Posts filed under ‘derivatives’

Quickly Out of the Gate

The race into 2024 has begun, and the U.S. market is off to a quick start. The S&P 500 jumped out of the gates by +1.6%, and the technology and AI (Artificial Intelligence) – heavy NASDAQ index raced out by +1.2%. The bull market rally broadened out at the end of 2023, but 2024 returned to the leaders of last year’s pack, the Magnificent 7 (see also Mission Accomplished). Out front, in the lead of the Mag 7, is Nvidia with a +24% gain in January.

Inflation dropping (see chart below), the Federal Reserve signaling a decline in interest rates, low unemployment (3.7%), and healthy economic growth (+3.3% Q4 – GDP) have all contributed to the continuing bull market run.

Source: Yardeni.com

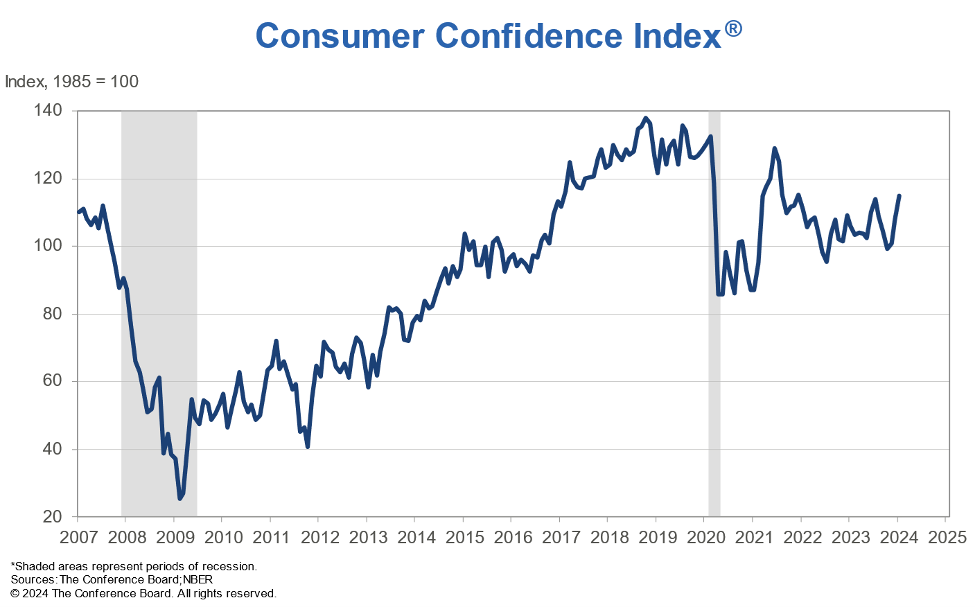

Consumer spending is the number one driver of economic growth, and consumers remain relatively confident about future prospects as seen in the recently released Conference Board Consumer Confidence numbers released this week (see chart below).

Source: Conference Board

But the race isn’t over yet, and there are always plenty of issues to worry about. The world is an uncertain place. Here are some of the concerns du jour:

– Red Sea conflict led by the Yemen-based, rebel group, Houthis

– Gaza war between Israel and Hamas

– Anxiety over November presidential election

– Ukraine – Russia war

Money Goes Where It is Treated Best

There are plenty of domestic concerns regarding government debt, deficit levels, and political frustrations on both sides of the partisan aisle remain elevated. When it comes to the financial markets, money continues to go where it is treated best. Sure, we have no shortage of problems or challenges, but where else are you going to put your life savings? China? Europe? Russia? Japan?

Well, as you can see in the chart below, anti-democratic, anti-American business, and confrontational military policies instituted by China have not benefitted investors – the U.S. stock market (S&P 500) has trounced the Chinese stock market (MSCI) over the last 30 years.

Source: Calafia Beach Pundit

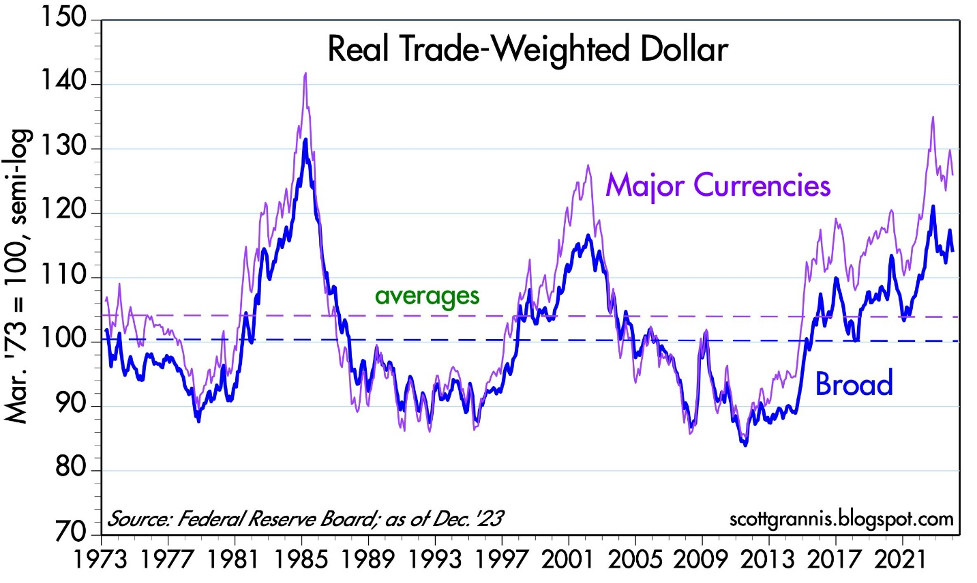

For years, market critics and pessimists have been screaming doom-and-gloom as it relates to the United States. The story goes, the U.S. is falling apart, government spending and debt levels are out of control, politicians are corrupt, and we’re going into recession, thanks in part to higher interest rates and inflation. Well, if that’s the case, then why has the value of the U.S. dollar increased over the last 10 years (see chart below)? And why is the stock market at all-time record-highs?

Source: Calafia Beach Pundit

Global investors are discerning in which countries they invest their hard-earned money. Global capital will flow to those countries with a rule of law, financial transparency, prudent tax policy, lower inflation, higher profit growth, lower interest rates, sensible fiscal and monetary policies, among other pragmatic business practices. There’s a reason they call it the “American Dream” and not the “Chinese Dream.” Our capitalist economy is far from perfect, but finding another country with a better overall investing environment is nearly impossible. There’s a reason why venture capitalists, private equity managers, sovereign wealth funds, hedge funds, and foreign institutions are investing trillions of their dollars in the United States. Money goes where it is treated best!

