for more generous EBITDA valuation multiples because it serves the bankers’ and clients’ best interests. However, the fact of the matter is that companies with debt or aggressive depreciation schedules do deserve lower valuations compared to debt-free counterparts (assuming all else equal).

Wading through the treacherous waters of accounting metrics can be a dangerous game. Despite some of EBITDA’s comparability benefits, and as much as bankers and analysts would like to use this very forgiving income metric, beware of EBITDA’s shortcomings. Although most analysts are looking for the one-size-fits-all number, the reality of the situation is a variety of methods need to be used to gain a more accurate financial picture of a company. If EBITDA is the only calculation driving your analysis, I urge you to follow Charlie Munger’s advice and plug your nose.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Sky is Falling?

Investors reacted like the sky was falling on Friday. Commentators mostly blamed the -400 point decline in the Dow on heightened probabilities for a September rate hike by Janet Yellen and her fellow Federal Reserve colleagues. Geopolitical concerns over a crazy dictator in North Korea with nuclear weapons were identified as contributing factors to frazzled nerves.

The real question should be, “Are these stories complete noise, or should I pay close attention?” For the vast majority of times, the response to questions like these should be “yes”, the media headlines are mere distractions and you should simply ignore them. During the last rate hike cycle from mid-2004 to mid-2006, guess how many times the Fed raised rates? Seventeen times! And over those 17 rate hikes, stocks managed to respectably rise over 11%.

So far this cycle, Yellen and the Fed have raised interest rates one time, and the one and only hike was the first increase in a decade. Given all this data, does it really make sense to run in a panic to a bunker or cave? Whether the Fed increases rates by 0.25% during September or Decemberis completely irrelevant.

If we look at the current situation from a slightly different angle, you can quickly realize that making critical investment decisions based on short-term Federal Reserve actions would be foolish. Would you buy or sell a house based solely on this month’s Fed policy? For most, the answer is an emphatic “no”. The same response should hold true for stocks as well. The real reason anyone should consider buying any type of asset, including stocks, is because you believe you are paying a fair or discounted price for a stream of adequate future cash flows (distributions) and/or price appreciation in the asset value over the long-term.

The problem today for many investors is “short-termism.” This is what Jack Gray of Grantham, Mayo, Van Otterloo and Company had to say on the subject, “Excessive short-termism results in permanent destruction of wealth, or at least permanent transfer of wealth.” I couldn’t agree more.

Many people like to speculate or trade stocks like they are gambling in Las Vegas. One day, when the market is up, they buy. And the other day, when the market is down, they sell. However, those same people don’t wildly speculate with short-term decision-making when they buy larger ticket items like a lawn-mower, couch, refrigerator, car, or a house. They rationally buy with the intention of owning for years.

Yes, it’s true appliances, vehicles, and homes have utility characteristics different from other assets, but stocks have unique utility characteristics too. You can’t place leftovers, drive inside, or sit on a stock, but the long-term earnings and dividend growth of a diversified stock portfolio provides plenty of distinctive income and/or retirement utility benefits to a long-term investor.

You don’t have to believe me – just listen to investing greats like Warren Buffett:

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio’s market value.”

The common sense test can also shed some light on the subject. If short-term trading, based on the temperature of headlines, was indeed a lucrative strategy, then the wealthiest traders in the world would be littered all over the Forbes 100 list. There are many reasons that is not the case.

Even though the Volatility Index (aka, “Fear Gauge” – VIX) spiked +40% in a single day, that does not necessarily mean stock investors are out of the woods yet. We saw similar volatility occur last August and during January and June of this year. At the same time, there is no need to purchase a helmet and run to a bunker…the sky is not falling.

Other related article: Invest with a Telescope…Not a Microscope

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Growth Stocks – Cheaper by the Day

Are you a value investor? If you said “yes,” how would you feel about buying an $18 stock with a P/E (Price/Earnings) ratio of greater than 100x and a Price/Sales ratio of 14x for a company that three years earlier was started in a garage? This may not sound like a value stock, but had you bought this stock at the initial public offering (IPO), it would have been a screaming bargain – priced at less than 1x P/E ratio, based on this year’s earnings estimates.

You may be surprised to know, this company with a meager $18 IPO share price is now worth $9,192 per share today (if you adjust for three stock splits)! Yes, that’s correct, a +50,900% return. If you are wondering to which stock I’m referring, I am talking about Amazon.com Inc. (AMZN). Incredibly, ever since Amazon went public in 1997, the CEO Jeff Bezos has managed to command the start-up e-commerce company from $31 million in revenues to $121 billion (with a “b”) on an annual basis in 2016 (a +389,000% increase).