As money sloshes around the world, the 2024 investing race has a long way before it’s over, but at least the stock market has quickly gotten out of the gate and built a small lead.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2024). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia Webinar: The Keys to ’23 & What’s in Store for ’24 – Market Update

Unlock valuable insights at our upcoming webinar:

The Keys to ’23 & What’s in Store for ’24!

Tuesday, January 30th at 12:00 PM

Click the Zoom link below to register:

https://sidoxia.link/Webinar-Registration

Don’t miss out on the latest trends and expert discussions.

We will delve into a comprehensive market update. Register now!

The Douglas Coleman Show Interviews Wade Slome

Wade Slome, President and Founder of Sidoxia Capital Management, recently had the pleasure of being featured on The Douglas Coleman Show hosted by Douglas Coleman.

Drawing from professional and personal life lessons, Wade shares his knowledge about navigating market trends, building investment strategies, and also discuss the books he has authored.

If you are interested in learning more about the books Wade has authored, please visit: https://www.sidoxia.com/wades-books

This Baby Bull Has Time to Grow

You may have witnessed some fireworks on New Year’s Eve, but those weren’t the only fireworks exploding. The last two months of 2023 finished with a bang! More specifically, over this short period, the S&P 500 index skyrocketed +13.7%, NASDAQ +16.8%, and the Dow Jones Industrial Average +14.0%. The gains have been even more impressive for the cheaper, more interest-rate-sensitive small-cap stocks (IJR +21.8%), which I have highlighted for months (see also AI Revolution).

For the full year, the bull market was on an even bigger stampede: S&P 500 +24%, NASDAQ +43%, and Dow +14%.

Although 2023 closed with a festive explosion, 2022 ended with a bearish growl. Effectively, 2023 was a reverse mirror image of 2022. In 2022, the stock market fell -19% (S&P) due to a spike in inflation. Directionally, interest rates followed inflation higher as the Fed worked through the majority of its 0% to 5.5% Federal Funds rate hiking cycle.

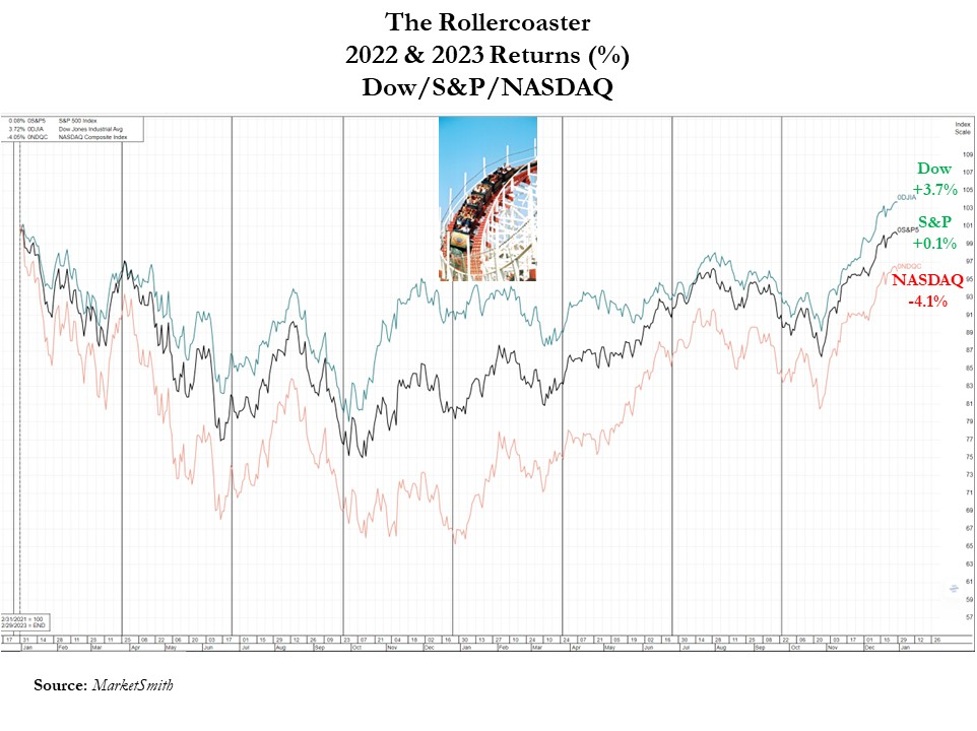

To sum it up simply, the last two years have been like riding a rollercoaster. For the year just ended, much of the year felt like a party, but 2022 felt more like a funeral. When you add the two years together, it was more of a lackluster result. For 2022-2023 combined, results registered at a meager +0.1% for the S&P, +3.7% for the Dow, and -4.0% for the NASDAQ (see chart below).

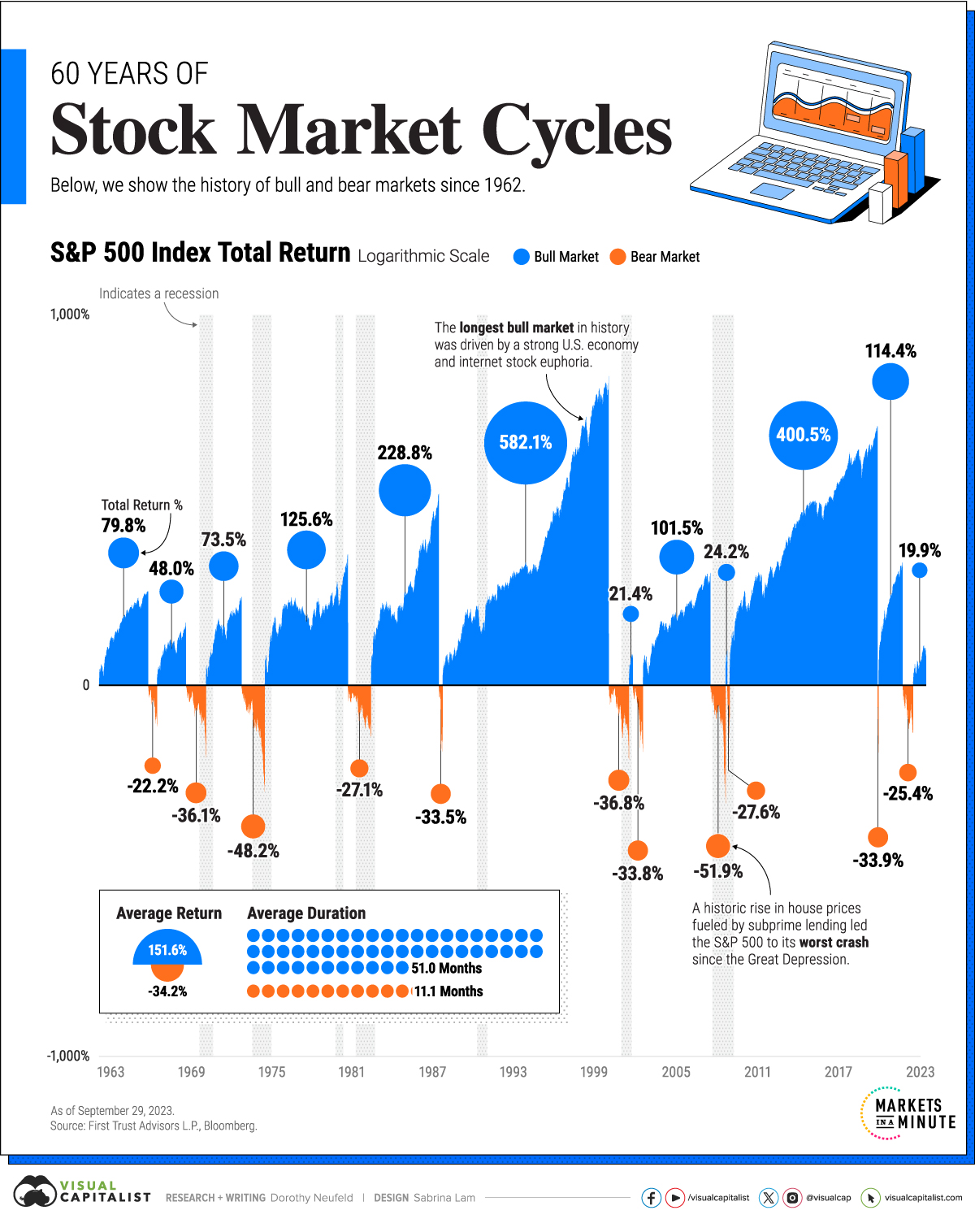

For those saying the good times of 2023 cannot continue, investors should understand that history paints a different picture. As you can see from the stock market cycles chart (below) that spans back to 1962, the average bull market lasts 51 months (i.e., 4 years, 3 months), while the average bear market persists a little longer than 11 months. This data suggests the current one-year-old baby bull market has plenty of room to grow more.

Source: Visual Capitalist

Why So Bullish?

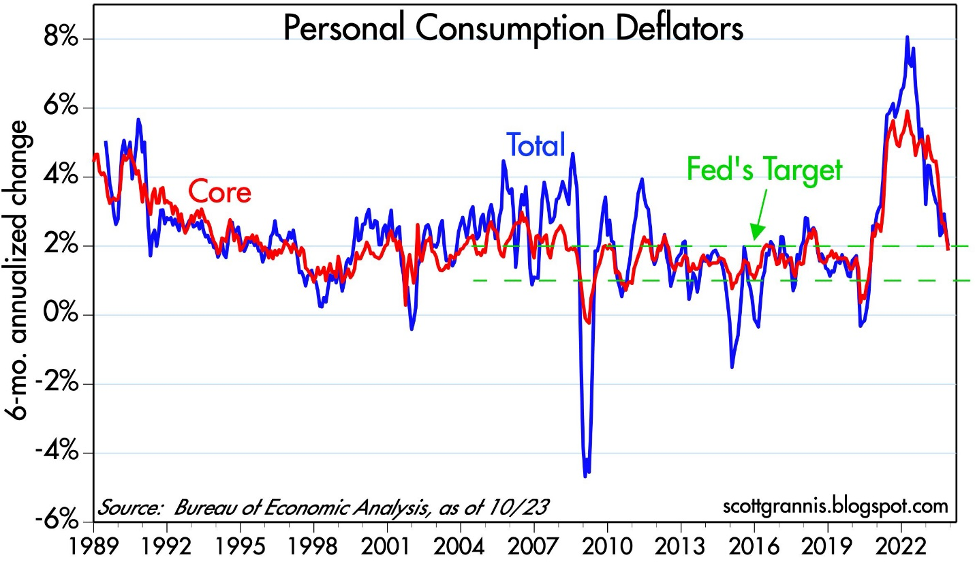

What has investors so jazzed up in recent months? For starters, inflation has been on a steady decline for many months. With China’s stagnating economy, it has helped our inflationary cause by exporting deflationary goods to our country. As you can see from the Personal Consumption Deflator chart below, this broad inflation measure has declined to the Federal Reserve’s 2% target level. Jerome Powell, the Federal Reserve Chairman has been paying attention to these statistics, as evidenced by the central bank’s forecast at the Fed’s recent policy meeting last month on December 13th for three interest rate cuts in 2024. This so-called “Powell Pivot” is a reversal in tone by the Fed, which had been on a relentless rampage of interest rate hikes, over the last two years.