Discovering the next IPO that turns into a $363 billion behemoth is easier said than done, and unfortunately these types of companies are a rare breed. Even if you are lucky enough to identify these diamonds-in-the-rough, early in their growth cycle, very few investors have the fortitude and discipline to continually own the stocks through the perpetual volatility (i.e., peaks and valleys).

The good news is, although you may be unable to find every unicorn out there, you can still apply the same principles and characteristics to any growth stock you invest in. In order to prudently achieve outsized returns, one must identify innovative market leaders that have gained some type of sustainable competitive advantage, which will serve as the profit and cash flow growth engine for the stock over the long-term.

If a company does not have a unique advantage over industry competitors, they will likely be unable to compound earnings growth – the key to becoming a big winner. Albert Einstein, Nobel Prize winner is credited with identifying compounding as the “eighth wonder of the world,” and without compounding there will be no gigantic results.

Amazon may be a rare breed, but there are plenty of other examples of so-called “expensive” stocks that get dismissed or fall through the cracks as they explode in value to the stratosphere. Consider Starbucks Corp. (SBUX), which at the time of its IPO in 1992 was priced at a very rich P/E of 52x. Sound expensive? Actually, this was a greatest offer in a generation. Adjusted for stock splits, the IPO shares were valued at $0.27 – in the most recent trading session Starbucks shares closed at $55.90, a +20,600% increase. Similar to Amazon, had you purchased Starbucks shares at the IPO price, you would have been paying less than a measly, eye-popping 1x P/E ratio based on 2016 earnings.

Alphabet Inc. (GOOGL), formerly Google Inc., is another case of growth stock appearing pricey on the outside, but really a value of a lifetime on the inside. The hype surrounding the Google IPO was so palpable in 2004, the stock priced at a relatively nose-bleed level of 60x P/E level, approximately. The unconventional auction bidding method to buy the initial shares made investors even more skeptical. Suffice it to say, the greater than +1,600% gain has once again shown that investors can reap handsome rewards, if they do thorough enough due diligence and ignore the illusory big ticket IPO prices.

What most investors fail to realize is that P/E ratios are temporary. By purchasing a growth stock, the numerator of the P/E ratio (price) becomes static or fixed. As earnings of a growth company expand, the stock becomes cheaper by the day. More specifically, the numerator of the P/E (price) is flat, while the denominator (earnings) grows, thereby making the P/E ratio smaller (cheaper). And as you can see from the few previous examples I have provided, if you are able to identify winners, and hold them long enough, you will eventually realize the initial hefty price tag at purchase will be considered almost free after all the earnings compounding.

Legendary growth investor Peter Lynch summed it up concisely when he noted, “People concentrate too much on the P, but the E really makes the difference.” Lynch goes on to highlight the importance of patience in growth investing because stocks often go down or move sideways for long periods of time before dramatic increases occur:

“My best stocks performed in the 3rd year, 4th year, 5th year, not in the 3rd week or 4th week.”

I’ve illustrated a few successful examples of meteoric growth stocks, but more importantly the misconception many investors place on the current P/E ratio. There still is no substitute for hard-nosed, detailed fundamental research for finding big growth winners, because true growth stocks bought and held for a long enough period, will become cheaper by the day. If you don’t have the time, discipline, or patience to execute this winning strategy, find and hire an experienced investment manager who understands these concepts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AMZN, and GOOGL, but at the time of publishing had no direct position in SBUX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Politics & Your Money

Will you be able to retire, and what impact will the elections have on your financial future? Answering these questions can be a scary endeavor. And unless you have been living in a cave, you may have noticed we are in the middle of a heated U.S. presidential election campaign between Donald Trump and Hillary Clinton. Regardless of which side of the political fence you stand on, the prospects of your retirement are much more likely to be impacted by your personal actions than by the actions of Washington politicians.

Even if you despise politics and were living in a cave (with WiFi access), there’s a high probability you would be overloaded with detailed and dogmatic online editorials from overconfident Facebook friends. Besides offering self-assured predictions, these impassioned political pleas generally itemize the top 10 reasons your favorite candidate is a moron, and another 10 reasons why their candidate is the greatest.

Your friends’ opinions may have pure intentions, but unfortunately, rarely, if ever, do their thoughts alter your views. A reference from a recent Legal Watercooler article summed it up best:

“Political Facebook rants changed my mind…said nobody, ever.”