Source: Calafia Beach Pundit

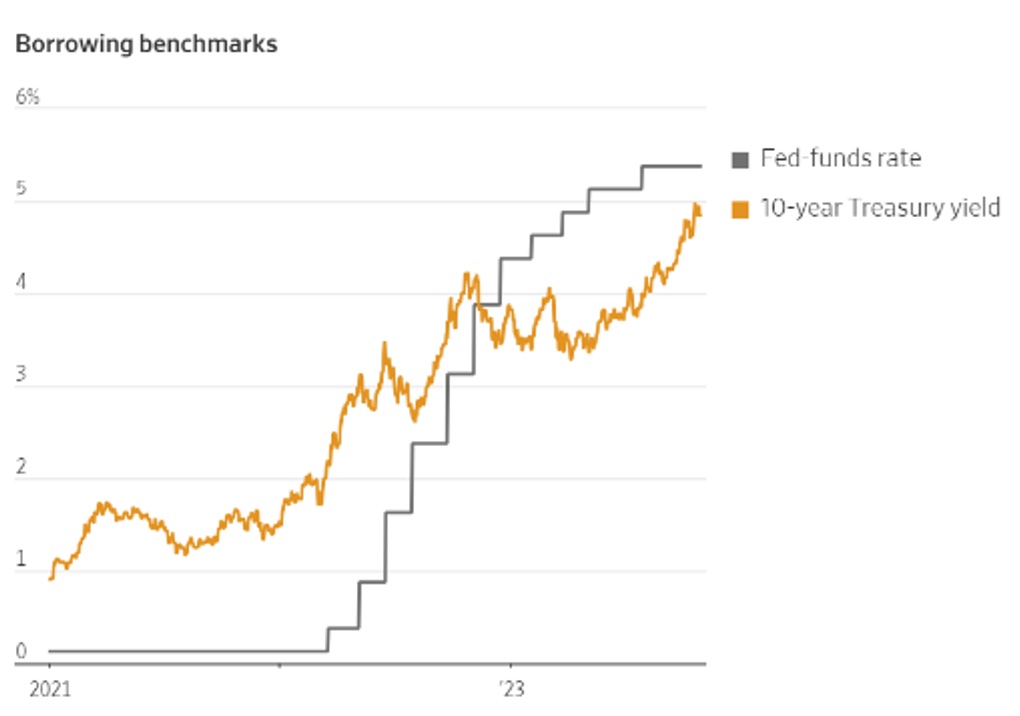

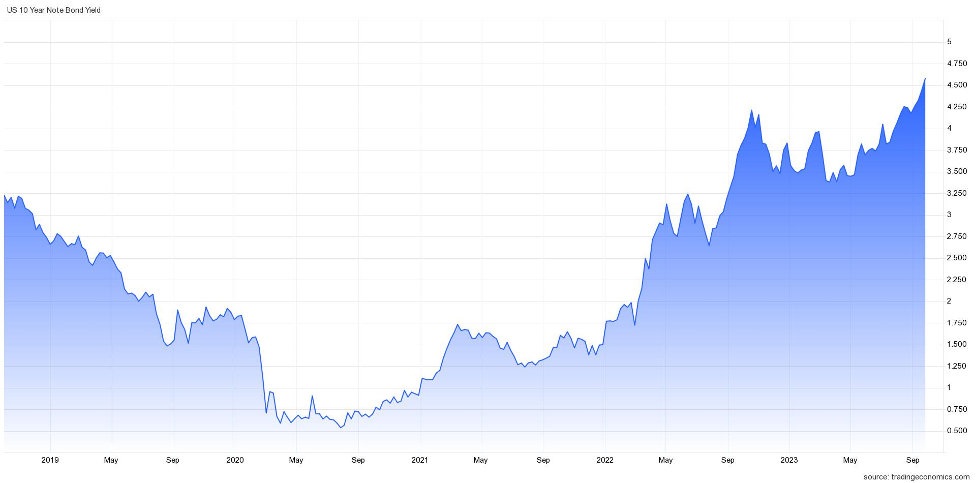

This interest rate cycle headwind has turned into a tailwind as investors now begin to discount the probability of future rate cuts in 2024. The relief of lower interest rates can be felt immediately, whether you consider declining mortgage and car loan rates for consumers, or credit line and corporate loan rates for businesses. This trend can be seen in the benchmark 10-Year Treasury Note yield, which has declined from a peak of 5.0% a few months ago to 3.9% today (see chart below).

Source: Trading Economics

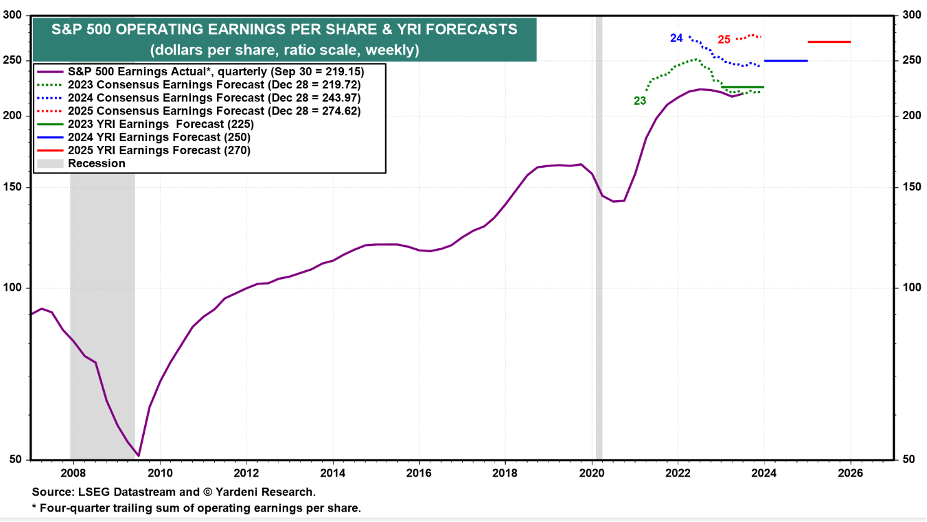

Declining inflation and interest rates explain a lot of investor optimism, but there are additional reasons to be sanguine. The economy remains strong, unemployment remains low, AI (Artificial Intelligence) applications are improving worker productivity, trillions of potential stock market dollars remain on the sidelines in money market accounts, and corporate profits have resumed rising near all-time record levels (see chart below).

Source: Yardeni.com

What could go wrong? There are always plenty of unforeseen issues that could slow or reverse our economic train. Geopolitical events in Russia or the Middle East are always difficult to predict, and we have a presidential election in 2024, which could always negatively impact sentiment. This new bull market had a great start in 2023, but in historical terms, it is only a baby. Time will tell if 2024 will make this baby cry, but whatever the market faces, declining inflation and interest rates should act as a pacifier.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 2, 2024). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

No Market Roar Due to War

The devastating damage to humanity from the Israeli-Hamas war that is in and around the Gaza strip should not be diminished or understated – innocent lives on both sides suffer in any conflict. However, the economic impact should not be overstated either. In other words, the hundreds of billions of dollars in financial stock market losses this month are not proportional to the Mideast economic losses incurred thus far.

To put the events in perspective, the population of Israel approximates 10 million people and the population located in the Gaza Strip is about two million people. There are more than eight billion people on the planet, so Israel/Gaza represents roughly 1/7 of 1% of the global population.

From an economic standpoint, the combined economic output of Israel/Gaza Strip accounts for around ½ of 1% of global GDP (see chart below – small slivers in the blue section).

And let’s not forget, economic activity is not dropping to zero. From an economic standpoint, the war’s financial impact is even smaller – a rounding error.

Source: Visual Capitalist

However, wars do not exist in a vacuum, and tensions in the Middle East have the potential of having a ripple effect. Whenever rumblings occur in the Mideast, one of the largest global sectors to be first impacted is the oil market. Approximately 20-30% of the world’s oil is trafficked through the Strait of Hormuz in the Persian Gulf, so it was not surprising to see a short-term spike in oil prices to almost $90 per barrel in early October after the Gaza invasion of Israel. By the end of the month, oil has settled back down to about $81 per barrel, almost precisely the same price right before the war started. On a year-over-year basis, oil prices are actually down approximately -5%, thereby providing minor relief to gas-powered car drivers.

If Iran, or Iran-backed militant group Hezbollah, throws their hat into the Israel-Hamas war ring, the U.S. and other Western allies may retaliate and escalate tensions in the region, which would unlikely be received well by the financial markets.

As a result of these domino effect fears in the region, the stock market took another leg down last month with the S&P 500 index declining -2.2%, the Dow Jones Industrial Average -1.4%, and the NASDAQ index fell the most, -2.8%. The world is a dangerous place, but we have seen this movie before – this is nothing new. We would all prefer world peace, but unfortunately, wars and skirmishes have gone on for centuries.

As Interest Rates Soar, Bonds Offer More

Source: Wall Street Journal

No, TINA is not the name of my high school girlfriend or wife, but rather the acronym TINA (There Is No Alternative) existed in recent years during the Federal Reserve’s zero-interest rate policy days. More specifically, TINA referred to the lack of investment alternatives to equities (i.e., stocks) when money effectively earned 0% in the bank and close-to-0% in many fixed income securities (i.e., bonds). In fact, at one point, although it is still hard to believe, there were more than $16 trillion in bonds paying negative interest rates – pure insanity.

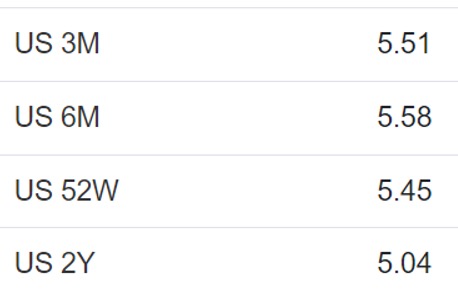

TINA Turns into FIONA

Given the large increase in interest rates by the Federal Reserve over two years (from 0% to 5.50%), investors have been given a short-term gift. As you can see from the chart above, yields on 10-Year Treasury Notes have risen to almost 5.0%. And believe it or not, shorter term bonds are currently providing yields even higher than this. The three-month, six-month, one-year, and two-year Treasuries are all yielding higher rates than 10-Year Treasury yields (i.e., inverted yield curve) – see table below. So, TINA has changed to FIONA – Fixed Income Opens New Alternatives. What’s more, for individuals with taxable accounts, the interest earned on Treasuries is tax-free at the state level, thereby making this short-term gift in yields even more attractive for investors.

Source: Trading Economics

Stock prices were down again for the month, and investment sentiment has been souring due to the war in the Middle East, but there is still plenty of reasons to remain constructive. Not only is the economy strong (e.g., 3rd quarter GDP of +4.9%), but the consumer also remains strong (see Consumer Wallets Strong) in large part because the unemployment rate remains near record lows (+3.8%). While anxiety rises due to the war, stock prices get cheaper, and opportunities increase. And although interest rates remain elevated, the Federal Reserve is signaling they are closer to a rate hiking end, inflation is cooling and FIONA is offering more attractive yields than during the TINA era. It’s true, this month stocks did not roar due to the war, but patient and opportunistic investors will be rewarded with more.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 1, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Consumer Wallets Strong, Rate Hikes Long, What Could Go Wrong?

Consumer wallets and balance sheets remain flush with cash as employment remains near record-high levels. Cash in consumer wallets and money in the bank help the economy keep chugging along at a healthy clip. More specifically, as you can see in the chart below, the net worth of U.S. households has reached a record $154.3 trillion dollars in the most recent month, thanks to appreciation in stocks, gains in real estate, and relatively stable levels of debt.

Source: Calafia Beach Pundit

Unemployment Remains Low

In addition, the unemployment rate is sitting at 3.8%, near multi-decade lows (see chart below).

Source: Trading Economics

As long as consumers continue to hold a job, they will continue spending to buoy economic activity – remember, consumer spending accounts for roughly 70% of our country’s economic activity. Case in point are the most recently released GDP (Gross Domestic Product) forecasts by the Atlanta Federal Reserve, which show 3rd quarter GDP growth estimated at a 4.9% rate (see chart below).

Rates Up, Housing Prices Up?

Yes, it’s true, despite a dramatic surge in mortgage rates over the last few years, the housing market remains strong due to a very tight supply of homes available for sale. Most homeowners with a mortgage have refinanced to a rate in the range of 3% (or in some cases even lower), so selling and moving into a new home with a mortgage at current rates of 7.3% is not that appealing. In other words, if you decide to move, your monthly mortgage payment could potentially go up by more > 50%, which could equate to thousands of dollars per month. Under this scenario, you are likely to stay put and not sell your home.

Source: Trading Economics

The embedded economic disincentive of selling a home with a mortgage has really put a real crimp on the supply of homes available for sale (chart below). As you can see, the inventory of homes has dramatically collapsed from a peak of about four million homes, circa the 2008 Financial Crisis, to around one million homes today.

Source: Trading Economics

In the face of this mixed data, the stock market finished a hot summer with a cool whimper last month, in large part due to a 0.49% increase in the 10-Year Treasury Note yield to 4.58% (see chart below). The S&P 500 index fell -4.9% for the month, the technology-heavy NASDAQ index dropped even further by -5.8%, while the Dow Jones Industrial Average outperformed, down -3.5% for the month. Worth noting, however, the Dow has significantly underperformed the other indexes so far this year.