Nearly as ineffectual as political Facebook opinions on your politics is the ineffectual influence of presidential elections on your finances. For example, over the last four decades, stock prices have gone up and down during both Republican and Democrat presidential terms. The picture looks much the same, if you analyze the fiscal performance of conservatives and liberals since 1970 – debt burdens as a percentage of economic output have risen and fallen under both political parties. No matter who wins the presidency, many investors forget the ability of that individual to affect change is highly dependent upon the political balance of power in Congress. If Congress holds a split majority in the House and Senate, or the opposition party commands the entire Congress, then the winning presidential candidate will be largely neutered.

Rather than panic over a political loss or celebrate a candidate’s victory, here are some tangible actions to improve your finances:

- Organize. Typically individuals have investment and saving accounts scattered with no cohesive accounting or strategy. Get your financial house in order by gathering and organizing all your accounts.

- Budget. Spend less than you take in. Or in other words…save. You can achieve this goal in one of two ways – cut your spending, or increase your income.

- Create a Plan. When do you plan to retire? How much money do you need for retirement? What asset allocation and risk profile should you adopt to meet your financial goals?

If you have difficulty with any of these actions, then meet with an experienced financial professional to assist you.

Politics can trigger very emotional responses. However, realizing your actions have a much more direct impact on your finances than political Facebook rants and temporary elections will benefit you in achieving your long-term financial goals.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds and FB, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Technical Analysis – Astrology or Lob Wedge?

Investing comes in many shapes and sizes. And like religion (see Investing Religion article), most investment strategies are built on the essential belief that following certain rules and conventions will eventually lead to profit enlightenment. When it comes to technical analysis (TA), a discipline used with the principal aim of predicting future prices from past patterns, some consider it a necessity for making money in the market. Others, regard the practice of TA as a pseudoscience, much like astrology.

I feel there is a proper place for TA on selective basis, which I will describe later, but for the most part I agree with some of the legendary investors who have chimed in on the subject:

Warren Buffett: “I realized technical analysis didn’t work when I turned the charts upside down and didn’t get a different answer.”

Peter Lynch: “Charts are great for predicting the past.”

Technical Analysis Linguistics

Fundamental analysis, the antithesis of technical analysis, strives to predict future price direction by analyzing facts and data surrounding a company, industry, and/or economy. It too comes with its own syntax and versions, for example: value, growth, top-down, bottom-up, quantitative, etc.

I do not claim to be a TA expert, however in my many years of investing I have come across a smorgasbord of terms and flavors surrounding the discipline. Describing and explaining the density of material surrounding TA would encompass too large of a scope for this article, but here are some prevalent terms one should come to grips with if you want to become a technical analysis guru:

Technical Analysis Approaches

- Elliot Wave

- Relative strength / Momentum (see Momentum Investing article)

- MACD (Moving Average Convergence / Divergence)

- Fibonacci retracement

- Dow Theory

- Stochastics

- Bollinger bands

Price Patterns

- Head and shoulders

- Double bottom

- Cup and handle

- Channels

- Breakouts

- Pivot points

- Candlesticks

- Resistance/Support

- Dead cat bounce (my personal favorite)

Each of these patterns are supposes to provide insight into the future direction of price. At best, I would say the academic research surrounding the subject is “inconclusive,” and at worst I’d say it’s considered a complete “sham.”

The Lob Wedge

As I’ve stated earlier, I fall in the skeptical camp when it comes to TA, since fundamental analysis is the main engine I use for generating and tracking my investment ideas. For illustrative purposes, you may consider fundamental analysis as my group of drivers and irons. I do, however, utilize selective facets of TA much like I use a lob wedge in golf for a limited number of specific situations (e.g., shots over high trees, downhill lies, and fast greens). When it comes to trading, I do believe there is some value in tracking the relationship of extreme trading volume (high or low), especially when it is coupled with extreme price movement (high or low). The economic laws of supply and demand hold true for stock trades just as they do for guns and butter, and sharp moves in these components can provide insights into the psychological mindset of investors with respect to a security (or broader market). Beyond trading volume, there are a few other indicators that I utilize as part of my trading strategies, but these tactics play a relatively minor role, since most of my core positions are held on a multi-year time horizon.

Overall, there is a stream of wasteful noise, volatility, and misinformation that permeates the financial markets on a daily basis. A major problem with technical analysis is the many false triggered signals, which in many cases lead to excessive trading, transaction costs, and ultimately subpar investment returns. Although I remain a skeptic on the subject of technical analysis and I may not read my horoscope today, I will continue to keep a lob wedge in my golf bag with the hopes of finding new, creative ways of using it to my advantage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own exchange traded funds and various securities, including BRK.B, but at time of publishing had no direct position in BRK.A or any company mentioned in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}