Source: Trading Economics

Inflation on the Mend

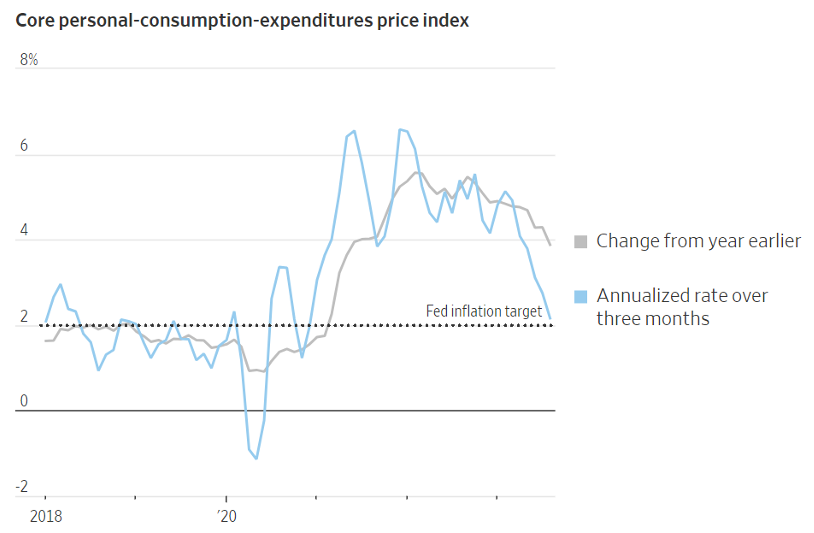

The Fed continues to talk tough about fighting inflation after taking interest rates from 0% to 5.5% over the last two years, nevertheless inflation continues to come down. The Fed’s go-to Core PCE inflation datapoint that came out last Friday at +0.1% is consistent with the downward inflation trend we have been witnessing for many months now (see chart below). As you can see, inflation on annualized basis has reached 2.2%, nearly achieving the Federal Reserve’s target of 2.0%.

Source: The Wall Street Journal and Commerce Department

There is never a shortage of investor concerns. Today, worries include Federal Reserve policy; restarting of school loan repayments (after a three-year hiatus); a potential government shutdown; an auto and Hollywood strike; higher oil prices; and a presidential election that is heating up. Many of these worries are nothing new. The bull market took a pause for the month, but consumer wallets remain fat, the economy keeps chugging, the employment picture remains strong, and stock prices remain up +12% for the year (S&P 500). For the time being, betting on a soft economic landing over an imminent recession could be a winning use for that cash in your wallet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 2, 2023). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Getting Paid to Eat Bon-Bons and Sell Options

I have a diverse set of interests, and two of my passions include eating assorted bon bons, and buying stocks low (selling them high). The only thing better than that is to also get paid for doing those same activities. Until I get paid for competing on the national bon bon competitive eating circuit, I’ll stick to getting paid for selling (“writing”) options.

The Mechanics of Option Writing

There are many places to learn about the basics of options, but for simplicity purposes think of options as tools for speculating, hedging, and generating income. Unfortunately, most people trading options lose money because of speculation and numerous shortcomings. Like guns, knives, or any other weapon, if properly used, these self-defense option tools can provide owners with significant benefits. If however the weapons are used irresponsibly, the consequences can be deadly. The same principles apply to options investing – beneficial in the right hands, disastrous in the wrong hands (see also Butter Knife or Cleaver article).

A Pricey Option Illustration

In order to illustrate the mechanics of option writing, let’s use Priceline.com Inc. (PCLN) as an example:

Suppose I did my in-depth fundamental research on Priceline and upon completion of my due diligence I realized that the stock is fairly valued at its current share price of $529. However, upon further consideration I realize I would love to buy 100 shares at a discount price of $500 if Priceline shares pulled back. In mirror-like fashion my fundamental valuation process may also indicate an adequate selling valuation level at a $560 premium.

Based on these previous assumptions, I could profitably sell (“write”) one naked put option with a strike price of $500 and an expiration date in October (approximately five months from today), in exchange for $3,560 in upfront cash less comissions.* That’s right, someone is going to pay me thousands of dollars to buy something I am openly willing to purchase at lower prices anyway. In bon bon terminology, speculators are paying me to eat bon bons, an activity I love even without upfront cash payments from others. In the case of an escalating Priceline share price, I prefer to sell covered calls (i.e. own underlying stock position plus simultaneously selling a call option), consistent with my valuation sell price targets (strik price of $560 per share).

Selling Insurance

Since writing options is effectively like selling insurance, it intuitively follows the best time to sell insurance is when people (investors) are the most nervous. If you were a fire insurance carrier and wanted to maximize collections, setting prices a week after a large fire in the hot, dry summer season around the firework-laden 4th of July may not be a bad choice. In the equity markets, the VIX (Volatility Index) is often referred to as the “fear gauge,” which can be used as an indicator to optimize premium collections from options sales.

Options, which are part of the derivatives family, get lumped into these wide set of financial instruments that billionaire investor Warren Buffett called “weapons of mass destruction.” The ironic part of that whole situation is that despite the evil titling of these instruments, Buffett has used these “weapons of mass destruction” extensively, more recently with his strategies related to selling index options – see Insurance Weapons of Mass Destruction. For those who followed the financial crisis of 2008-2009, observers fully realize that American International Group (AIG) was selling insurance on credit defaults (Credit Default Swaps). Regrettably, the CDS market was not regulated to a similar extent as the more sophisticated options and futures market.

Eating bon bons for pay can be satisfying, and so can trading stocks for cash, when buying them low and selling them high. On the other hand, these same activities can prove to be harmful if abused or misused. If you eat bon bons in moderation, and receive premiums from thoroughly researched naked puts and covered calls, then you have nothing to worry about.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: *Based on 5-9-11 closing trade data from Yahoo Finance. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in PCLN, AIG, VXX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ball & Chaining the Rating Agencies

After sifting through the rubble of the financial crisis of 2008-2009, Congress is spreading the blame liberally across various constituencies, including the almighty rating agencies (think of Moody’s [MCO], Standard & Poor’s [MHP], and Fitch). The Senate recently added a proposed amendment to the financial regulation bill that would establish a government appointed panel to select a designated credit rating agency for certain debt deals. The proposal is designed to remove the inherent conflict of interest of debt issuers – such as Goldman Sachs Group Inc. (GS), Morgan Stanley (MS), UBS, and others – shopping around for higher ratings in exchange for higher payments to the banks. The credit rating agencies are not satisfied with being weighed down with a ball and chain, and apparently New York Attorney General Andrew Cuomo is sympathetic with the agencies. Cuomo recently subpoenaed Goldman Sachs Group Inc., Morgan Stanley, UBS and five other banks to see whether the banks misled credit-rating services about mortgage-backed securities.

Slippery Slope of Government Intervention

Many different professions, inside and outside the financial industry, provide critical advice in exchange for monetary compensation. In many industries there are inherent conflicts of interest between the professional and the end-user, and a related opinion provided by the pro may result in a bad outcome. If government intervention is the appropriate solution in the rating agency field, then maybe we should answer the following questions related to other fields before we rush to regulation:

- Should the government control which auditors check the books of every American company because executives may opportunistically shop around for more lenient reviews of their financials?

- Perhaps the Securities and Exchange Commission (SEC) should dictate which investment bank should underwrite an Initial Public Offering (IPO) or other stock issuance?

- Maybe the government should decide which medicine or surgery should be administered by a doctor because they received funding or donations from a drug and device company?

Where do you draw the line? Is the amendment issued by Al Franken (Senator of Minnesota) a well thought out proposal to improve the conflicts of interest, or is this merely a knee-jerk reaction to sock it some greedy Wall Street-ers and solidify additional scapegoats in the global financial meltdown?

In addition to including a controversial government-led rating agency selection process, the transforming regulatory reform bill also includes a dramatic change to ban “naked” credit default swaps (CDS). As I’ve written in the past, derivatives of all types can be used to hedge (protect) or speculate (e.g., naked CDS). Singling out a specific derivative product and strategy like naked CDSs is like banning all Browning 9x19mm Hi-Power pistols, but allowing hundreds of other gun-types to be sold and used. Conceptually, proper use of a naked CDS by a trader is the same as the proper use of a gun by a recreational hunter (see my derivatives article).

Solutions

Rather than additional government intervention into the rating agency and derivative fields, perhaps additional disclosure, transparency, capital requirements, and harsher penalties can be instituted. There will always be abusers, but as we learned from the collapse of Arthur Andersen on the road to Enron’s bankruptcy, there can be cruel consequences to bad actors. If investment banks misrepresent opinions, laws can lead to severe results also. Take Jack Grubman, hypester of Worldcom stock, who was banned for life from the securities industry and forced to pay $15 million in fines. Or Henry Blodget, who too was banned from the securities industry and paid millions in fines, not to mention the $200 million in fraud damages Merrill Lynch was forced to pay.

At the end of the day, enough disclosure and transparency needs to be made available to investors so they can make their own decisions. Those institutional investors that piled into these toxic, mortgage-related securities and lost their shirts because of over-reliance on the rating agencies’ evaluations deserve to lose money. If these structures were too complex to understand, then this so-called sophisticated institutional investor base should have balked from participation. Of course, if the banks or credit agencies misrepresented the complex investments, then sure, those intermediaries should suffer the full brunt of the law.

Although weighing down the cash-rich credit rating agencies (and CDS creators) with ball and chain regulations may appease the populist sentiment in the short-run, the reduction in conflicts of interest might be overwhelmed by the unintended consequences. Now if you’ll please excuse me, I’m going to do my homework on a naked CDS related to a AAA-rated synthetic CDO (Collateralized Debt Obligation).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in MCO, MHP, GS, MS, JPM, UBS, BAC, T or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Goldman: Gambling Prosperity at Client Expense?

What a scene that 11-hour Senate subcommittee interrogation of Goldman Sachs (GS) executives was on C-Span – I’m still wondering whether a forklift was utilized to hoist in the multi-thousand page binders stuffed with reams of exhibits. With caffeine beverage firmly in hand, I watched as much of the marathon as possible until fatigue set in. Not all was lost though, because I managed to simultaneously conduct new stock research as I was glued to the hearings. After I saw the Goldman executives repeatedly wrestle open the gargantuan-sized binders of smoking-gun emails, I checked the paper futures markets and am now contemplating a purchase of International Paper’s (IP) stock.

Lead trader of the controversial Abacus/John Paulson deal, “Fabulous Fab” Fabrice Tourre, did not disappoint his supporters either, firmly addressing his responses in his French Pepe Le Pew accent. His Goldman trading counterparts (Daniel Sparks, ex-mortgage department head, Joshua Birnbaum, ex-managing director of the department, and Michael Swenson, current managing director of the department), like all Goldman witnesses, did their best at bobbing and weaving the intrusive, pointed questions. On the cozier side of the questioning fence, the Senators did a superb job of raking the Goldman execs over the coals with endless exhibits of emails. Judging by the shiny, sweating mugs of the traders, the Senators were successful in making the testifiers uncomfortable – either that, or the Senators had the thermostat in the room raised to 82 degrees.

Betting Away to Profits

At the heart of the questioning was the key issue of whether Goldman Sachs executives and employees were acting in the best interest of their clients (fiduciary duty), or were they making bets against clients with the benefit of privileged information. Senator Claire McCaskill compared Goldman to a bookie manipulating bets in their own favor without sharing their edge with bettors (investors). In the case of the Abacus deal, Goldman admits to not freely disclosing the involvement of now-famous, mortgage market short seller John Paulson (see the Gutsiest Trade) to the so-called sophisticated institutional investors, ACA Capital Holdings Inc. Was this lack of disclosure illegal? Perhaps unethical, but pundits have already established the high hurdle the SEC (Securities and Exchange Commission) will need to clear in order to prove Goldman’s guilt.

Based on the testimony and facts introduced in the hearings, and as I write in my previous Goldman article (Goldman Cheat?), Goldman’s behavior throughout the housing collapse and participation in the ACA deal reflects more about intelligent opportunism within a loose regulatory framework than it does about criminal behavior. Having managed a $20 billion fund (see my book) I dealt with the conflicts of interest and self dealings of the investment banks first hand. As I entered trade orders reaching into the millions of shares, do I naively believe Goldman and other banks altruistically kept that information in their trading vaults? Or is it possible that information leaked out to other clients or was used for the banks benefit? Suffice it to say, the regulatory structure and conflict of interest frameworks, as they stand today, are not stacked in favor of investors.

The Solutions

Although we wish our regulators and government officials could have been more forward looking, rather than reactive, nonetheless, some reforms need to be instituted to resolve the substantial risks built into our financial system today. Here are a few ideas from the 10,000 foot level:

Volcker Rule: Former Federal Reserve Chairman’s so-called “Volcker Rule” is looking better by the minute. Not a new concept, but as regulators shine the light on the opaque industry of derivatives trading and proprietary trading desks, the need for new reforms becomes even more evident. Derivatives are not evil (see Financial Engineering), but like a gun or knife, if misused these instruments can become extremely dangerous…as we have found out. The Glass-Steagall Act, which separated investment bank functions from commercial bank functions, was repealed almost 70 years after its introduction in 1932. The Volcker Rule would be a “lite” version of Glass-Steagall Act because the thrust of the proposal is aimed at splitting the risk-taking proprietary trading desk activities from the client based activities.

Heightened Capital: If you rented out an exotic car or motorcycle from a store, you would likely be required to commit a deposit or collateral to protect against adverse conditions. The same principle applies to derivatives, which generally raises volatility due to inherent leverage. The riskier the product, the larger the capital requirement should be. The collapse of Bear Stearns, Lehman Brothers, and AIG are painful lessons learned from situations of excessive leverage.

Central Clearing/Transparency: Derivative products such as options, futures, and swaps have existed for decades. The transparency gained by trading these securities on exchanges increases market confidence, thereby increasing liquidity and lowering costs for end-users. Standardization around complex derivatives like CDOs (Collateralized Debt Obligations), CDSs (Credit Default Swaps), and CLOs (Collateralized Loan Obligations) is a must to ensure the fact regulators can actually understand the products they are regulating.

Credit Rating Agency: It’s not entirely clear to me that the rating agencies play a critical role in the market place. In effect, the agencies serve as an outsourced research resource primarily for fixed income investors. If the agencies disappeared today, investors would be forced to do their own homework on each deal – not necessarily a bad idea. If the existing oligopoly structure of agencies ultimately survives, I suggest penalties should be incurred by firms with inaccurate ratings. Conversely, ratings could be structured such that compensation could be tiered (or escrowed) over time with payment incentives tied to the underlying deal performance relative to ratings accuracy.

Too Big To Fail: The massive bailouts and TARP (Troubled Asset Relief Program) money handed out to the financial and auto companies have left a sour taste in taxpayers’ mouths. A systemic risk regulator with the authority to unwind unhealthy institutions makes common sense. An insurance pool financed by self-inflicted industry taxes would assist regulators in achieving the reduction of troubled financial institutions.

Fiduciary Duty: Sidoxia Capital Management is a Registered Investment Advisor (RIA) and must act in the best interests of the client. Unfortunately, much of the industry is structured with a much lower “suitability” threshold, which provides a veil for firms to engage in less than ethical behavior.

Overall, regulatory reform urgency is in the Washington D.C. air and there is no question in my mind that a certain degree of witch hunting and scapegoating is occurring. Nonetheless, Lloyd Blankfein and team Goldman Sachs made it out alive from the Congressional hearing, but not without suffering some negative reputational damage. Former Goldman CEO alum and Treasury Secretary Henry Paulson probably sent roses to Mr. Blankfein thanking him for taking Paulson’s job before the 2008 market collapse. When regulatory reform eventually kicks in, perhaps Lloyd Blankfein and Henry Paulson will take a trip to Las Vegas to celebrate (or commiserate).

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and in a security derived from an AIG subsidiary, but at the time of publishing SCM had no direct positions in GS, IP, AIG, JPM/Bear Stearns, LEH/Barclays or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Goldman Cheat? Really?

Really? Am I supposed to be surprised that the SEC (Securities and Exchange Commission) has dug up a CDO (Collateralized Debt Obligation) deal with $1 billion in associated Goldman Sachs (GS) losses? The headline number may sound large, but the billion dollars is not much if you consider banks are expected to lose about $3 trillion dollars (according to an International Monetary Fund report) from toxic assets and bad loans related to the financial crisis. Specifically, Goldman is being charged for defrauding investors for not disclosing the fact that John Paulson (see Gutsiest Trade), a now-famous hedge fund manager who made billions by betting against the subprime mortgage market, personally selected underlying securities to be included in a synthetic CDO (a pool of mortgage derivatives rather than a pool of mortgage securities).

Hurray for the SEC, but surely we can come up with more than this after multiple years? More surprising to me is that it took the SEC this long to come up with any dirt in the middle of a massive financial pigpen. What’s more, the estimated $1 billion in investor losses associated with the Goldman deal represents about 0.036% of the global industry loss estimates. These losses are a drop in the bucket. If there is blood on Goldman’s hand, my guess is there’s enough blood on the hands of Wall Street bankers to paint the White House red (two coats). The Financial Times highlighted a study showing Goldman was a relative small-fry among the other banks doing these type of CDO deals. For 2005-2008, Goldman did a little more than 5% of the total $100+ billion in similar deals, earning them an unimpressive ninth place finish among its peers. As a matter of fact, Paulson also hocked CDO garbage selections to other banks like Deutsche Bank, Bear Stearns, and Credit Suisse. The disclosure made in those deals will no doubt play a role in determining Goldman’s ultimate culpability.

Context, with regard to the fees earned by Goldman, is important too. Goldman earned less than 8/100th of 1% of their $20 billion in pretax profits from the Abacus deal. Not to mention, unless other charges pile up, Goldman’s roughly $850 billion in assets, $170 billion in cash and liquid securities, and $71 billion in equity should buttress them in any future litigation. These particular SEC charges feel more like the government trying to convict Goldman on a technicality – like the government did with Al Capone on tax evasion charges. At the end of the day, the evidence will be presented and the courts will determine if fraud indeed occurred. If so, there will be consequences.

Demonize Goldman?

How bad can Goldman really be, especially considering their deep philanthropic roots (the firm donated $500 million for small business assistance), and CEO Lloyd Blankfein was kind enough to let us know he is doing “God’s work,” by providing Goldman’s rich menu of banking services to its clients.

Certainly, if Goldman broke securities laws, then there should be hell to pay and heads should roll. But if Goldman was really trying to defraud investors in this particular structured deal (called Abacus 2007-ACI), then why would they invest alongside the investors (Goldman claims to have lost $90 milllion in this particular deal)? I suppose the case could be made that Goldman only invested for superficial reasons because the fees garnered from structuring the deals perhaps outweighed any potential losses incurred by investing the firm’s own capital in these deals. Seems like a stretch if you contemplate the $90 million in losses overwhelmed the $15 million in fees earned by Goldman to structure the deal.

Maybe this will be the beginning of the debauchery flood gates opening in the banking industry, but let’s not fully jump on the Goldman Scarlet Letter bandwagon just quite yet. Politics may be playing a role too. The Volcker rule was conveniently introduced right after Senator Scott Brown’s Senate victory in Massachusetts, and political coincidence has reared its head again in light of the financial regulatory reform fury swelling up in Washington.

Waiting for More teeth

There is a difference between intelligent opportunism and blatant cheating. There is also a difference between immorally playing a game within the rules versus immorally breaking laws. Those participants breaking the law should be adequately punished, but before jumping to conclusions, let’s make sure we first gather all the facts. While the relatively minute Abacus deal may be very surprising to some, given the trillions in global losses caused by toxic assets, I am not. Surely the SEC can dig up something with more teeth, but until then I will be more surprised by Jesse Jame’s cheating on Sandra Bullock (with Michelle “Bombshell” McGee) than by Goldman Sachs’s alleged cheating in CDO disclosure.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GS, DB, Bear Stearns (JPM), and CSGN.VX/CS.N or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}